Newsletter

Newsletter

Your portfolio is set, your asset allocation is in place—and then the markets do whatever they please. Prices rise, fall, and fluctuate. Suddenly, your portfolio no longer matches your risk profile. Does it have to be this way? Not necessarily. In this fifth lesson of our financial guide, you’ll learn how to rebalance your portfolio with minimal effort—and when you can skip that step entirely.

< Lesson 4 | Overview | Lesson 6 >

Short & sweet

- Rebalancing means adjusting your portfolio back to your target weighting after market fluctuations – no more and no less.

- If you hold a single global ETF and a fixed amount of Swiss francs as a low-risk component, you do not need rebalancing.

- It becomes relevant if the low-risk portion is defined as a percentage or if different asset classes in the portfolio perform differently.

- Checking once or twice a year is sufficient – readjustment is only worthwhile if there is a deviation of 5 percentage points or more, ideally via new deposits rather than sales.

- The so-called rebalancing bonus can bring a small additional return, but is a welcome side effect – the real argument remains risk control.

Contents

What is rebalancing – and do you even need it?

In the last lesson, you learned how to divide your assets into a high-risk and a low-risk part. The foundation of your portfolio is now in place. But the markets don’t stick to your plan: prices rise and fall, and the weightings shift with them. Rebalancing means restoring the original allocation.

