Newsletter

Newsletter

Who wouldn’t want to escape the daily hamster wheel and become financially free? Financial freedom and independence – these dazzling terms are on everyone’s lips these days. But what do they actually mean? What factors are crucial for achieving financial freedom? You will find these and other answers in this article. ![]()

Let’s get straight to the point: Achieving financial freedom without inheritances and the like is definitely not a sprint, but a marathon. But there are also comforting aspects for “mere mortals”: It is not uncommon for average earners to manage to become financially free, while many high earners are unable to do so due to their lavish lifestyles combined with a lack of financial education.

Contents

- From quick riches straight to bankruptcy

- Financial freedom vs. financial independence

- What matters when it comes to financial freedom

- Examples of passive income

- Financially free – what now?

- How to become financially free in just 8.8 years

- Financially free with 20 times your annual expenditure

- Step by step to financial freedom

- Conclusion

- This might also interest you

- Disclaimer

From quick riches straight to bankruptcy

Just think of the numerous dramas of former multi-millionaires from the world of sport (see Watson article “Just standing at the bar and drinking – 22 football stars who went bankrupt”) and show business (an impressive example is Curtis Jackson, once the most successful rapper and better known as “50 Cent”; a bankruptcy court confirmed his bankruptcy in 2015, as well as his running costs of USD 108,000 – per month!) They all got into serious financial difficulties after their career peaks. Not to mention the numerous impoverished former lottery millionaires.

Financial freedom vs. financial independence

But what does financial freedom or independence actually mean?

In line with the FIRE movement (“Financial Independence, Retire Early”) and the frugalist scene, we adhere to the following definition:

Financial freedom = being able to live exclusively from passive income streams, without a budget, i.e. basically without restrictions on consumption.

Financial independence = being able to live exclusively from passive income streams, within the limits of previous expenditure.

Financial independence is therefore a preliminary stage of financial freedom. For the sake of simplicity, we will limit ourselves to the concept of financial freedom below. We therefore assume that all our financial needs and wishes can be covered by our current expenditure. The following therefore applies: financial freedom = financial independence.

What matters when it comes to financial freedom

“The goal of financial freedom is to be able to live off passive cash flows from investments.”

To become financially free, the following three steps must be repeated:

- Earn money

- Save money earned

- Invest saved money profitably

The aim is to be able to live off passive cash flows from investments and thus not be dependent on an employer (salary) or the state (pension).

Passive cash flows can take many forms, such as income from shares, real estate or P2P lending. What all cash flows have in common, however, is that they are not generated from active work, but are earned independently of your own time investment. This is such a central aspect of financial freedom, which is why we want to explain it in more detail in the following section.

Examples of passive income

For example, if someone has individual stocks in their equity portfolio, the income from them is often not of a passive nature. This is because these investors tend to be more or less involved with their portfolio: they study annual reports, attend general meetings, trade, reallocate stocks, etc. In other words, income in the form of dividends and realized price gains is generated through active work. Our recommendation: Buy-and-hold strategy with passive investments in broadly diversified equity ETFs(see our blog article “ETFs: The investment revolution”).

“Rental income generated through own property management and tenant support is not passive income.”

The situation is similar with real estate: rental income generated through own property management and tenant support is not passive income. Because here too, income in the form of rental income is offset by active work. Our recommendation: Buy and hold strategy with passive investments in broadly diversified real estate ETFs.

Finally, P2P loans. In other words, you play bank by granting loans to SMEs or private individuals. In return, you receive interest (and bear the default risk). Interest income, which is subject to active risk management such as checks on the borrower and their financing project, is not passive, but involves (often nerve-wracking) work. Our recommendation: Choose a P2P platform that allows you to grant loans with just a few clicks and dispense with interactions with the borrower. In addition, risk diversification should be automatic or system-based, i.e. without you having to invest countless small amounts. (In our opinion, the Swiss platform “Creditgate24” pursues an interesting approach by means of automatic risk diversification or with its solidarity contribution concept).

Financially free – what now?

Once you have achieved financial freedom, you can basically do whatever you want: explore the world, pursue your hobbies, devote yourself to your family or, of course, continue to work. The latter with the decisive additional freedom to simply leave if it no longer suits you.

“For us, financial freedom is primarily a question of being rather than having.”

From this perspective, we consider financial freedom to be a goal worth striving for (with certain reservations, as we will show in the conclusion below). For us, financial freedom is primarily a question of being (i.e. living in freedom) rather than having (in the sense of having a lot of money), even if the one does not exclude the other.

– Partner Offer –

In our experience and due to the low costs for ETFs, a particularly attractive broker at present is “DEGIRO” (link to the DEGIRO Review). Bei Interesse kannst du dich bei DEGIRO über unseren partner link to get trading credits of 100 CHF (with conditions) and support our blog at the same time.

