Newsletter

Newsletter

Accumulating wealth is relatively simple, for example by investing regularly in an equity ETF. It is more complex to withdraw the assets you have saved so that they secure your standard of living for many years and last until the end of your life. So that you can retire early with peace of mind, you need a clever withdrawal plan as the key to your financial freedom – the happy ending to your financial planning, so to speak! In this article, we present three withdrawal plans, show you which one is our favorite and why we think the popular “4 percent rule” is unsuitable.

Short & sweet

- With a clever withdrawal plan, your assets will last from the start of your early retirement until your death while consuming as much as possible.

- To withdraw assets from the portfolio, you can sell parts of your assets, “consume” distributed dividends and interest or combine the two.

- For a withdrawal plan, you need the amount of your available initial assets, their average return, your annual consumer spending and your life expectancy.

- We examined three withdrawal plans that differ from each other in terms of withdrawal rate and/or market risk.

- We prefer a flexible withdrawal plan. It is based on the annuity rule and rules out premature bankruptcy.

- On the other hand, such a withdrawal plan is associated with market-related fluctuations in consumption, which can be very severe depending on stock market developments.

- These fluctuations in consumption are largely caused by the sequence of returns. Poor stock market years at the beginning of the withdrawal phase are particularly problematic.

- By means of a cash reserve, which you tap into after bad stock market years, and a withdrawal cap, which comes into play after good stock market years, you can effectively mitigate fluctuations in consumption.

Contents

- Some questions you should ask yourself before taking early retirement

- What withdrawal plans are there?

- Conclusion: take the best of both worlds for early retirement

- This might also interest you

- Updates

- Disclaimer

Some questions you should ask yourself before taking early retirement

What is a withdrawal plan?

The withdrawal plan, also known as a withdrawal strategy or withdrawal plan, involves converting the saved assets into consumption according to a predefined procedure. The withdrawal plan is therefore used during the withdrawal phase, which is the counterpart to the asset accumulation phase

Building wealth is relatively easy to implement. Our basic rules can be summarized in a few words: Invest long-term, regularly, globally diversified and cost-effectively in one or more equity ETFs.

On the other hand, it is much more complex to reduce the assets that have (hopefully) grown significantly over several decades. Ideally, a clever withdrawal plan should cover the following three needs:

- Consume as much as possible (“I don’t want to die a millionaire.”)

- Sufficiently long consumption (“I don’t want to go bankrupt before I die.”)

- Consistent consumption (“I want to enjoy a consistent standard of living.”)

Unfortunately, as we will see later, there is no withdrawal plan that can meet all these needs without compromising.

Based on these three needs, you should ask yourself the following four questions, the answers to which we have ranked in order of increasing complexity:

- How much money do I want to bequeath?

If you would like to bequeath part of your assets to your children or a charitable organization, for example, define the corresponding amount. This amount is not allocated to consumption, but reserved for the lucky heirs you have chosen.

- How much money do I need to live?

This question is not quite as easy to answer as the first one. But with a little research on your own behalf, you will be able to answer it quite precisely. This is because you can draw on a wealth of experience and a reliable database consisting of your previous expenditure. Ideally, you should not only determine your average consumer spending (standard case scenario) but also the basic necessities of life (worst case scenario) and a standard of living that you would like to achieve (best case scenario).

- How much return will my assets generate?

If you invest some of your assets in low-risk government bonds or cash in a savings account at the start of the withdrawal phase, you will probably only earn a low interest rate in line with inflation, if at all. Nevertheless, we think it’s a good idea to keep a nest egg for the unexpected. Annual increases in value, including dividends, of 8% on average are quite realistic for risky equity investments. A residual uncertainty remains: After all, past returns are no guarantee of future ones.

- How many years would I like to withdraw money from my assets?

Now it definitely gets complex. You would need to know your exact life expectancy or time of death. As an initial guide, you can use the average life expectancy as an example. According to the Federal Statistical Office, life expectancy in Switzerland is one of the highest in the world. In 2021, it was 81.6 years for men and 85.6 years for women at birth. At the age of 65, life expectancy is still 19.9 years for men and 22.7 years for women, meaning that the average time of death is 84.9 years for men and 87.7 years for women. If necessary, you can refine these values with individual factors such as state of health, lifestyle or genes. But even if you have estimated the end of your life too pessimistically or if you live longer than you have enough money for, there is no need to panic – at least not in Switzerland. We have state-run, well-managed retirement and nursing homes, to which even destitute senior citizens are entitled.

Who needs (no) withdrawal plan?

Even though we use the term “early retirement” in this article, we are actually referring to anyone who wants to retire with assets. It is therefore basically irrelevant whether retirement is conventionally planned for mid-60s, at 70 or – which is currently very much the trend – earlier, for example at 50 or even at 40 (see also our article “Financial freedom – hype or a goal worth striving for?”.

However, it is obvious that a reliable withdrawal plan is even more important for early retirement, as there are no state-guaranteed pension benefits until normal retirement age or consumption is covered exclusively by assets.

In addition, our target audience wants to consume their available capital over the long term or until their death in order to secure and optimize their accustomed standard of living.

However, the topic of “early retirement with a withdrawal plan” is likely to be less interesting for people who will have saved little or no assets by the time they retire. This is because they simply do not need a withdrawal plan. In Switzerland, their pension is regulated by the state, based on AHV (1st pillar), pension fund (2nd pillar) and, if necessary, supplementary benefits.

These people enjoy a high degree of security in terms of the reliable payment of their state pension until their death. In contrast, they have to accept more or less significant reductions in their standard of living. This is because our state pension benefits are primarily geared towards existential needs such as food, housing and health. Another disadvantage is that people without their own savings cannot freely determine their retirement age or voluntarily take early retirement.

What are the risks of early retirement?

Risks are always associated with uncertainties. And there are plenty of these when it comes to early retirement and the associated withdrawal plans. However, the more carefully you deal with your individual withdrawal plan (including answering the questions in the previous chapters), the better you will have the following risks under control:

- Glide risk: Risk that the assets will be used up before the end of the planned withdrawal period. This risk is influenced by the sequence of returns risk and the longevity risk.

- Standard of living risk: Risk that your standard of living will have to be involuntarily restricted as a result of fluctuations in consumption.

- Unplanned inheritance: Risk that the assets reserved for consumption will not be used up completely after the planned withdrawal period has expired.

For our traditionally security-conscious compatriots, the risk of bankruptcy is probably the most serious risk. For this reason, the majority of pensioners will probably calculate too cautiously.

In Switzerland, however, a guaranteed state pension and – if all else fails – supplementary benefits cushion this risk. Of course, this state pension only applies to people who have reached the normal retirement age in their mid-60s. Anyone who wants to take early retirement cannot rely on it. They are all the more dependent on a well thought-out withdrawal plan.

We therefore believe, and subsequent market simulations suggest, that the much more likely risk is the “unplanned inheritance”. This risk may seem harmless, but it can be very drastic. Specifically: out of fear of the risk of bankruptcy, Mr. and Mrs. Schweizer restrict their consumption too much during the withdrawal period, i.e. usually over several decades. As a result, their own quality of life suffers – to the benefit of their happy heirs!

How should I withdraw money from my assets?

Before we examine and evaluate the most important extraction plans, let’s look at this last, non-match-decisive question. This is about the withdrawal technique. Basically, you have the following three options to choose from:

- Withdrawal of dividends and interest

- Sale of assets

- A combination of both

The use of dividends and interest is likely to be somewhat cheaper because brokers generally do not charge any fees for this. Partial sales, on the other hand, usually incur not only brokerage fees, but also stamp duty if the broker is a Swiss broker such as Swissquote(Review). Two established foreign brokers on the Swiss market with low fees and no stamp duty are DEGIRO(Review) and Interactive Brokers(Review).

In addition, distributions are more convenient as they are made automatically, whereas partial sales usually have to be “triggered” manually.

