Newsletter

Newsletter

In this article, we want to introduce you to an asset class that is still relatively unknown in Switzerland but is growing rapidly: Crowdlending, also known as peer-to-peer (P2P) or marketplace lending. In this first article, you will find out what P2P loans are and how the Swiss market presents itself. We draw on the latest Crowdfunding Monitor Switzerland 2019 from Lucerne University of Applied Sciences and Arts.

Contents

What Crowdlendig (P2P Switzerland) is and how it works

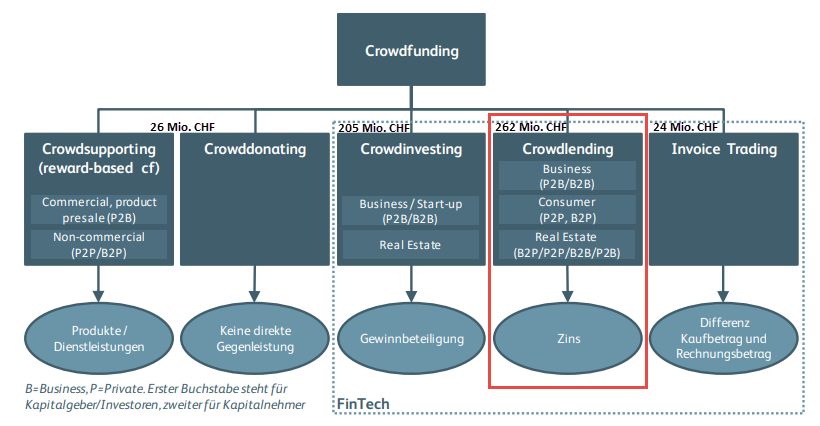

Crowdlendig is one of five categories of crowdfunding and, at around CHF 262 million, has the largest loan volume (see Figure 1)![]()

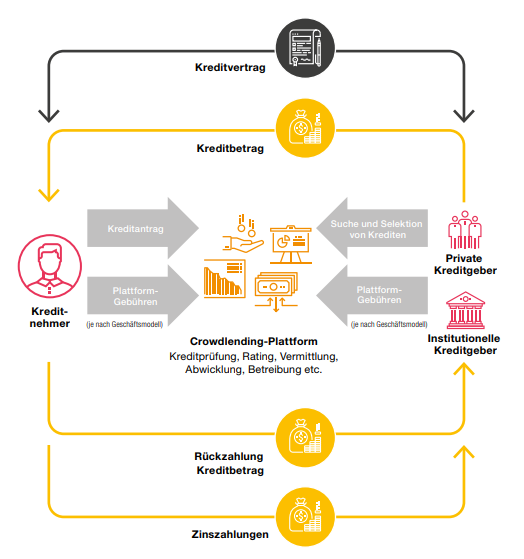

Crowdlending involves the financing of companies or private individuals through loans (borrowed capital). In contrast to traditional lending, there is no intermediary bank in crowdlending. Instead, the loans are arranged online via a platform. For a fee, the provider of such a marketplace usually takes on the risk assessment of the borrower as well as the entire debt collection process, including payment reminders, dunning letters and debt collection.

In return for granting the loan, you as the lender receive interest payments, the amount of which essentially depends on the credit risk, the loan term and the type of loan. Figure 2 below shows the interaction between the various players in the crowdlending system in simplified form.

In addition to private and SME loans, mortgages are also granted to private individuals in Switzerland without an intermediary bank. Loans to private individuals are also referred to as consumer crowdlending, while loans to companies are referred to as business crowdlending. The term real estate crowdlending is also used for loans in the form of mortgages. As different as these variants may be in detail, they all have one decisive and cost-efficient feature: there is no need for an expensive bank as an intermediary.