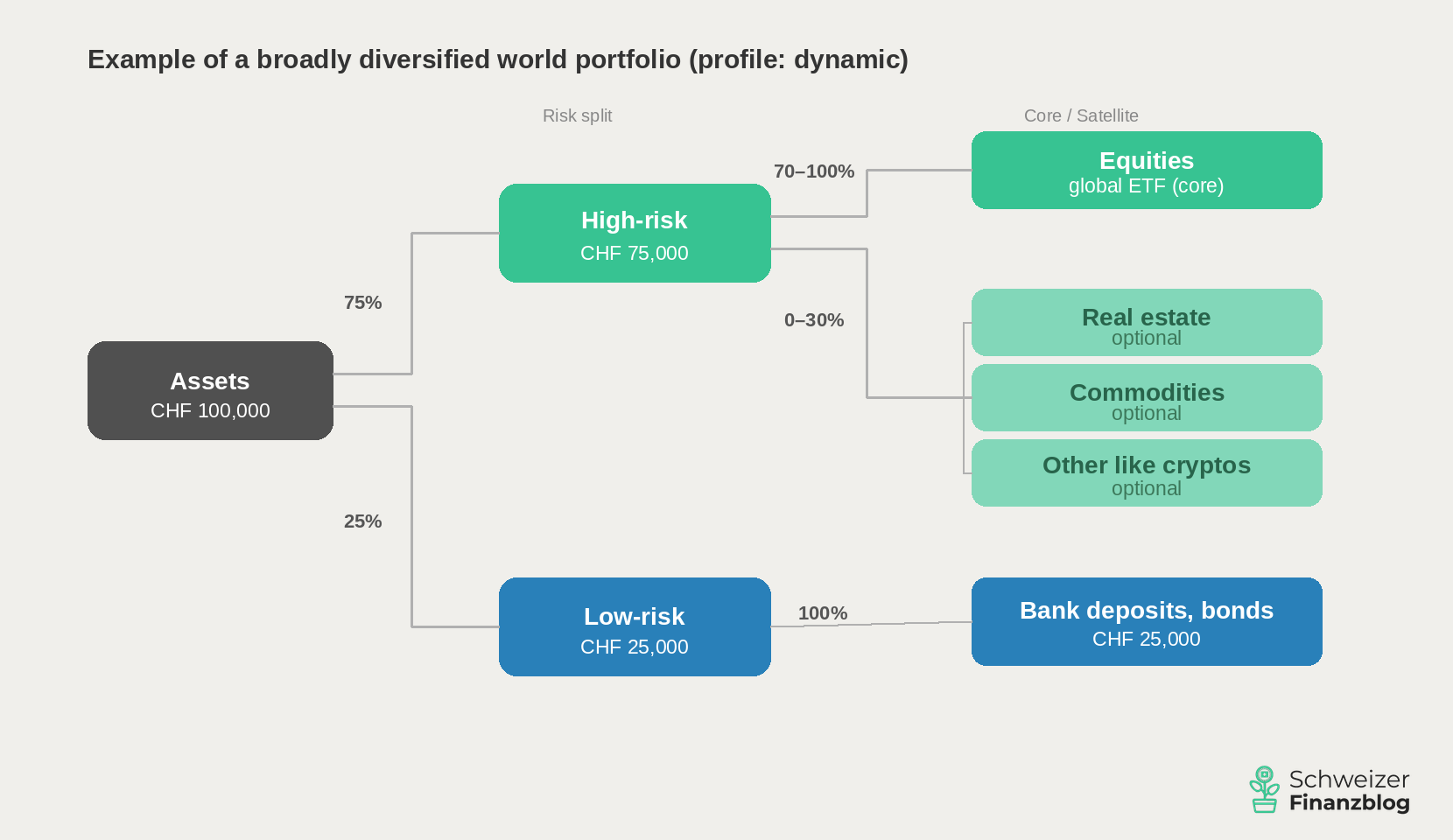

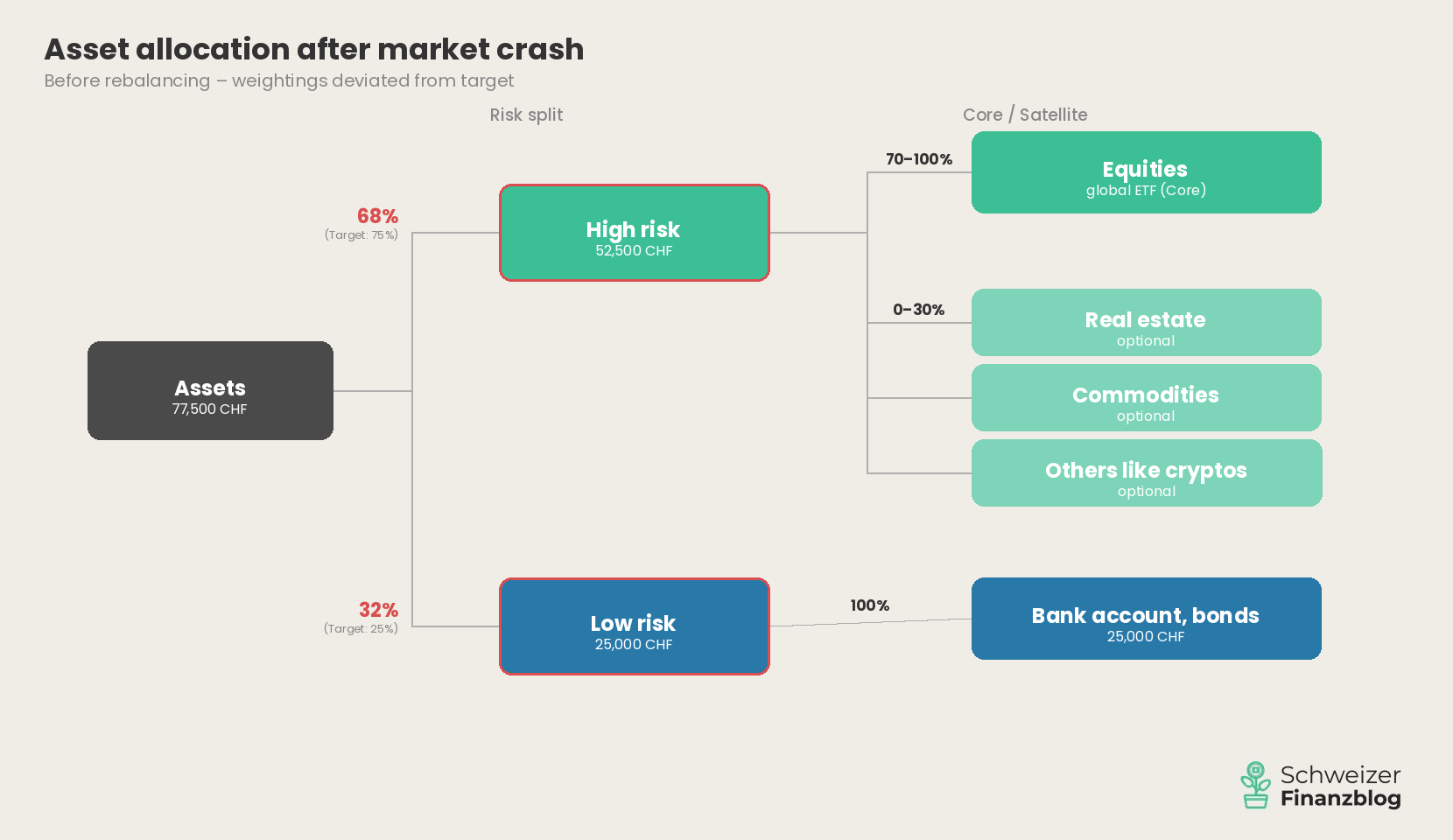

An example: You have invested CHF 100,000 – 75% high-risk, 25% low-risk.

Now the stock markets collapse by 30%. Your risky portion falls from CHF 75,000 to CHF 52,500, while the CHF 25,000 in your savings account remains unchanged. Your total assets now amount to CHF 77,500 – and the low-risk portion is suddenly 32% instead of 25%. Your portfolio is much more conservative than you had planned.

To get back to 75/25, you would have to shift around CHF 5,600 from your savings account to the risky part – after a crash, of all times, when your gut feeling is against it. This is exactly what rebalancing is: a sober, rule-based correction that brings your portfolio back into line with your risk profile.

When you don’t need rebalancing

But before you go creating a rebalancing schedule: Not every portfolio needs this adjustment. If you hold a single global ETF and define the low-risk portion as a fixed amount in Swiss francs—e.g., CHF 25,000 in a savings account, excluding emergency funds—you simply have nothing to rebalance. The ETF is continuously adjusted internally by the provider. And a fixed amount doesn’t shift, no matter what the markets do. In the event of the same market crash, your CHF 25,000 stays where it is. Your high-risk portion has shrunk, but your risk profile hasn’t changed—and that’s the logic behind the fixed amount in Swiss francs. No action needed.