With regard to income tax, it does not matter whether you access the cash flows or sell assets. This is because dividends must be taxed as income for both distributing and accumulating securities. In the article “ETF taxes Switzerland: Optimize your portfolio with these 4 tax-saving tips” you will find more detailed information on the tax topic.

Realistically, the first choice for most investors will be a withdrawal technique consisting of a combination of dividends and interest on the one hand and – more relevant in terms of amount – asset sales on the other. After all, if you can only live off dividends and interest, you need very large assets. In addition, it contradicts the actual purpose of a withdrawal strategy to only access the fruits without touching the actual assets.

– Partner Offer–

– – – – –

What withdrawal plans are there?

There are probably countless withdrawal plans. We will concentrate on the following three withdrawal plans, each based on a different basic strategy:

- Early retirement withdrawal plan variant 1: Fixed withdrawal amounts without market risk

- Early retirement withdrawal plan variant 2: Fixed withdrawal amounts with market risk

- Early retirement withdrawal plan variant 3: Flexible withdrawal amounts with market risk

These three variants can be both combined and individually modified. They therefore differ in terms of the two factors withdrawal amounts (static vs. flexible) and market risk (without vs. with). Below we take a closer look at these three withdrawal plans and some sub-variants and evaluate them.

Early retirement withdrawal plan variant 1: Fixed withdrawal amounts without market risk

In this first variant, the assets are not invested in the stock market during the withdrawal phase and are not subject to market fluctuations.

So let’s assume that your available assets are safely deposited in your bank account with an interest rate that corresponds exactly to inflation. You can’t expect a higher return.

The advantages of this option are obvious: predictability, constant consumption and no (premature) bankruptcy. Important: The latter refers to your defined withdrawal period. If you outlive this period, you also run the risk of bankruptcy.

This option is therefore particularly suitable for very wealthy individuals who can afford to forego real asset growth and the associated market risk. For example, if you have liquid assets of CHF 3 million saved and in your bank account at the start of the withdrawal phase, you can consume CHF 100,000 in real terms every year for 30 years. This is enough for a financially carefree retirement. All the more so as the state pension is added to this.

This option is also suitable for risk-averse people who only need a small amount of money for life. For example, if you have assets of “only” CHF 1 million in your savings account at the start of the withdrawal phase, you can consume CHF 33,333 a year in real terms over 30 years. You won’t be able to make any great leaps in the high-price island that is Switzerland. But if you take state pensions into account, you should still be able to make ends meet.

Advantages/disadvantages of early retirement withdrawal plan variant 1: Fixed withdrawal amounts without market risk

No premature bankruptcy Constant consumption No unplanned inheritance: assets are used up in full

No premature bankruptcy Constant consumption No unplanned inheritance: assets are used up in full  Restricted consumption by foregoing higher returns (no risk premium) High standard of living only possible with high assets

Restricted consumption by foregoing higher returns (no risk premium) High standard of living only possible with high assets Line spacing

Early retirement withdrawal plan variant 2: Fixed withdrawal amounts with market risk

With this second option, you also withdraw a fixed withdrawal amount plus inflation adjustment. This means that your withdrawal rate remains constant in real terms. In contrast to variant 1, however, your available assets are subject to market-related fluctuations.

Like variant 1, this variant also guarantees you a constant standard of living thanks to the fixed withdrawal rate. In contrast to variant 1, you benefit from the risk premium in the form of increases in the value of your equity investments.

However, you run two risks: An unplanned inheritance and the risk of bankruptcy. As these two risks are mutually exclusive, only one of them can occur. As we will see later, the probability of occurrence for the “unplanned inheritance” risk is significantly higher than premature bankruptcy, even with generous withdrawal rates of 5%. Generally speaking, the lower the withdrawal rate, the greater the risk of “unplanned inheritance” and the higher the withdrawal rate, the greater the risk of premature bankruptcy.

The “4 percent rule”

For a long time, the so-called “4% rule”, which was developed by Bill Bergen back in 1994, provided a concrete framework for this static withdrawal option. This rule states that you should withdraw 4% of your initial assets each year from the start of the withdrawal phase – and thanks to the risk premium, you should not go bankrupt until your death. This means that the amount withdrawn from your assets remains constant. However, in order to maintain purchasing power, it makes sense to calculate with real withdrawal amounts , i.e. to take inflation into account each year.

The Mannheim study

In the course of our research, we came across the study “Entsparen im Alter – Portfolioentnahmeestrategien in der Rentenphase”, which was first published by the two professors Philipp Schreiber and Martin Weber from the University of Mannheim in 2017 and last updated in 2020. (After publication of this article, the withdrawal simulator was updated). Weber is best known to a wider public as the inventor of the ARERO investment fund. The special feature of this mixed global fund is that it tracks the asset classes equities, bonds and commodities via indices in a single product and according to a scientific concept.

We would now like to take a closer look at the Mannheim study. On request, Jan Mertes, a doctoral student at the University of Mannheim, explained the study in more detail with regard to the portfolio composition and return simulation:

- The portfolio

The global portfolio used for the simulation is constructed as follows: A broadly diversified equity and bond portfolio with 60% equities and 40% bonds. Specifically, the portfolio is based on the MSCI All Country World Index (equities) and the Bloomberg Barclays Global Aggregate Bond Index (bonds). Dividends and interest income were taken into account. According to Mertes, the core idea behind this portfolio is to reflect the market as closely as possible and thus achieve maximum diversification (i.e. minimum unsystematic risk). This involves deliberately accepting a lower return than with a pure equity portfolio in order to be exposed to fewer fluctuations.

- The return simulation

The monthly returns of the portfolio described above were determined for the period from January 1990 to November 2018. From these returns, 360 returns are randomly drawn (with a lag) to simulate the portfolio development over 30 years (for a different planning horizon, the planning horizon in years multiplied by 12). This process is then repeated 10,000 times to map various capital market scenarios.

Surprising results for yields

Based on this huge pool of data, we took a closer look at historical yields and came to the following, sometimes astonishing, conclusions:

| Average yield | 7,2% |

| Share of negative returns | 27% |

| Share of plus returns | 73% |

| Share of plus returns 0 – 10% | 35% |

| Share of plus returns >10% | 39% |

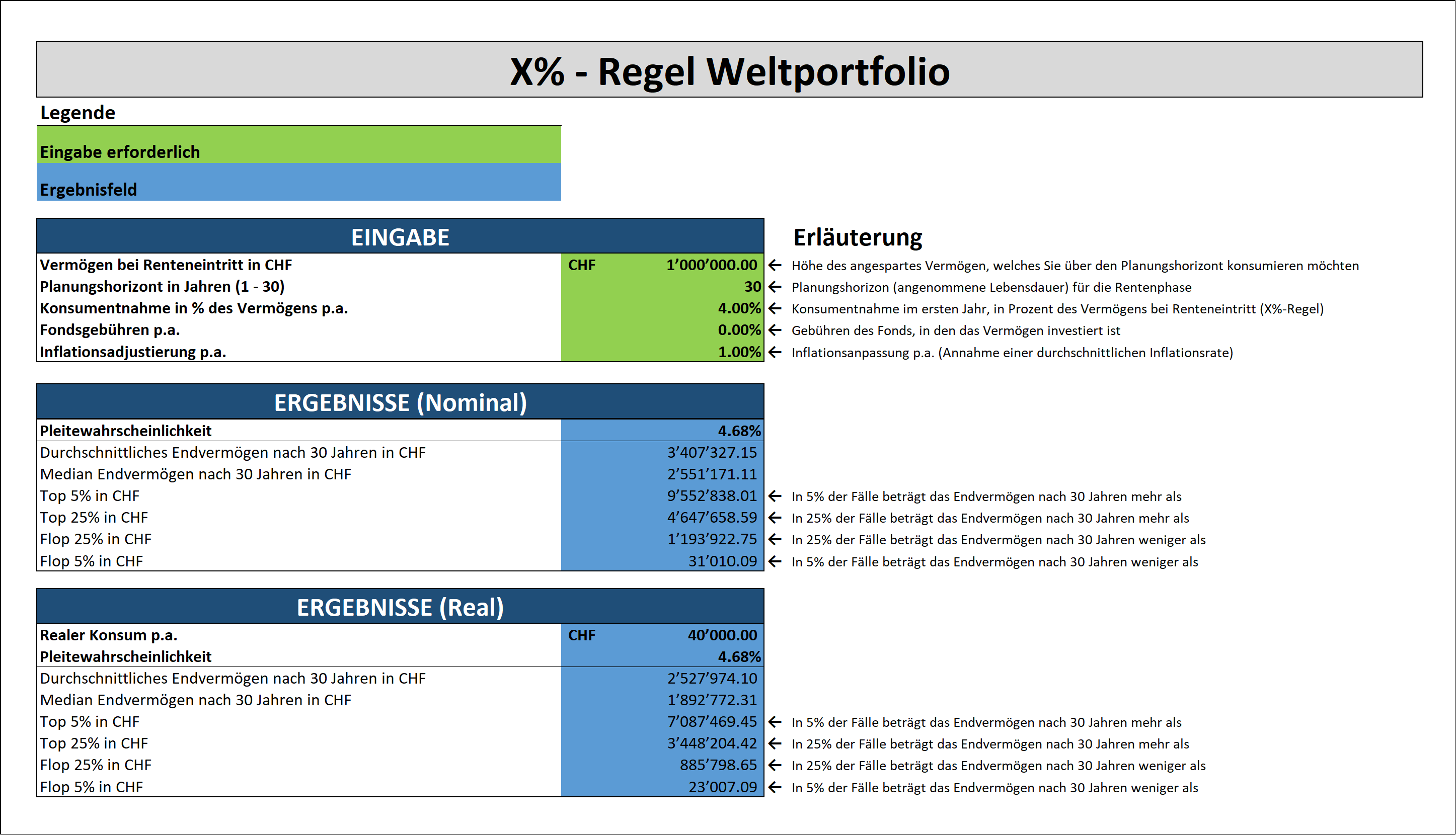

We were particularly surprised by the fact that returns of more than 10% were achieved in around four out of ten stock market years. And what about the “4% rule”? According to the Mannheim study, it seems to work quite well (see Fig. 1)

Explanation of Fig. 1: With a fixed withdrawal of 4% of the initial assets of CHF 1 million (i.e. CHF 40,000 p.a.), including inflation of 1% p.a., over a withdrawal period of 30 years, the probability that you will go bankrupt prematurely is 4.68%. Your average (real) final assets adjusted for purchasing power are more than 2.5 times your initial assets, namely CHF 2,527,974.

Based on the historical data of the Mannheim study, the “4 percent rule” therefore often leads to an unplanned inheritance and relatively rarely to premature bankruptcy.

With regard to the risk of bankruptcy, there is another important aspect to consider: The risk of bankruptcy increases when returns are unfavorable. In other words, if poor stock market years follow at the beginning of the withdrawal phase. This is the sequence of returns risk.

In this study, simulation 9 is a good example of an increased return sequence risk. In the following, we calculate the withdrawal rates for the following parameters:

| Initial assets | CHF 1 million |

| Withdrawal period | 30 years |

| Withdrawal p.a. | 5% |

| Expected inflation p.a. | 1% |

The sequence of the 30 returns in simulation 9 is shown in the table below.

| Year | Historical returns from simulation 9 of the Mannheim study |

|---|---|

| 1 | -12,30% |

| 2 | -4,50% |

| 3 | 5,04% |

| 4 | -2,26% |

| 5 | 13,42% |

| 6 | -2,08% |

| 7 | 31,19% |

| 8 | -0,63% |

| 9 | -8,87% |

| 10 | -11,53% |

| 11 | 26,27% |

| 12 | 7,83% |

| 13 | 27,02% |

| 14 | 29,77% |

| 15 | -8,23% |

| 16 | 4,13% |

| 17 | -12,33% |

| 18 | 3,90% |

| 19 | 8,77% |

| 20 | -7,12% |

| 21 | 25,07% |

| 22 | 12,40% |

| 23 | 13,56% |

| 24 | 12,87% |

| 25 | 17,60% |

| 26 | -0,05% |

| 27 | 4,67% |

| 28 | 5,38% |

| 29 | -6,79% |

| 30 | 11,99% |

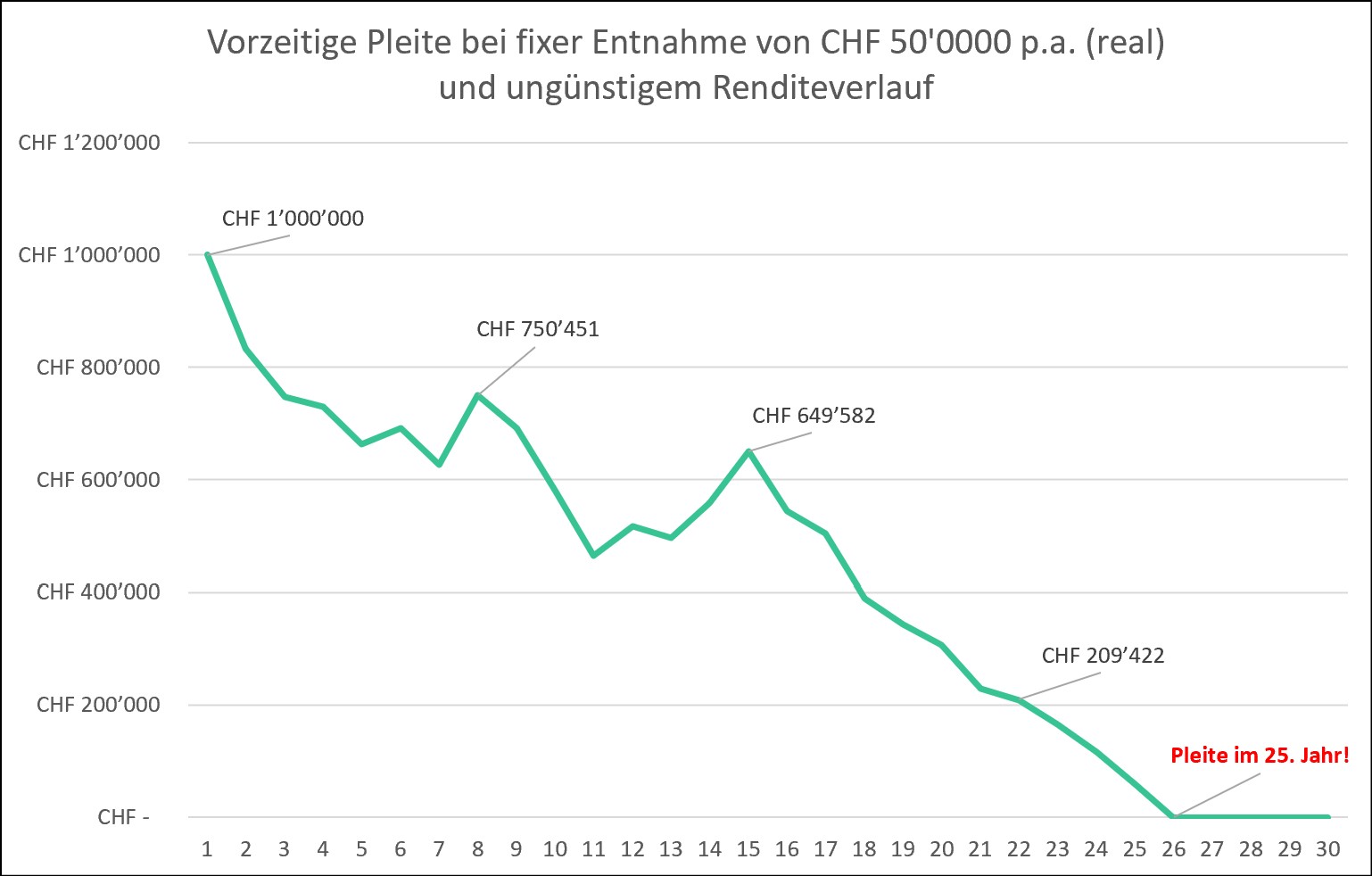

As there were some stock market divers at the beginning of the withdrawal period, the company went bust prematurely in the course of the 25th year of withdrawal (see Fig. 2).