– – – – –

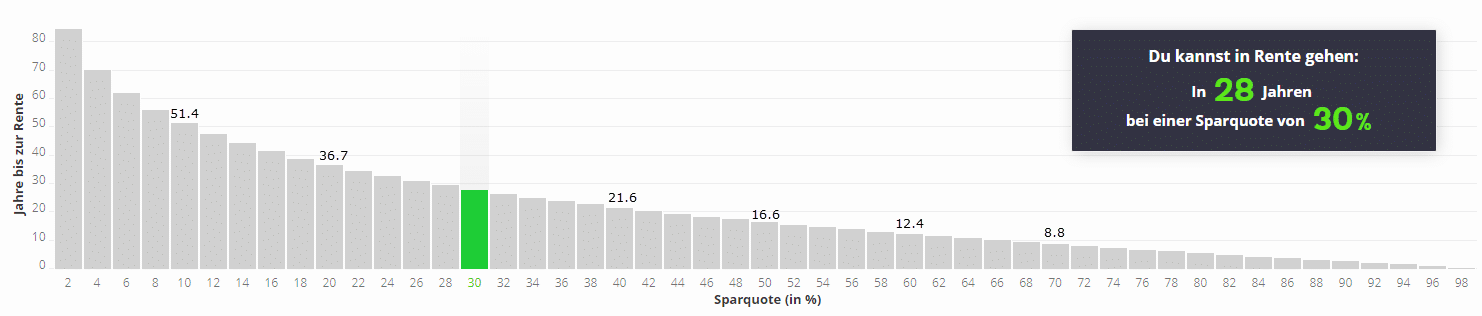

How to become financially free in just 8.8 years

As already mentioned, the three factors of income, saving and investing play a role in financial freedom. Basically, the less money you need to live on, the more you can save and invest from your income – and the faster you can live off the investment income from your assets.

These three factors can be summarized in the following two influencing factors:

- Savings ratio: savings amount in relation to active income

- Investments: broadly diversified and profitable investments

A high savings rate is likely to be much more difficult to achieve: This is because it is associated with sacrifice or a frugal lifestyle. In contrast, broadly diversified and potentially profitable investments using passive equity ETFs are very easy to achieve with just a few clicks (see this article).

Oliver Noelting, probably the best-known frugalist in the German-speaking world, who has set himself the goal of retiring before 40, has set up a corresponding calculator on his blog Frugalisten.de. As Figure 1 below impressively shows, the individual retirement age can be reached earlier and earlier as the savings rate increases. With a savings rate of 70%, for example, in just 8.8 years!

The calculations are based on the following simplifying assumptions:

- Your expenses remain constant – now and during the retirement phase

- Income and return (5%) are net amounts (after tax)

- All monetary amounts are adjusted for inflation

Financially free with 20 times your annual expenditure

This means that you would need to have invested 20 times your annual expenditure in order to live off the income afterwards. With annual expenditure of CHF 50,000, you would therefore need an ETF portfolio worth CHF 1 million. Important: Returns in the context of shares or share ETFs are always made up of dividends and price increases. This means that passive income in this case consists of dividend and/or sales income.

“If the focus is not on capital preservation (and heirs), but on generating as much passive income as possible for the rest of your life, the path to financial freedom can be significantly shorter.”

If we also assume that equities yield an average return of 8%(see our blog article “Why investing is better than saving”) and average inflation does not exceed 3%, this 5% rule does not erode the real value of assets. In other words, if the focus is not on capital preservation (and heirs), but on generating the highest possible passive income for the rest of your life, the path to financial freedom can be significantly shortened.

This assumes constant net returns, which is of course not realistic. Even with a broadly diversified global equity portfolio, more or less strong fluctuations are realistic. Depending on whether positive or negative returns result at the beginning of the withdrawal phase, you will end up with an inflation-adjusted capital gain or loss.

If you are confronted with negative extreme situations or so-called black swans such as the global economic crisis from 1929 onwards at the beginning of the withdrawal phase, this can even lead to premature complete capital depletion. Our 5% rule should therefore be seen as a rule of thumb (see also our response to Oliver’s input in the comments section below).

In the article “Withdrawal plans: How to take early retirement with peace of mind“, we present different variants of early retirement financing based on historical data.

Step by step to financial freedom

It can be motivating for you on your way to financial freedom if you draw up a list of all important expenses, such as health insurance or taxes, and cross out those that you can finance with passive income.

Or you can determine the days that you are already financially free. Based on the example above, this means: If your passive income currently amounts to CHF 10,000, you are financially free for an impressive 73 days (365 * 10,000 / 50,000) per year. Or perhaps even more motivating: every time your passive income increases by 137 francs (50,000 / 365), you will be financially free for one additional day a year, for the rest of your life!