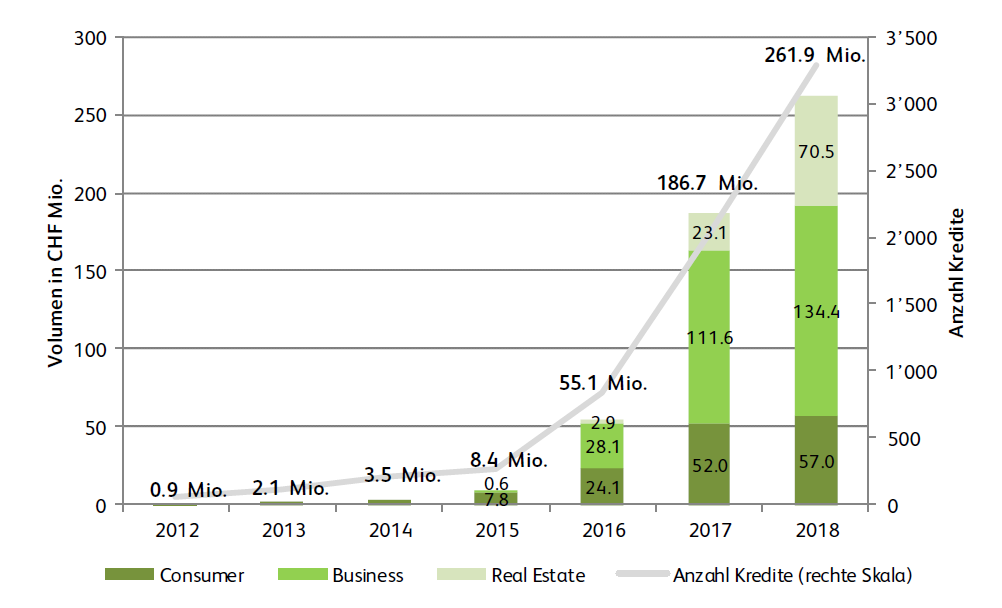

Within the crowdlending category, SME loans account for the lion’s share at CHF 134.4 million. This is followed by real estate loans (70.5) and consumer loans to private individuals (57) (see Figure 3). At 1.3% (2018), the latter are still marginal in relation to the overall consumer credit market.

How the Swiss market presents itself

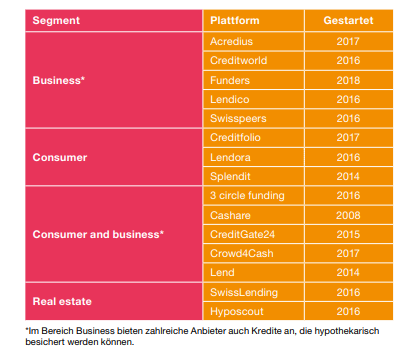

The first so-called P2P platform was founded in Switzerland back in 2008 with the provider Cashare. At the end of 2018, the Swiss market was much more diverse with a total of 15 active platforms (see Figure 4).

The platforms usually focus on one or two segments of crowdlending. In the business and consumer crowdlending segment, there are also providers that offer mortgage-backed loans. Business crowdlending platforms are typically aimed at small to medium-sized enterprises (SMEs). Consumer crowdlending platforms are active in the consumer credit market.

The growth momentum in terms of the number of new platforms has decreased significantly. In 2018, only one new crowdlending platform, Funders, entered the Swiss market.

Although it was only launched in 2015, CreditGate24 is clearly the largest crowdlending platform in terms of loan volume (as of 2019).