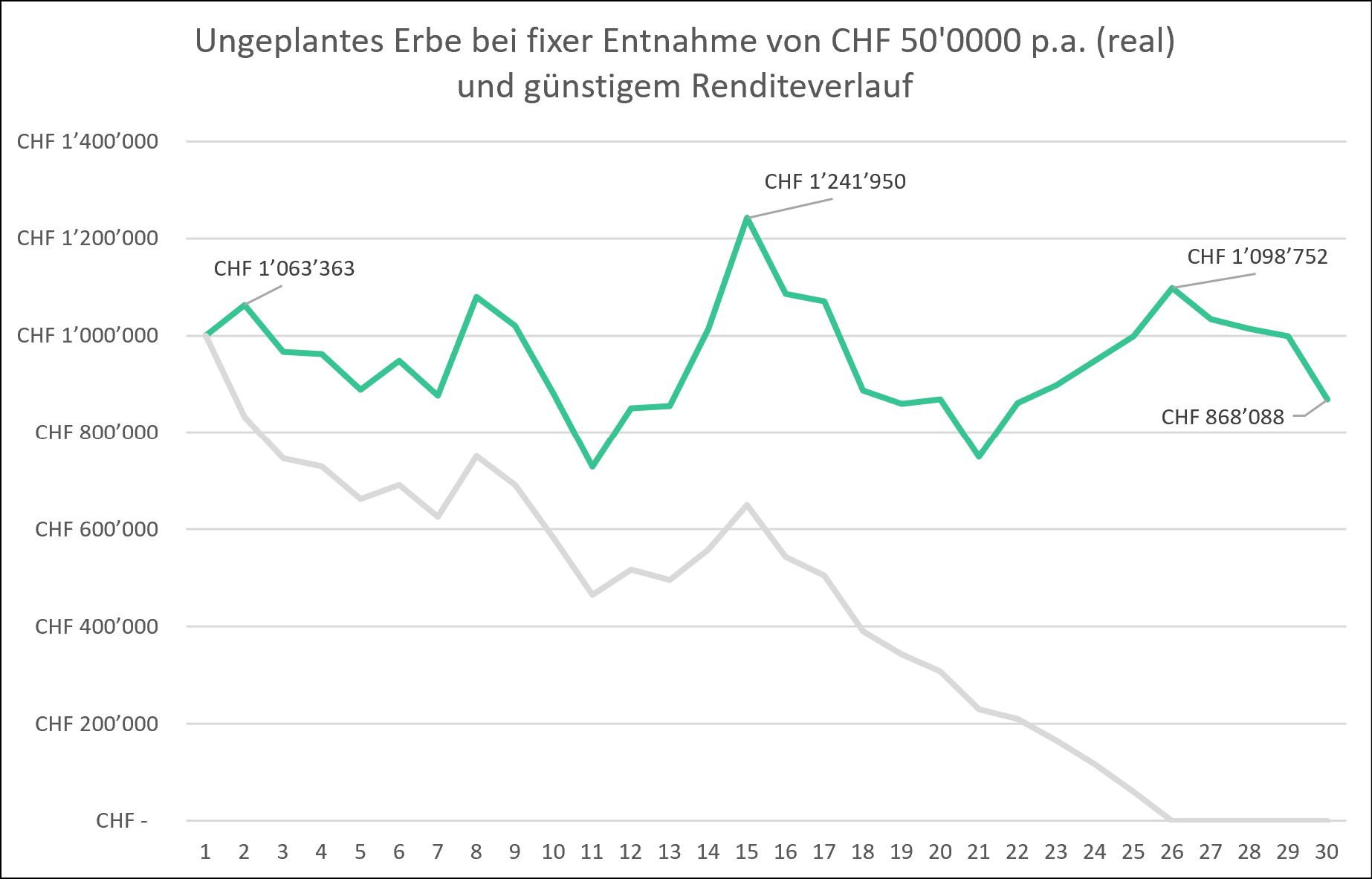

The following chart shows how incredibly strong this return sequence effect is. We have simply swapped the return in the 1st year (-12.30%) with that of the 30th year (+11.99%).

Instead of going bankrupt prematurely, after 30 years we still have a handsome fortune of CHF 868,088 in real terms!

Since we cannot influence the stock market as we see fit, we have to find other ways to get a grip on the sequence of returns risk.

But let’s leave the individual examples for the time being and return to the average values based on the entire historical database of the Mannheim study.

In the table below, we have compiled the results of nine simulations , each with three different withdrawal rates and withdrawal periods, based on initial assets of CHF 1 million and inflation of 1% per year.

| Withdrawal duration | Ø Final assets in real terms with withdrawal of CHF 30 thousand p.a. (3%) | PR | Ø Final assets in real terms with withdrawal of TCHF 40 p.a. (4%) | PR | Ø Final assets in real terms with withdrawal of TCHF 50 p.a. (5%) | PR |

|---|---|---|---|---|---|---|

| 20 years | CHF 2’099’002 | 0,04% | CHF 1’697’248 | 0,32% | CHF 1’298’931 | 3,30% |

| 25 years | CHF 2’646’426 | 0,12% | CHF 2’047’091 | 1,98% | CHF 1’467’316 | 10,20% |

| 30 years | CHF 3’391’069 | 0,45% | CHF 2’527’974 | 4,68% | CHF 1’718’889 | 17,95% |

These results from Table 2 astounded us and lead us to the following four findings:

- The risk of leakage increases with increasing extraction rate and duration.

- However, thanks to the risk premium and the compound interest effect, the average final assets increase as the withdrawal period increases. In other words, in all nine simulations, this is higher than the initial assets, adjusted for inflation. (Incidentally, the same also applies to the median final assets, albeit to a slightly lesser extent).

- The “unplanned inheritance” risk is much more likely to occur than the bankruptcy risk. According to our sample returns and periods, “only” between 0.04% and 17.95% of people go bankrupt. Conversely, this means that between 82.05% and 99.96% of assets will still be left at the end of the planned savings phase or the “unplanned inheritance” risk will occur.

- Although a fixed withdrawal strategy is easy to implement, it is unsuitable in practice (see point above).

The withdrawal strategy tool (Excel) provided free of charge by the University of Mannheim with the world portfolio simulation described above no longer exists in this form. You can download the updated version via this link.

Criticism of the “4 percent rule”

Recently, the “4% rule” has been increasingly called into question. It is not so much the static withdrawal that is being criticized (which is our focus), but rather the “4 percent” is being questioned or judged to be too optimistic.

The US study “The Safe Withdrawal Rate: Evidence from a Broad Sample of Developed Markets” from September 22, 2022 concludes that the popular “4% rule” is not based on suitable data: no international focus (home bias) and an observation period that is no longer representative for today (1926 – 1991). It is therefore not reliable enough and the risk of bankruptcy is too high. Statistically speaking, according to the study, a US couple aged 65 may withdraw a maximum of 2.26% of their initial assets so that their risk of bankruptcy does not exceed 5%.

This is of course depressing news, because the lower the withdrawal rate falls, the less money is available for consumption. People would therefore have to make do with a more modest standard of living, retire later or a combination of both.

But we do not share this alarmist sentiment. Apart from the tangible disadvantages mentioned above, which an ever lower withdrawal rate entails, we do not consider the static concept behind it to be expedient. So let’s take a look at some examples of flexible withdrawal plans in the next chapter.

