Newsletter

Newsletter

In the previous article, we learned that we are quite a savings-minded bunch. But how much wealth does this generate? Which investments are currently very popular? Which ones are wallflowers? And what are the differences in investment behavior by gender, age, wealth and region? You can find the answers in this article.

Contents

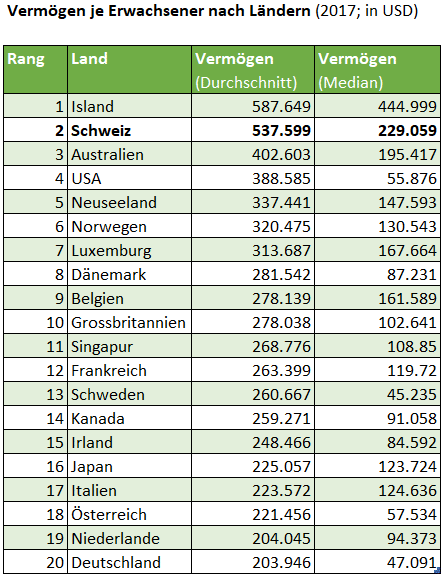

Swiss with the world’s second-highest wealth

According to the Credit Suisse Global Wealth Report 2017, the average net wealth per adult in Switzerland after deducting debts is exactly USD 537,599, putting Switzerland in second place behind Iceland (see Figure 1).![]()

This amount probably seems surreally high to most people. There are two factors to bear in mind here: firstly, it includes our compulsory contributions to the occupational pension scheme. Secondly, these are average values.

Median beats average (in terms of informative value)

Averages make sense for body sizes because we can assume a normal distribution. For assets, on the other hand, average values are not very meaningful due to the great inequality.

To illustrate: a single billionaire, of which there are a few in Switzerland, and 99 destitute people result in an average wealth per person of CHF 10 million.

A better reference value in such cases is the median, which divides wealth into two groups: One half of Switzerland owns more than the median wealth, the other half less. The study in question arrives at a median value of USD 229,059, which in our opinion is still an extremely high amount (see Figure 1)

Now let’s go one step further and look at the question of how Mrs. and Mr. Swiss invest their obviously abundant money.

Cash and savings account top – ETFs flop (unfortunately)

In 2018, the Moneyland comparison service conducted a representative survey on the investment behavior of around 1,500 people in Switzerland together with the market research institute GfK. Respondents were asked how much money they had invested in various financial investments.

The most popular investments are listed below in descending order:

- 67% have cash as an investment

- 64% have medium or large amounts in their savings account

- 59% have medium or large amounts in their private account

- 55% have a 3a account; 43% have a 3a fund

- 41% have invested in real estate (usually in owner-occupied property)

- 39% have shares (individual securities)

- 25% have actively managed investment funds

- 19% have invested in gold and 10% in other precious metals

- 14% have ETFs (this ingenious investment vehicle is unfortunately still too unknown; click here for the explanatory article: ETFs: The investment revolution)

- 12% own structured products

- 8% are invested in cryptocurrencies

– Partner Offer –

In our experience and due to the low costs for ETFs, a particularly attractive broker at present is “DEGIRO” (link to the DEGIRO Review). Bei Interesse kannst du dich bei DEGIRO über unseren Partnerlink anmelden, womit du dir Trading Credits von 100 CHF (mit Bedingungen) sicherst und gleichzeitig unseren Blog unterstützt.

– – – – –

Young people opt for low-risk investments – and bitcoins

Investment behavior also changes significantly depending on the age group. Among the youngest group of respondents aged between 19 and 25, private accounts, savings accounts and cash are more common than average.

At the same time, older respondents have a lower affinity for new technologies and investment opportunities. Cryptocurrencies such as Bitcoin are significantly more popular among younger than older investors. Conversely, ownership of shares, real estate and investment funds increases significantly with age.

The wealthier, the riskier

Investment behavior is strongly influenced by the personal wealth situation. Many asset classes correlate positively with growing wealth, including investment funds, ETFs, equities, real estate, structured products and even 3a savings accounts.

What is meant here is not only absolute values, but also that the relative values in relation to the other invested assets increase with increasing assets.

This finding is particularly evident among the richest group of people with assets of CHF 1 million or more. Virtually all millionaires have invested in equities and real estate, two thirds in a 3a savings account, 65% in investment funds and around half in structured products and ETFs.

Cautious women

Women are generally more reluctant to invest than men. This is particularly evident with somewhat riskier forms of investment such as shares, investment funds and speculative investments such as structured products and cryptocurrencies.

Only just over a quarter of women hold shares, while around half of men own such securities.

Depending on the asset class, there are clear differences between the language regions. For example, investments in cash, private accounts and savings accounts are more popular in German-speaking Switzerland than in French-speaking Switzerland.

The difference is also clear when it comes to shares: 41% of respondents in German-speaking Switzerland own shares, compared to just 28% in French-speaking Switzerland. Interestingly, highly speculative cryptocurrencies such as Bitcoin are slightly more popular in French-speaking Switzerland than in German-speaking Switzerland.

In contrast, the differences between the urban and rural populations are not significant for most asset classes.

Conclusion

At USD 537,599 (average) and USD 229,059 (median), the net assets (i.e. less debts) of adults living in Switzerland are very high by international standards. This puts Switzerland in 2nd place behind Iceland.

With the exception of millionaires, the majority of people in Switzerland invest very conservatively across all age groups, genders and regions.

This is all the more surprising given that the popular savings and private accounts have not yielded any interest for years, as we have shown in this article. And there are very attractive alternatives on the market in the form of ETFs.

If we also take into account the current inflation rate of around 1 percent, the result is a gradual loss of wealth.

You can get a complete overview of the topic of “Investing” here: Learning to invest – in eight lessons.

1 Kommentare

Klasse Beitrag! Einen ähnlichen, aber doch ganz anderen habe ich erst kürzlich auf meinem Blog veröffentlicht! Über deine Meinung wäre ich sehr gespannt, LG Eric