Newsletter

Newsletter

Why does a broadly diversified portfolio beat the supposedly smartest stock tip? The answer lies in one of the most powerful concepts of modern financial theory – and in the only real “free lunch” in investing. In this third lesson of our financial guide, you will find out how to use diversification effectively in two stages, where its limits lie and what this means for your wealth accumulation.

< Lesson 2 | Overview | Lesson 4 >

Short & sweet

- Diversification is the only “free lunch” in investing: You get the same return potential with less risk.

- Before you invest, you should meet two basic requirements: a nest egg of three to six months’ expenditure and no outstanding consumer loans.

- Level 1: Diversify your shares globally and across sectors – this will eliminate company-specific risk. Together with a solid nest egg, you are already well positioned.

- Level 2: If you want to go one step further, combine different asset classes – bonds, commodities and alternative investments can reduce fluctuations or open up additional opportunities for returns.

- With the core-satellite approach, you maintain discipline in the foundation and scope for targeted positions in the satellite.

- Stock picking can increase returns – but can also lead to a total loss. Even professional fund managers regularly fail to beat the market in the long term. This is why diversification is generally the more promising approach – and scientifically sound.

Contents

- Resisting the temptation of stock-picking

- What is behind diversification? The theory in a nutshell

- Diversification in practice – two stages

- The pragmatic middle way: the core-satellite approach

- The honest flip side: diversification vs. concentration

- Conclusion

- This might also interest you

- Updates

- Disclaimer

Resisting the temptation of stock-picking

Admittedly: It’s not easy to resist the supposedly safe stock tip with rosy profit prospects from a trusted acquaintance. But it’s definitely necessary! ![]()

“The hunt for individual stocks, also known as stock-picking, can backfire badly.“

If you invest in a single stock, substantial price losses with no prospect of a sustained recovery are unfortunately an all too realistic scenario. And it’s not just exotic stocks that are affected, but also well-known and established Swiss companies.

The Swatch Group, once a popular stock on the Swiss stock exchange, has lost around 70% of its value since its high in November 2013 – as the chart clearly shows.

The worst case is even more drastic: bankruptcy. Swissair, once the nation’s proudest airline, had to stay on the ground in October 2001 – shareholders lost everything. Investors in Credit Suisse did not fare much better: Once one of the largest banks in the world, it was taken over by UBS on an emergency basis for little money in March 2023 following a crisis of confidence. Shareholders lost practically everything.

Incidentally, the opposite of stock-picking is not necessarily passive investing – even actively managed funds often hold hundreds of stocks and are therefore broadly diversified. The actual counter-concept is the concentration on a few stocks. And it is precisely this concentration that increases risk – without increasing returns.

But concentration is not only evident in stock picking. Anyone who keeps their entire assets in a savings account is also concentrating on a single form of investment – with the difference that the threat here is not price losses, but a creeping loss of purchasing power due to inflation. And the compound interest effect, which makes the decisive difference in the long term, has virtually no effect. We showed how big this difference is over decades in lesson 1.

You can find out how diversification solves this risk – and what the science says about it – in the next chapter.

What is behind diversification? The theory in a nutshell

This brings us to Harry Markowitz’s Modern Portfolio Theory (MPT). He was awarded the Nobel Prize in Economics in 1990 for his groundbreaking doctoral thesis.

Markowitz was the first to provide theoretical proof of the positive effect of diversification on the risk and return of an overall portfolio. The core of his theory is the distinction between systematic and unsystematic risk.

All securities on the market are subject to systematic risk – i.e. market risks such as interest rate rises, recessions or political instability. It cannot be diversified away and is simply the price of investing itself.

The unsystematic risk, on the other hand, is the company-specific risk – such as management errors as in the VW emissions scandal. This risk can be reduced through diversification. And that is the key point: the market compensates you for the systematic risk – but not for the unsystematic risk. So if you invest in individual stocks, you are taking on unnecessary risk without being able to expect higher returns.

“Company-specific risk can be reduced through diversification – market risk cannot.“

You will achieve the strongest diversification effects if you combine investments with the lowest possible correlation. The range extends from +1 (same development) to 0 (independent development) to -1 (opposite development). Within the equity asset class, typical correlations are between 0.70 and 0.95 – the effect is real, but limited. The combination of different asset classes brings significantly more, as we will see below.