Advantages/disadvantages of early retirement withdrawal plan variant 2: Fixed withdrawal amounts with market risk

Constant consumption Higher consumption thanks to risk premium Risk of failure Unplanned legacy Line spacing

Early retirement withdrawal plan variant 3: Flexible withdrawal amounts with market risk

In contrast to variants 1 and 2, the same amount, adjusted for purchasing power, is not withdrawn every year. Instead, market fluctuations are taken into account with a flexible withdrawal rate.

So you redefine your withdrawal rate every single year. There will be years in which you can go over the top financially. Other years, on the other hand, will bring you losses in consumption.

In concrete terms, this means two things: firstly, your standard of living depends to a certain extent on the performance of the stock market. And secondly, all expenses that are not (life) necessities for you are maneuvering mass.

We clearly prefer a flexible withdrawal plan because it has the best advantage/disadvantage ratio for us. We accept the fluctuating consumption, which we see as the only disadvantage, as long as it remains within an acceptable range for us.

However, we need to get this risk under control. It is important that the financing of your existential expenses or basic needs is guaranteed at all times . This includes the following cost items, for example:

- Living

- Nutrition & Household

- Health (health insurance)

However, non-existential consumption is available for disposition or as a maneuvering mass. We call it lifestyle consumption. This includes the following cost items, for example:

- Vacations in upscale hotels

- Regular restaurant visits

- Expensive jewelry

After a “stock market crash year”, for example, a vacation on a balcony would be the order of the day – instead of Hawaii.

Advantages/disadvantages of early retirement withdrawal plan variant 3: Flexible withdrawal amounts with market risk

Higher consumption possible thanks to risk premium No premature bankruptcy No unplanned inheritance: assets are used up completely (only guaranteed with annuity rule without bandwidth) Fluctuating consumption Line spacing

How to implement a flexible withdrawal plan with market risk

We will now take a closer look at some flexible withdrawal plans and their implementation. As different as the following sub-variants are, they can all be characterized by a variable withdrawal amount.

Practitioner method with the same interest rate

We start with the simplest variant: At the beginning of each year, you withdraw a fixed percentage of your available (remaining) assets. Again, we refer to the historical returns from the Mannheim study or simulation 9 with an unfavorable return curve.

For the calculation, we have made the following assumptions for the three required parameters:

| Initial assets | CHF 1 million |

| Withdrawal period | 30 years |

| Withdrawal p.a. | 5% |

| Expected inflation p.a. | 1% |

The residual assets after 30 years mean that the risk of “unplanned inheritance” has occurred. Although this practical method is easy to implement, it is mathematically impossible to use up all the assets at the end of the withdrawal phase if the withdrawal percentage remains the same. As a result, too few assets are withdrawn overall and the standard of living during the withdrawal phase is lower than it could have been.

We therefore cannot recommend this withdrawal plan variant.

Annuity rule with and without upper limit

Let us now turn to the original variant of flexible withdrawal plans. With the annuity rule, the consumption that can be withdrawn in each period, taking into account the expected return on the remaining assets, is calculated so that the assets are exhausted at the end of the planning horizon. With this rule, both the amount and the percentage withdrawal can fluctuate (strongly) depending on stock market developments.

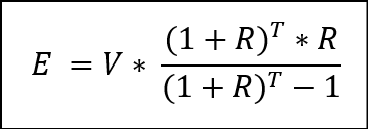

The annuity rule or the withdrawal rate per year is based on the following formula (excluding taxes and inflation):

E = Withdrawal rate at the beginning of the year according to the annuity rule

V = (Residual) assets at the beginning of the year

R = Expected return (e.g. 0.08 for an expected return of 8%)

T = Remaining years

Calculation example: With initial assets of CHF 750,000, a remaining term of 25 years and an expected return of 8%, the withdrawal rate is CHF 70,259. The withdrawal rate must be recalculated each year.

70’259 CHF = 750’000 CHF * 1.0825 * 0.08 / (1.0825 – 1)

In the last year of the defined planning period, the percentage withdrawal is 100% in each case. As a result, the assets are used up completely and the risk of “unplanned inheritance” is eliminated.

To calculate the annuity rule, we have made the following assumptions for the four required parameters:

| Initial assets | CHF 1 million |

| Withdrawal period | 30 years |

| Expected return p.a. | 8% |

| Expected inflation p.a. | 1% |

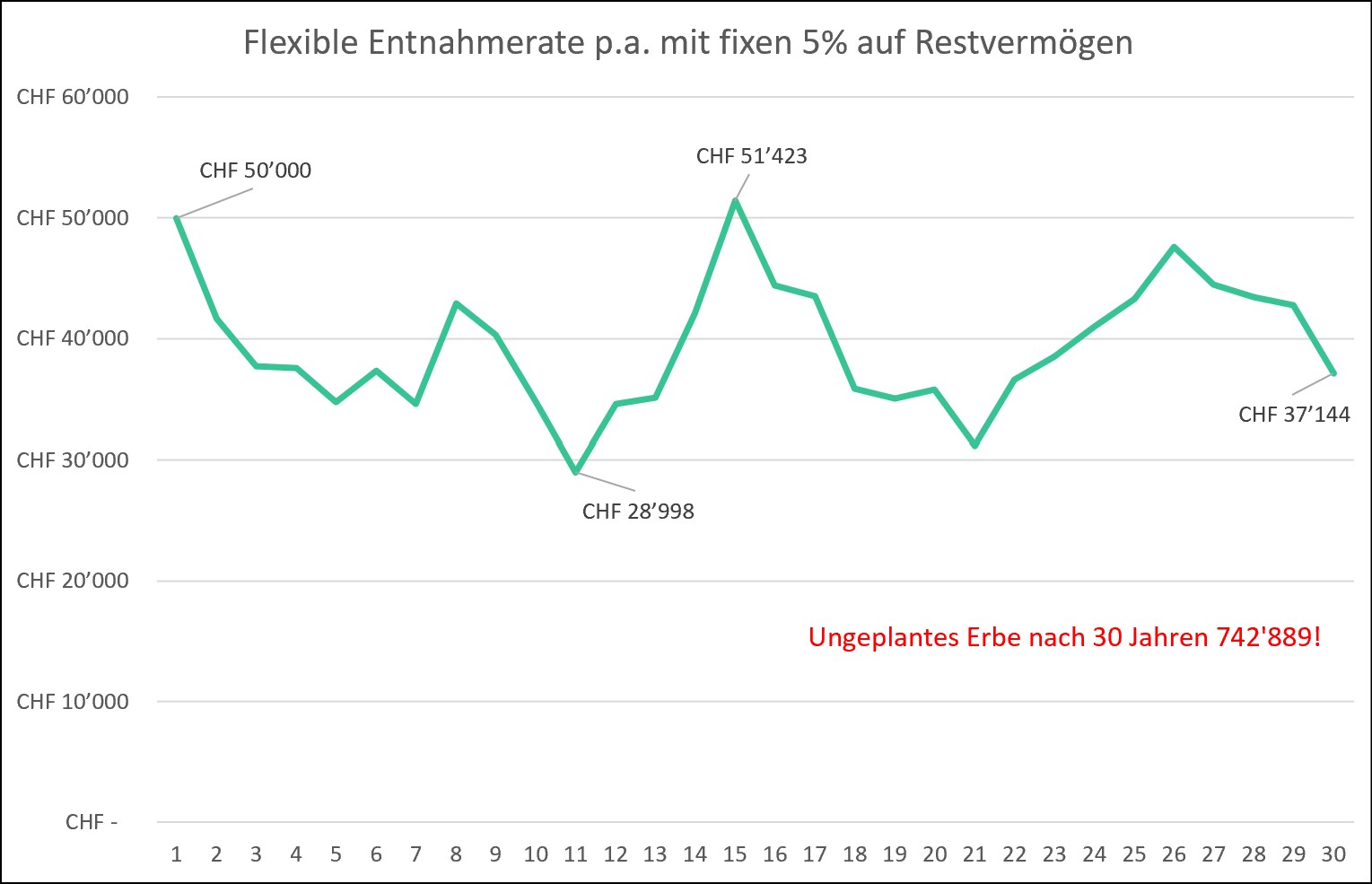

The annuity rule and the underlying formula are also included in the withdrawal strategy tool (see “Dynamic withdrawal” variant in the newly linked, updated tool) from the University of Mannheim. We again refer to the historical returns according to simulation 9. As a reminder, this is an unfavorable return constellation, which would have previously led us to bankruptcy prematurely or in the 25th year with the static withdrawal plan.