Rebalancing therefore becomes relevant if the low-risk portion is defined as a percentage (as in the example above) or if the portfolio consists of several ETFs, such as in a core-satellite approach. In both cases, the weightings drift apart over time – and you have to actively readjust them. We will now take a look at how this can be done pragmatically and cost-effectively.

Rebalancing in practice: how to bring your portfolio into balance

Two questions arise: When should you rebalance? And how?

When to rebalance?

In theory, there are two approaches: calendar-based and threshold-based. With the calendar-based approach, you review your portfolio at fixed intervals – about once a year. With the threshold-based approach, you only take action if a deviation exceeds a certain value, e.g. 5 percentage points.

In practice, you can combine the two: You check your portfolio once or twice a year – and only intervene if the deviation is large enough. That’s enough. Rebalancing is not a daily business, but an occasional adjustment.

Three ways to bring your portfolio back into balance

There are basically three methods to bring your portfolio back in line with the target weighting:

- Rebalancing: You sell investments that are above their target weighting and use them to buy underweighted positions. Classic, but associated with transaction costs.

- Cash Flow Rebalancing: You direct new deposits—such as your monthly savings—specifically toward underweighted positions. No selling required, no additional costs. For investors in the accumulation phase, this is the most elegant approach—and it’s the one we follow as well.

- Combination: In the event of minor deviations, readjust by making new deposits. Only in the event of major shifts do you actively reallocate.