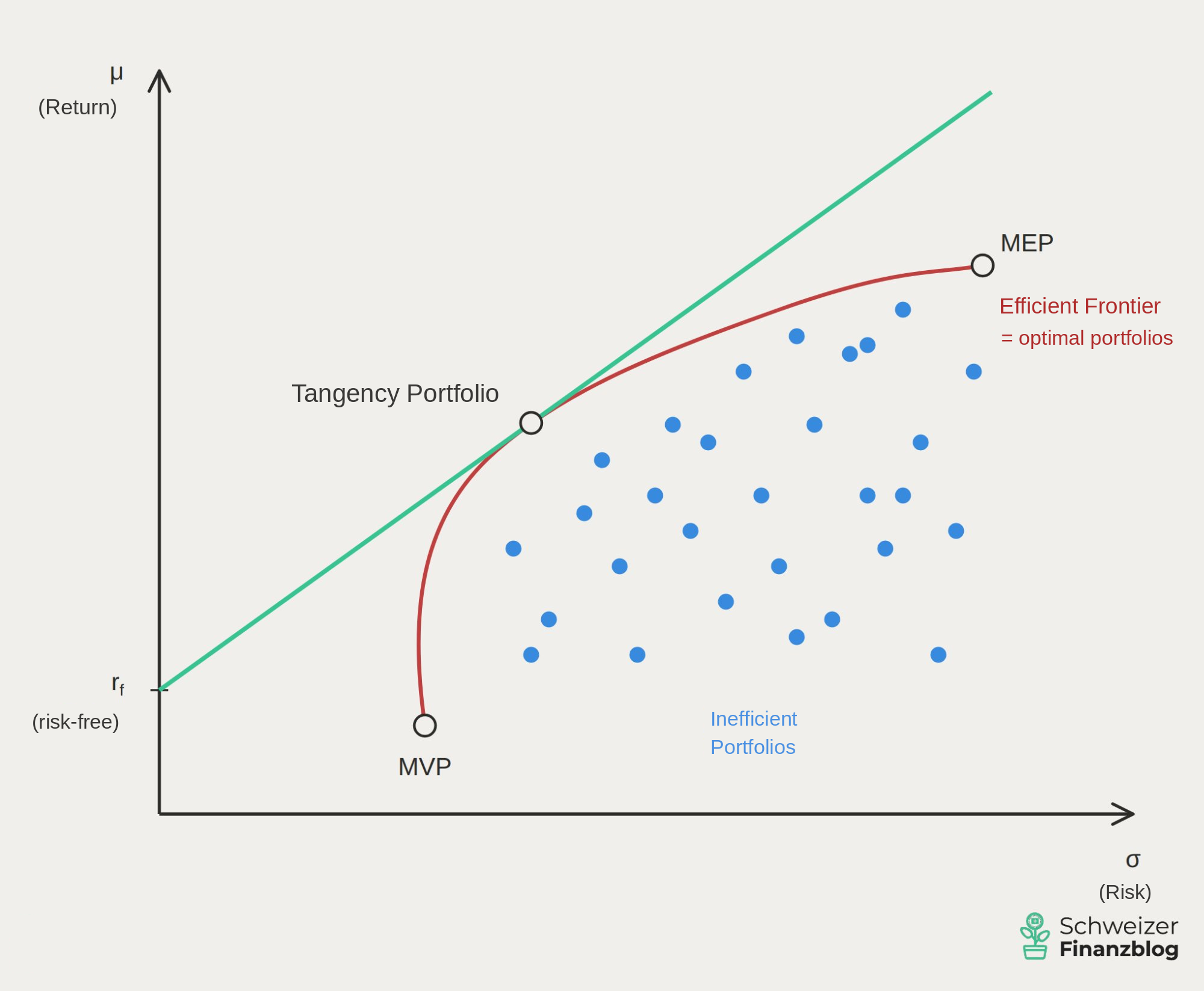

The efficiency line: what makes an optimal portfolio

Markowitz not only showed that diversification reduces risk – he also specified the minimum amount of risk that must be taken for a given return. The result is the efficient frontier.

The efficiency line is created by plotting all conceivable portfolio combinations in a diagram – with the risk on the x-axis and the expected return on the y-axis.

Portfolios on the curve are efficient: they achieve the maximum possible return for a given risk. Portfolios below the curve are inefficient – too much risk for too little return. Portfolios above the curve are simply not achievable.