Conclusion

We are of the opinion that financial freedom is definitely worth striving for. After all, it can provide a secure and comfortable lifestyle . But for most people, complete financial freedom remains a pipe dream. The sacrifices are too great and the expensive extras too dear. You must also be aware that on the path to financial freedom – from a purely financial point of view – you are “sacrificing” your life now for the future. We want to draw a differentiated conclusion to financial freedom in the spirit of a conciliatory conclusion:

For those who are unwilling or unable to save, financial freedom is neither attainable nor desirable.

At the other end of the spectrum are the hardcore savers, the so-called frugalists. These contemporaries indulge in an extremely modest lifestyle in terms of consumption/materialism, often with a good income and equally good financial education. They naturally have the best prerequisites for achieving financial freedom.

For the majority, including the authors, who do not belong to either group, there is an interesting middle way: continuously expand your passive income through conscious spending behavior and regular investments (e.g. in broadly diversified ETFs) and thus gradually reduce your financial dependency on third parties, be it your employer or the state.

For example, if your passive income reaches 20 percent of your current expenses, you could also reduce your workload by 20 percent. You can then “invest” the time you gain in family, hobbies or simply doing nothing, depending on what you like. That’s already a great start!

This might also interest you

Disclaimer

Disclaimer: Investing involves risks of loss. You must decide for yourself whether you want to bear these risks or not.

Errors excepted: We have written this article to the best of our knowledge and belief. Our aim is to provide you as a private investor with the most objective and meaningful financial information possible. However, should we have made any errors, forgotten important aspects and/or no longer have up-to-date information, we would be grateful if you could let us know.

2 Kommentare

Hallo liebe Schweizer Finanzblogger,

ihr schreibt, dass bei einem Aktienportfolio, das durchschnittlich mit real 5 % (8 % minus 3 % Inflation) rentiert, auch eine konstante Kapitalentnahme von 5 % im Jahr möglich ist (ohne Kapitalverzehr). Das ist jedoch falsch. Ganz im Gegenteil hätte eine solche Entnahme sogar ein ziemlich hohes Risiko für einen frühzeitigen Bankrott. Der Grund ist das Sequence-of-Returns-Risiko, das bei der reinen Betrachtung der Durchschnittsrendite unberücksichtigt bleibt:

https://frugalisten.de/das-sequence-of-returns-risiko-entnahmestrategien-teil-2/

In der FIRE-Community wird deshalb typischerweise eher mit Werten zwischen 3 und 4 % (sogar mit Kapitalverzehr) gerechnet, siehe auch die “4 %-Regel”:

https://frugalisten.de/die-4-prozent-regel-wie-viel-geld-brauchst-du-um-nicht-mehr-arbeiten-gehen-zu-muessen/

https://frugalisten.de/william-bengen-trinity-wahrscheinlichkeiten-entnahmestrategien-teil-3/

Hoi Oliver

Vielen Dank für deine Mitteilung und die verlinkten Artikel zum Thema.

Die 4-Prozent-Regel kennen wir natürlich, sie ist uns aber etwas zu konservativ. (“German Angst” lässt grüssen:-) Deshalb haben wir in unserem Artikel die 5-Prozent-Regel erwähnt, und zwar basierend auf empirischen Daten und der Voraussetzung eines global gestreuten, d.h. mutmasslich weniger volatilen Aktien-Portfolios. Gemäss der von dir im Link erwähnten Trinity-Studie besteht für eine 30-jährige 5%-Entnahmeperiode eine Erfolgsquote von 85%, und zwar bezogen auf ein nicht global gestreutes S&P 500-Portfolio und unter Berücksichtigung der bisher wohl schlimmsten Weltwirtschaftskrise, welche den S&P-Index von 1929 bis 1932 um über 70% zusammenstauchte.

Solche Extremereignisse bzw. sogenannte “Schwarzen Schwäne”, wie auch dein fiktives Beispiel mit ebenfalls vier aufeinanderfolgenden Jahren mit Negativrenditen zu Beginn der Entnahmeperiode, können selbstverständlich zu einem vorzeitigen vollständigen Vermögensverzehr führen. Und bei einem Zusammenbruch des kapitalistischen Systems taugt selbst die superkonservative 3-Prozent-Regel nichts mehr….

Uns ging es jedoch um eine Faustregel, nicht um eine wasserdichte Entnahmestrategie, welche es ja ohnehin nicht gibt, da niemand die Zukunft bzw. die “Schwarzen Schwäne” voraussehen kann. Diesbezüglich haben wir unseren Artikel aufgrund deines Inputs präzisiert.

Mit bestem Dank und Gruss

Schweizer Finanzblog