Perfection is out of place

If you balance every position down to the last franc, you’ll end up paying unnecessarily high transaction fees—especially on smaller amounts. Focus on the largest deviations. Once the overall allocation between the high-risk and low-risk portions is back in balance, you can safely ignore minor imbalances within the high-risk portion. You can simply realign them during your next contribution. As a rule of thumb: if a position deviates by more than 5 percentage points from its target weighting, action is warranted. Below that, the effort is usually not worth it.

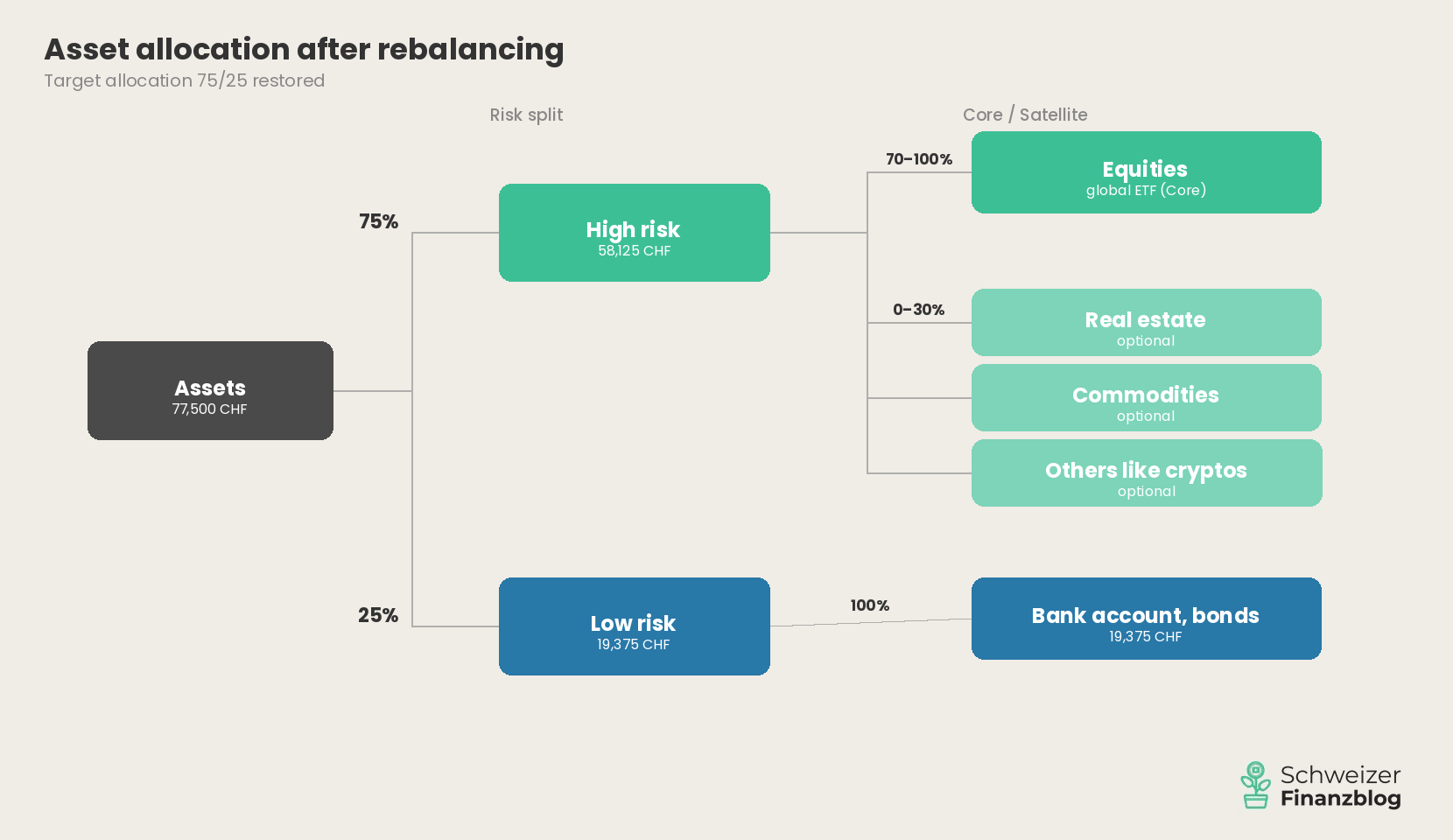

The following graphic shows what this looks like in concrete terms.