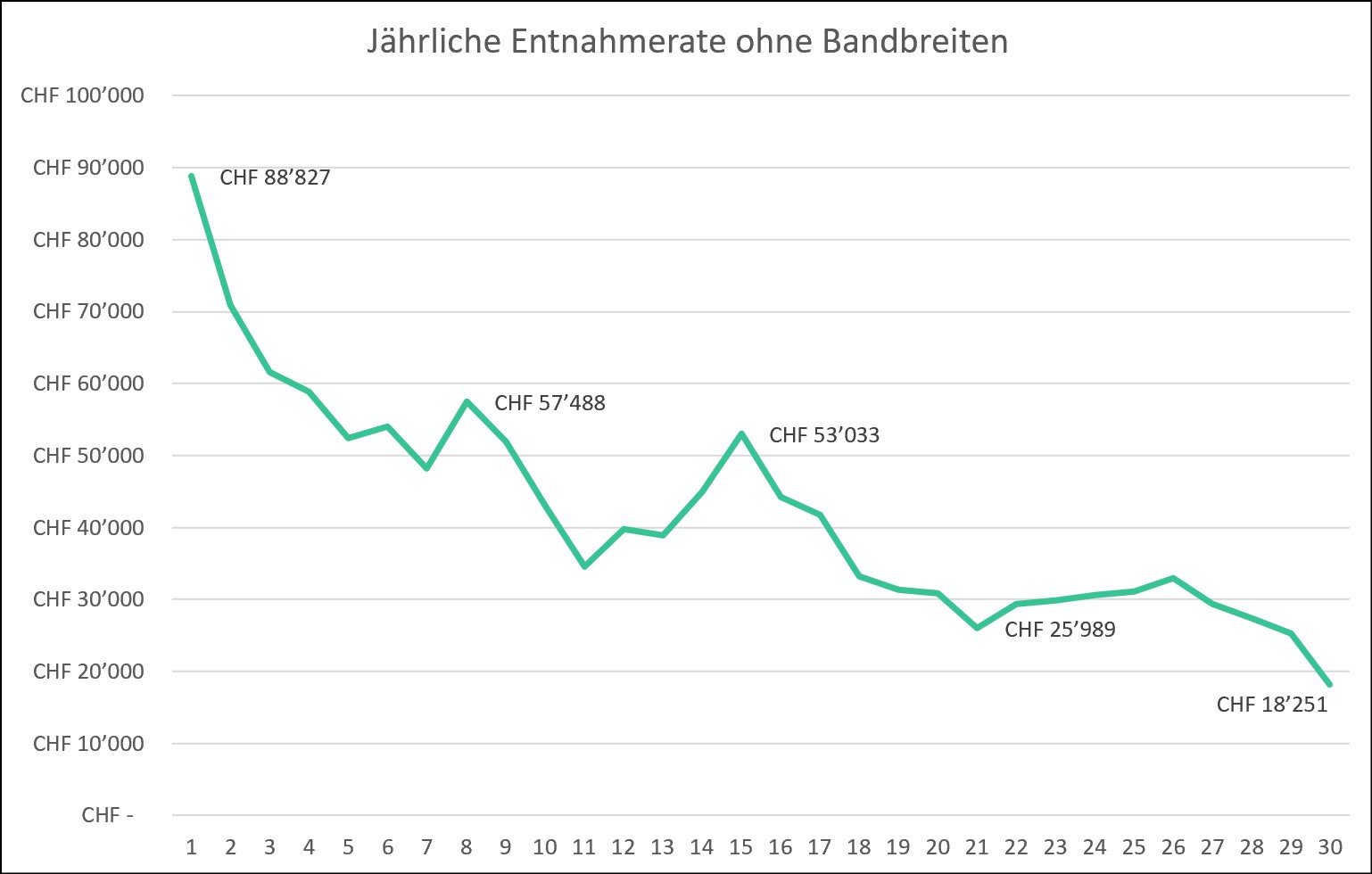

Explanation of Fig. 5: With initial assets of CHF 1 million and a flexible withdrawal rate without bandwidths, including 1% inflation, consumption fluctuates by an average of 44.06%. At the end of the defined planning period of 30 years, the assets will be completely exhausted. There is therefore neither a premature risk of bankruptcy nor the risk of “unplanned inheritance”. We have assumed an expected return of 8%.

It’s great that we have eliminated both the risk of bankruptcy and the risk of “unplanned inheritance” with the annuity rule without bandwidths! But one problem remains: The fluctuations in withdrawal rates are (too) strong, as the following illustration clearly shows.

In our example, the annual withdrawal rate fluctuates between a generous CHF 88,827 and a modest CHF 18,251.