“Diversification is the only free lunch in investing: same expected return – but less risk.“

A global equity ETF such as the FTSE All-World is close to the MEP – the maximum return portfolio at the upper end of the efficiency line. A single stock such as the Swatch Group, on the other hand, lies to the right of the curve: with the same or even lower expected return, you bear significantly more risk – without being compensated for it. This is precisely the “free lunch” of diversification: not more return, but less risk with the same expected return.

Diversification in practice – two stages

Theory is nice – but how do you put diversification into practice? And how far do you have to go? The old stock market adage that you shouldn’t put all your eggs in the same basket comes in two stages. But first you should fulfill an important prerequisite.

The nest egg. Before you invest, you should keep a bank balance of three to six months’ expenses as a liquidity reserve. This reserve serves to cushion unforeseen expenses – due to job loss, illness or repairs – without you having to touch your investments. Paying off any consumer loans also has priority, as their interest rates exceed any realistic return on investment. Only once you have built up this reserve and are free of consumer debt can you really invest the rest of your assets for the long term.

Level 1 – Diversification within the equity asset class

Let’s start with the most important level: broadly diversify shares. A simple rule of thumb helps with orientation:

- No-go: individual shares

If you only hold one share, you bear the full company-specific risk. Total loss – as with Swissair – is not a theoretical scenario. - Suboptimal: few Swiss stocks

Many people tend to overweight domestic stocks – the so-called home bias. Understandable, but structurally problematic: the Swiss market is heavily concentrated in three sectors (pharmaceuticals, financials, consumer goods) and accounts for less than 3% of global market capitalization. - Recommended: Global and cross-sector

A global ETF on the FTSE All-World or MSCI ACWI comprises thousands of companies from all over the world. The company-specific risk is practically eliminated – and you simply don’t care whether individual companies rise or fall in the index.

Caution: limited cluster risk also in ETFs

Anyone who buys an MSCI World ETF and thinks they are perfectly diversified should take a closer look: Around 70% of the index is made up of US equities, of which over 20% is made up of the seven largest technology companies alone (“Magnificent Seven”). In addition, the MSCI World only covers developed markets of large and medium-sized companies – emerging markets such as China, India or Brazil are not included. If you want real geographical diversification, you have two options: either supplement the emerging markets component with a separate ETF, or invest directly in an MSCI ACWI or FTSE All-World, which already include emerging markets. If you want to go one step further, add a small-cap ETF to your portfolio – and thus also include smaller companies.

The legislator also has diversification rules: For UCITS funds – the standard structure of most ETFs available in Switzerland – the so-called 5-10-40 rule applies: individual positions exceeding 5% of the fund assets may not account for more than 40% in total. UCITS is not a must, but a quality feature designed to protect investors. Other ETFs – such as those that track the best-known Swiss index SMI – do not meet the requirements, as Nestlé, Novartis and Roche together regularly make up more than 50% of the index. So if you want to invest in a well-diversified way, you should pay attention to the UCITS label.

Excursus: Currency risk – an issue for Swiss investors

If you invest globally, you automatically invest in foreign currencies – around 60% of a FTSE All-World consists of US dollar securities. The decisive factor here is not whether you buy your ETF in CHF or USD, but in which currency areas the companies in the fund operate.

Is that a reason to forego global diversification? No. In the long term, the diversification benefits clearly outweigh the disadvantages, and currency fluctuations are partially balanced out over time. Currency-hedged ETFs do exist, but they cost more and eat into returns in the long term. For most investors with a long-term horizon, the currency risk is simply bearable – and part of the package.

Conclusion on diversification level 1

In combination with a solid liquidity reserve in your bank account, you are already well positioned with level 1 – a global equity ETF covers the most important aspects. But if you want to go one step further – reduce fluctuations or tap into additional return opportunities – you can combine different asset classes. This is level 2.

Level 2 – Diversification across asset classes

The combination of different asset classes is even more effective than diversification within equities – because their correlations with each other are significantly lower than within the equity asset class. While equities from different markets still have correlations of 0.70 to 0.95, the correlations between equities and other asset classes are often significantly lower – in some cases close to zero or even negative. The lower the correlation, the greater the diversification effect.

Bonds

Bonds often move in the opposite direction to equities – in times of crisis, bond prices rise when everyone is looking for safety. However, this is not always the case: in 2022, both equities and bonds fell massively in value when the central banks drastically increased interest rates. Bonds are therefore not a panacea, but can be a valuable portfolio anchor over long periods of time.

A classic example is the 60/40 portfolio: 60% global equities, 40% bonds. For decades, this has been a proven starting point for people with a balanced investment approach – more stability, but also lower returns than with pure equity investments. Anyone with a long investment horizon and a focus on maximum growth will find bonds to be a drag on returns. The right weighting ultimately depends on the individual risk profile – precisely the topic of the next lesson.