Good to know: Rebalancing in the deconsolidation phase, 3rd pillar and taxes

De-savings phase

What has been described so far relates to the accumulation phase – i.e. the time in which you build up your assets. But you can also rebalance your assets when you retire. The principle is simply reversed: Instead of targeting new deposits, you first sell positions that are above their target weighting. In this way, you bring your portfolio closer to the target weighting with each withdrawal – without additional transactions.

3rd pillar

If you hold part of your assets in the 3rd pillar: Rebalancing is usually automated here. You enter your risk profile once, and the provider handles the rebalancing for you—often already included in the management fees. However, you still need to take care of rebalancing your freely available assets yourself.

Taxes

Rebalancing generally has no tax consequences for private investors in Switzerland. Capital gains on private assets are tax-free. The only exception: anyone who trades so frequently and on such a large scale that the tax authorities suspect commercial securities trading must pay tax on gains as income. This is not an issue for one or two rebalancing transactions per year.

The rebalancing bonus: a welcome side effect

The main aim of rebalancing is clear: to bring your portfolio back in line with your risk profile. However, there is a pleasant side effect that is known in specialist literature as the rebalancing bonus.

The principle behind it is simple: with rebalancing, you systematically buy investments that have fallen and reduce those that have risen. You are therefore acting anti-cyclically – and it is precisely this behavior that can generate a small additional return in the long term. Various studies put this effect at around 0.1 to 0.5 percentage points per year.

The honest flip side

The rebalancing bonus is not a law of nature. It works best when prices return to the mean after spikes – the so-called regression to the mean. In phases with long-lasting trends, however, rebalancing can slow you down because you sell winners too early. None other than Charlie Munger, Warren Buffett’s partner of many years, firmly rejected rebalancing for precisely this reason: systematically cutting winners slows down the growth of your portfolio.

On top of that, there are transaction costs. With an expensive primary bank, those costs can quickly eat into the savings. The rebalancing savings are therefore only worthwhile with a low-cost online broker that charges low fees per transaction.

Therefore: See the bonus as a welcome extra, not as a guarantee.

“The real argument for rebalancing is not the additional return – but risk control.“

– Partner offers –

Still looking for the right financial solution? Our recommendations – with attractive starting bonuses.

– – – – –

Conclusion

Rebalancing is not a third major investment principle alongside diversification and asset allocation – but the maintenance that ensures that your portfolio remains in line with your risk profile even after market fluctuations.

If you keep it simple – a global ETF and a fixed amount of Swiss francs in your savings account – you don’t need to worry about this. For everyone else: check once or twice a year and readjust if there are major deviations, preferably by making new deposits rather than selling. Perfection is out of place – as long as the overall allocation is correct, you can safely ignore minor imbalances.

In lesson 6, we take a closer look at the investment vehicle that crops up again and again in this guide: the ETF. What’s behind it – and why are we talking about a revolution in private investment?

You can find an overview of all the lessons here: Learning to invest – in eight lessons.

This might also interest you

Updates

2026-06-12: Minor adjustments made.

2026-04-14: Article completely revised and updated.

Disclaimer

Disclaimer: Investing involves risks of loss. You must decide for yourself whether you want to bear these risks or not.

Errors excepted: We have written this article on rebalancing to the best of our knowledge and belief. Our aim is to provide you, as a private investor, with the most objective and meaningful financial information possible. However, if we have made mistakes, forgotten important aspects and/or are no longer up to date, we would be grateful if you could let us know.