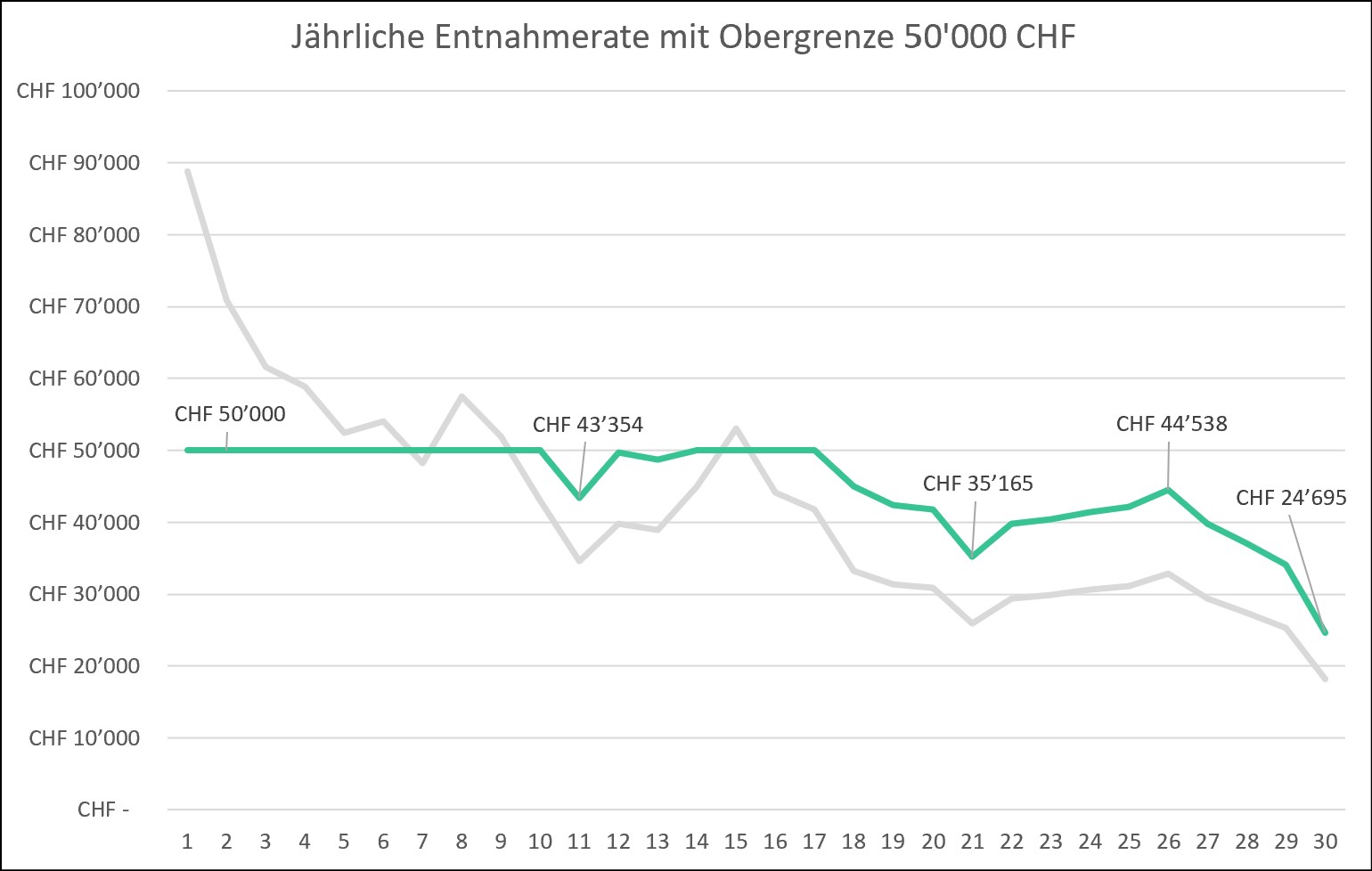

We can reduce these market-related fluctuations by means of an upper limit . In addition to the previous parameters, we therefore choose an upper limit for the annual withdrawal rate of CHF 50,000 (see Fig. 7).

Explanation of Fig. 7: With a flexible withdrawal of assets with an upper limit of CHF 50,000 p.a., including 1% inflation, consumption fluctuates by an average of 11.37%. There is no risk of bankruptcy within the defined planning period of 30 years. However, the “unplanned inheritance” risk is highly likely to occur. We have assumed an expected return of 8%.

Figure 8 shows that with our returns from simulation 9 and an upper limit of CHF 50,000, the fluctuations can be significantly mitigated. Nevertheless, the withdrawal rate still fluctuates quite strongly between CHF 24,695 and CHF 50,000, or 50%.

In this example, we have completely used up our assets at the end of the 30-year withdrawal phase and the “unplanned inheritance” risk has not materialized. However, as mentioned above, this risk cannot be ruled out with the annuity rule with an upper limit.

In order to mitigate the fluctuations even further, a lower limit should be set in addition to the upper limit. We consider a lower limit on the withdrawal rate to be particularly useful if the living expenses cannot be covered by state pensions. However, with an additional lower limit, the annuity rule would run the risk of going bankrupt prematurely, which would contradict the main purpose of this rule.

Therefore, a little creativity is required, which brings us to the conclusion.

Conclusion: take the best of both worlds for early retirement

The explanations and evaluations so far have shown one thing above all: All three withdrawal plans and their sub-variants can have serious disadvantages. Let us summarize briefly: The fixed withdrawal without market risk leads to a lower standard of living on average, the fixed withdrawal with market risk means either bankruptcy or an unplanned inheritance, and the flexible withdrawal with market risk exposes us to the whims of the stock market, which can lead to a highly fluctuating standard of living.

We would therefore like to conclude by presenting a “do-it-yourself” practical method that combines the flexible with the static “removal world”, at least in certain areas.

The annuity rule described above, on which the flexible withdrawal strategy is based, serves as a reference.

As we have impressively seen above, market fluctuations can be problematic with the flexible withdrawal strategy, depending on the course of returns. In extreme cases or after heavy price losses, the reduced withdrawal rates can no longer even cover the necessary consumption. And this is precisely where we need to start. Without throwing the whole concept of the flexible withdrawal strategy overboard, or with the following two corrective measures, you can get a grip on excessively fluctuating withdrawal rates.

Measure 1: Set an upper limit for the “best-case scenario”

This upper limit comes into effect after very good stock market years. The maximum withdrawal rate should not be set too low, but also not too high. Because if you set it too low, you run the risk of your assets not being used up (risk of “unplanned inheritance”). On the other hand, if you set it too high, you will hardly be able to mitigate the fluctuations. In our simulation above, we have capped the maximum withdrawal rate at CHF 50,000 for initial assets of CHF 1 million. This value is 25% above the “4% rule” (CHF 50,000 vs. CHF 40,000). If necessary, the upper limit can be somewhat more generous. After all, you don’t treat yourself to anything else😊.

Measure 2: Have a cash reserve ready as a nest egg

In this second measure, we use the fixed withdrawal strategy without market risk. Specifically, this means: Your withdrawal strategy consists of two withdrawal pots: equity ETFs and cash. Keep cash worth at least two annual withdrawal rates in your bank account for loss-making stock market years. With initial assets of CHF 1 million and average consumer spending of CHF 45,000, this would be around CHF 90,000. You use this cash joker in the first few bad stock market years (e.g. in the event of price losses of 10% p.a. or more). 2022, for example, would have been such a joker year, as the broad market MSCI World Index fell by around 17%.

The timing is crucial because of the sequence of returns risk. For example, if the stock market corrects downwards by 10% in the third year of withdrawal, you should play this joker immediately, because the positive effect on the subsequent withdrawal rates and their fluctuations is greatest at the beginning. However, the mitigating effect on fluctuations is much less pronounced at the end, i.e. if you only play the joker in the 23rd year instead of the 3rd.

Taboo for many investors, but possibly an alternative for cool-headed calculators: those who do not want to hoard interest-free cash for “emergencies” can instead finance their consumption for the withdrawal year after a stock market dip by means of a Lombard loan. In such a case, the assets invested exclusively with market risk would serve as collateral for the lender. The loan would only be repaid once the stock market prices had recovered, by selling assets as is customary in the withdrawal plan. Of course, it is important that the loan is financed at the lowest possible interest rates. In our experience, Interactive Brokers offers comparatively attractive interest conditions for Lombard loans.

Concluding remarks

As we have seen, you need to take a few precautions in order to retire early with peace of mind. It is particularly important that you have a well thought-out withdrawal plan. Flexibility when withdrawing assets is the be-all and end-all. The basic rule is that equity assets should not be sold after poor stock market years, or only to a limited extent.

This might also interest you

Updates

2023-09-11: Link to the University of Mannheim’s energy-saving simulator replaced by new version.

Disclaimer

Disclaimer: Investing involves risks of loss. You must decide for yourself whether you want to bear these risks or not.

Errors excepted: We have written this article to the best of our knowledge and belief. Our aim is to provide you as a private investor with the most objective and meaningful financial information possible. However, should we have made any errors, forgotten important aspects and/or no longer have up-to-date information, we would be grateful if you could let us know.

19 Kommentare

Wie immer ein äusserst informativer Blog, danke euch.

Kurze Frage: Sind die 2 Jahre Cash, die man mindestens auf der Seite halten sollte bei Rente, quasi der Notgroschen? Also wenn man pensioniert ist, sollte man anstatt 3-4 Monatsgehältern oder so Cash für 2 Jahre horten?

Und wenn man ein 80/20 Portfolio hat (80% risikoreich, ETFs und 20% risikoarm, Cash), kommen die 2 Jahre Cash obendrauf?

Vermögensbildung bzw. entsprechende Strategien sind ja nicht exakte Wissenschaften. Letztlich hängt die Höhe des Notgroschens von deinem Risikoprofil ab. Wer Cash hortet, damit er für die darauffolgenden zwei Jahre im Notfall sämtliche laufenden Ausgaben decken kann, weist eher eine geringe Risikobereitschaft auf. So oder so, ob Cash für 4 Monate oder 2 Jahre, es ist Bestandteil des risikoarmen Anteils des Portfolios, also in deinem Beispiel wird es den 20% zugerechnet.

Kann ich mir wirklich sicher sein, dass keine Steuern auf die Kapitalgewinne erhoben werden?

Was wenn ich für Säule 1/2: CHF 8000 pro Monat beziehe, aber aus meinem Portfolio weitere CHF 15000 pro Monat?

Versucht die Finanzabteilung dann auf Biegen und Brechen einem ein professionelles Handeln mit ETFs vorzuwerfen?