Raw materials

Gold, oil and industrial metals often act as a hedge against inflation and have low correlations with equities. Gold in particular has acted as a safe haven in many crises. However, commodities do not generate current income such as dividends or interest.

Alternative investments as an admixture

Anyone wishing to expand their portfolio beyond traditional asset classes will find further sources of diversification in the area of alternative investments – with different return, risk and liquidity profiles.

- Real estate

Real estate ETFs are the most accessible entry into “concrete gold” – without a mortgage, condominium owners’ association or administrative expenses. They offer current income, but are sensitive to changes in interest rates and are not completely decoupled from the equity markets. - Crowdlending

P2P lending – direct lending to private individuals or SMEs via online platforms – can generate attractive returns. But the risks are real: during the coronavirus crash in 2020, several platforms froze payouts, and Estateguru ‘s returns plummeted from double digits to zero for many – high default rates on German real estate loans still weigh on the platform today. Conceivable as a small addition for risk-takers – not as a core component. - Collectibles

Collector’s items – Art, watches, whisky, sports cards – are considered inflation-resistant and have little correlation with financial markets. Investments from as little as EUR 50 are possible via platforms such as Splint Invest. The downsides: low liquidity, assets that are difficult to value and no ongoing income.

Conclusion on diversification level 2

All asset classes can be a useful addition to the portfolio – but none can replace the stable foundation of diversified equity ETFs. The golden rule: the more exotic the investment, the smaller its weighting should be.

The pragmatic middle way: the core-satellite approach

The core-satellite approach elegantly resolves the apparent dilemma between diversification and concentration. The idea is simple:

- Core – typically 70-90% of the portfolio

One or two broadly diversified ETFs – such as MSCI ACWI or FTSE All-World – form the stable foundation. There is no speculation here, assets are built up over the long term. People with a more balanced investment approach can also supplement the core with bonds. - Satellite – typically 10-30%

There is room here for targeted positions – individual countries or sectors, factor ETFs, individual shares or alternative investments such as real estate ETFs, P2P lending or collectibles. These positions can beat the market, but they don’t have to. Their loss does not jeopardize the overall portfolio.

The key advantage: you keep the discipline of diversification at the core without sacrificing the joy of active investing. And you always know what is at stake.

The honest flip side: diversification vs. concentration

Here’s a point that financial blogs often fail to mention because it seems to undermine the main message. But it is part of the truth:

Exceptional returns come from concentration, not diversification.

Warren Buffett achieved his excess returns by betting massively on a few carefully selected companies. Private equity funds also outperform the market – if they do – through concentrated bets. Anyone who had bet everything on Nvidia or Apple in the past would be rich today.

That sounds tempting – but it is not a realistic path for the vast majority. And for one simple reason: concentration not only increases the opportunities, but also the risks. For every Buffett, there are hundreds who have backed the wrong horse and suffered total losses. Excess returns through concentration require sound analysis, a robust psychological profile, a lot of time – and above all a considerable amount of luck.

For most private investors, diversification is therefore not the path to super returns – but it is the path to solid, risk-adjusted returns over decades. And that is exactly what sustainable wealth accumulation means in practice.

– Partner offer –

Still looking for the right financial solution? Our recommendations – with attractive starting bonuses.

– – – – –

Conclusion

Diversification is not a lazy compromise – it is the only proven “free lunch” in investing: same return potential, less risk. If you accumulate individual securities, you take on unnecessary risk without any corresponding return compensation. And if you park your assets in a savings account, you avoid price fluctuations – but you pay a different price: gradual loss of purchasing power due to inflation and lost compound interest.

Even the first stage – a global equity ETF combined with a solid liquidity reserve – forms a solid foundation. If you want to go further, you can also diversify across different asset classes – with a sense of proportion.

The core-satellite approach combines the best of both worlds: a stable foundation thanks to diversification and scope for targeted positions thanks to controlled concentration.

In the fourth lesson of this financial guide, we start right here and look at asset allocation – in other words, the question of how you distribute your total assets across the various asset classes in line with your individual risk profile.

You can find an overview of all the lessons here: Learning to invest – in eight lessons.

This might also interest you

Updates

2026-04-06: Article completely revised and updated.

Disclaimer

Disclaimer: Investing involves risks of loss. You must decide for yourself whether you want to bear these risks or not.