Wäre gut zu wissen wie sich die Schweizer Steuerbehörden verhalten, ansonsten zwingt mich die Grösse meines Pirtfolios den Lebensabend in einem anderen Land mit max. 10% Kapitalertragssteuer zu verbringen.

Danke für eure Einschätzung.

Wir erachten es als sehr unwahrscheinlich, dass dich die Steuerbehörden mit deinem angedachten Entnahmeplan als gewerblichen Wertschriftenhändler einstufen würden…

Herzlichen Dank für Eure Einschätzung!

Ich bin bald in der Entnahmephase. Bei mir im Portfolio sind Aktien-ETF und ein Teil Einzeltitel (Schweizer Dividendenperlen), die ich schon seit Jahren im Depot habe. Diese Dividenden sorgen schon mal für jährlich ca. Fr. 13’000.- Einkommen. Die Barreserve ist auch vorhanden. Meine Frage: Wenn ich dann jeweils entnehme, was verkaufe ich am besten? ETF, die sich erfolgreich entwickelt haben oder besser die anderen? Oder die Einzeltitel, die seit dem Kauf massiv an Wert zugelegt haben? Das bereitet mir noch Kopfzerbrechen.

In der Entnahmephase würden wir grösseren Wert auf Stabilität und Ausgewogenheit im Portfolio legen. Das heisst, wir würden uns zuerst von (schwankungsanfälligen) Einzeltiteln trennen, dann von den (oft auch volatilen) Nischen-ETFs (falls vorhanden) und erst danach von den breit diversifizierten “Brot- und Butter”-ETFs (MSCI World & Co.). Aber das ist natürlich Geschmacksache und auch keine Anlageempfehlung:-)

Danke vielmals für den Gedankenanstoss! Und natürlich auch für den tollen und aufwändigen Artikel.

Sehr guter Beitrag, seit langer Zeit bin ich auf der Suche von so etwas. Ich wollte die Excel-Tabelle von der Webseite der Uni Mannheim herunterladen, leider funktioniert der Link nicht mehr. Könnt Ihr mir sie bitte zusenden?

Besten Dank und Grüsse,

Peter

Hoi Peter

Tatsächlich, der Link ist von der Uni Mannheim mittlerweile deaktiviert worden. Es soll jedoch hier bald Alternativen zum Download geben.

Beste Grüsse

SFB

…jetzt ist er da! hier geht’s zum neuen Entspar-Simulator der Uni Mannheim.

Ich bin sehr begeistert wie ihr das so konzentriert aber dennoch verständlich aufbereitet habt! Einfach toll!

Ich habe noch eine Rückfrage zur Datenbasis (Simulationstool). Einer der wichtigsten Kenngrössen, die zu erwartende Rendite lässt sich bei der Annuitätenregel nicht erfassen im 1. Reiter (Wo alle anderen Angaben erwartet werden). Im Reiter “Berechnung Annuitätenregel” gibt es ein Feld dafür, dass aber nicht zu Eingabe gekennzeichnet ist. Wenn man dort jetzt aber den Wert ändert, d.h. erhöht, sinkt der “Reale durschnittliche Konsum”. Das ergibt für mich keinen Sinn. Übersehe ich hier etwas?

Beste Grüsse

Gute Frage, die wir soeben an die Uni Mannheim weitergeleitet haben. Wir melden uns, sobald wir die Antwort erfahren.

Beste Grüsse

SFB

…also wenn man den angehenden Doktoranden der Uni Mannheim spannende Fragen, wie die deinige, stellt, dann scheinen sie regelrecht zur Höchstform aufzulaufen und antworten super schnell:-) Hier also die Antwort von Herrn Mertes (die von ihm erwähnten 15% Rendite sind nicht von uns, da hat er fürs bessere Verständnis wohl selber eine Annahme getroffen):

“Das hängt mit den simulierten Renditen zusammen.

Wenn Sie die Erwartete Rendite erhöhen, wird gemäß Annuitätenfaktor zu Beginn ein höherer Betrag pro Periode für den Konsum entnommen. Das macht auch erstmal Sinn, schließlich rechnet man damit, dass das verbliebene Vermögen auch stärker anwächst. Wenn nun allerdings die tatsächliche Rendite (das sind hier die simulierten Renditen) geringer ausfällt als die erwarteten 15%, reist der erhöhte Konsum ein Loch in die Planung und der zukünftige Konsum muss drastischer reduziert werden, da die zuvor erwarteten Anlageeinnahmen fehlen. Auch in den zukünftigen Perioden wird weniger Anlageeinnahmen erwirtschaftet, weil bereits so viel in den ersten Perioden entnommen wurde. Daher reduziert sich das gesamte Vermögen durch die erhöhte Erwartete Rendite.

Im Detail hängt das vom Ablauf der Renditen ab (theoretisch kann auch der umgekehrte Effekt eintreten), da aber die simulierten Renditen in dem Tool (im Einklang mit historischen Werten) nur einen Durchschnitt von etwa 7.2% aufweisen, führt eine Annahme von 15% erwarteter Rendite regelmäßig zu dem oben genannten Effekt.”

Alles klar?

Perfekt, Vielen Dank!

Ein sehr gut aufbereiteter Beitrag. Vielen Dank.

Aus meiner Sicht müsste auch das Alter berücksichtigt werden. Wer am Anfang der Rente steht, unternimmt viel und ist oft unterwegs, die sogenannten GoGo Years. Dann wir man ruhiger und bleibt in der Nähe , die sogenannten SlowGo Years. Ab 80=85 sind die NoGo Years dran. Über 30 Jahre braucht man mehr Geld zu Beginn und weniger am Schluss. Der lebensnahe Entnahmeplan ist also veränderlich. Am Anfang wird viel Geld benötigt, am Schluss wenig. Wie könnte der Entnahmeplan aussehen?

In diesem Fall könntest du dein Vermögen zu Beginn der Rente (z.B. 1 Mio. CHF) in mehrere Teilvermögen splitten. Das heisst, z.B. die ersten “teuren” 10 Jahre mit 500’000 CHF kalkulieren, die zweiten 10 Jahre noch mit 300’000 CHF und die “günstige” letzte Dekade schliesslich mit 200’000 CHF. Abgesehen davon könnte man bezüglich des Kostenverlaufs aber auch umgekehrt argumentieren:-) Nämlich so, dass es “hinten raus” immer teurer wird (Pflegekosten & Co. lassen grüssen…)

Whow, was für ein genial guter Beitrag, vielen DANK. Genau sowas hatte mir noch gefehlt. Auch Dankeschön für die Links. Habe das Excel gleich selber mal ausgetestet und da auch mit der TER gespielt. Bei 1 Mio. was ja mind. das Ziel wäre, macht das schon was aus. Der Sparkojote hatte ja vor kurzem ein Video darüber “diese Gebühren zerstören dein Depot”.

Ich frage mich nun aber, wieso er wie ihr ja auch den VWRL (TER 0.22) und nicht den VT (TER 0.07) im Depot habt. Da gibt es ja diverse Unterschiede wie Fonddomizil, Währung, Steuererklärung, etc. Vielleicht ist das mal ein Thema für ein Blog Beitrag für euch, diese zwei Gegenüber zu stellen mit allen Vor- und Nachteilen….

Merci fürs Lob, was uns natürlich sehr freut! (Umso mehr uns dieser Beitrag einiges an Hirnschmalz abverlangt hat:-) Zu deinem ETF-Vergleich: Beides sind natürlich Top-ETFs. Was u.a. für den VWRL spricht: Handelswährung CHF (Beim Kauf ist kein Währungswechsel nötig). Die TER ist zwar (auf tiefem Niveau) etwas höher, doch die für uns noch wichtigere Tracking Difference liegt bei gerade mal 0,02%. Solange es solch attraktive ETFs an der Heimbörse gibt, ziehen wir diese jeweils den US-Pendants vor.

Beste Grüsse

SFB