Errors excepted: We have written this article on investment diversification to the best of our knowledge and belief. Our aim is to provide you as a private investor with the most objective and meaningful financial information possible. However, if we have made mistakes, forgotten important aspects and/or are no longer up to date, we would be grateful if you could let us know.

8 Kommentare

Der Artikel ist wirklich sehr gelungen. Die Struktur ist klar, die Beispiele (Swatch, Swissair, Credit Suisse) treffen es auf den Punkt, und der Ehrlichkeit-Abschnitt zu Konzentration vs. Diversifikation hebt den Artikel nochmal ab. Das liest man nicht überall.

Weiter so!

Ein sehr gelungener und wichtiger Beitrag! Gerade in Zeiten, in denen an jeder Ecke vermeintliche „Geheimtipps“ für einzelne Aktien gehandelt werden, ist es entscheidend, die Risiken des Stock-Pickings realistisch einzuschätzen. Der Artikel erinnert eindrücklich daran, dass selbst traditionsreiche Schweizer Unternehmen wie Zürich Versicherung oder UBS keine Garantie für stabile Renditen sind.

Die klare Erklärung der Modernen Portfoliotheorie zeigt zudem, dass Diversifikation kein theoretisches Konzept ist, sondern in der Praxis über langfristigen Anlageerfolg entscheidet. Besonders gut gefällt mir der Hinweis auf den Unterschied zwischen systematischem und unsystematischem Risiko – ein Punkt, den viele Privatanleger oft unterschätzen.

Ich stimme der Kernaussage voll zu: Stock-Picking ist mehr Spekulation als Investition. Wer langfristig Vermögen aufbauen will, sollte breit diversifizieren – am besten global und über verschiedene Assetklassen hinweg. So wird aus Risiko-Reduktion eine echte Strategie.

Vielen Dank für den fundierten Kommentar! Es freut uns sehr, dass die Bedeutung der Diversifikation so klar rübergekommen ist – genau das wollten wir mit dem Beitrag erreichen.

Hallo zusammen

Wäre das ein gutes Portfolio bez. der Diversifikation?

60% HSBC MSCI World (IE00B4X9L533)

20% HSBC EURO STOXX 50

(IE00B4K6B022)

20% UBS MSCI Switzerland

(CH0226274246)

Gruss und Danke für das Feedback

Hoi Erwin

Mit dem MSCI World bist du in über 1600 Aktien der entwickelten Welt investiert, weshalb du alleine mit diesem Produkt sehr gut diversifiziert bist. Bei den anderen beiden Produkten erreichst du keine zusätzliche Diversifikation, da die Aktien dieser ETFs bereits im MSCI World enthalten sind. Möglicherweise ist es aber dein Wunsch, die Eurozone im Allgemeinen und die Schweiz im Speziellen bei deiner Anlage besonders stark zu gewichten (d.h. stärker als die entsprechende Marktkapitalisierung der Aktien aus der Eurozone und der Schweiz).

Was unseres Erachtens in deiner Aufstellung fehlt, sind die Emerging Markets, womit du Aktien von zusätzlichen 25 Ländern erreichst. Auch kannst du dir überlegen, ergänzend noch die “Small Caps” zu berücksichtigen, womit du dann – was die Anlageklasse Aktien betrifft – extrem gut diversifiziert wärest.

Beste Grüsse

SFB

Hallo zusammen

Vielen Dank für das Feedback.

Genau das war meine Idee/Wunsch mit Europa und der Schweiz, da ich davon ausgehe, dass die Wirtschaft in Europa sich in den nächsten Jahren besser entwickeln wird.

Bei dem Emerging Markets weiss ich nicht so recht. Dieser ist mir fast zu “China” lastig. Ansonsten wäre es eine Möglichkeit den MSCI World durch den iShares MSCI ACWI UCITS ETF (Acc) zu ersetzen. Somit hätte ich die Schwellenländer auch mit drin.

Beste Grüsse

…ja genau, den MSCI World ETF durch einen ETF ersetzen, welcher auf dem Index MSCI ACWI oder FTSE All-World (von Anbieter Vanguard) basiert, wäre ein prüfenswerte Option…

Paranoid vor einem Crash muss man nicht sein, doch wer sich nicht absichert und seine Asset Allocation absichert ist selbst schuld. Man kann weiter investieren und Investments halten die bei einer Rezension stark steigen. Auch andere Währungen wie der Schweizer Franken können eine Lösung sein.