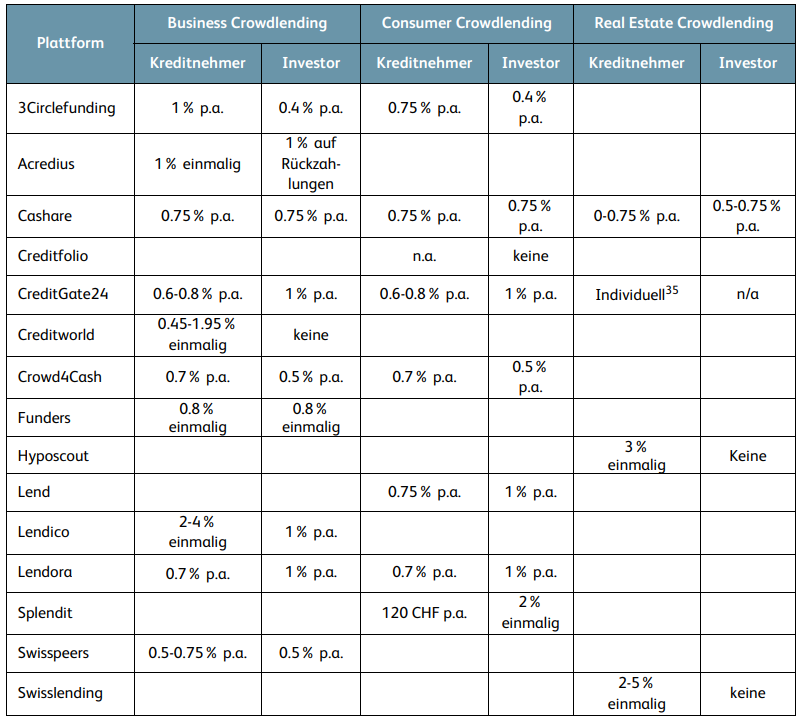

How the platforms finance themselves

The fees in crowdlending usually relate to the amount of the loan (see Figure 5). Fees are often incurred on the lender and borrower side. Depending on the platform, these can be incurred both at the time of conclusion and over time. The ranges are correspondingly high and the fee models are sometimes difficult to compare.

– Partner Offer –

In our experience and due to the low costs for ETFs, a particularly attractive broker at present is “DEGIRO” (link to the DEGIRO Review). Bei Interesse kannst du dich bei DEGIRO über unseren partner link with which you can earn Trading Credits of 100 CHF (with conditions) and support our blog at the same time.

– – – – –

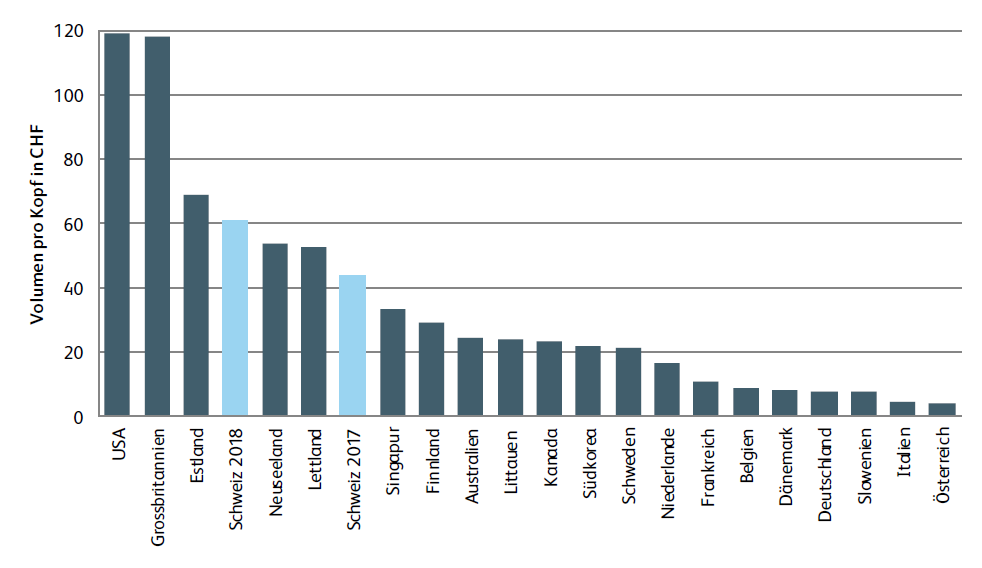

Switzerlandis at the forefront ofinternationalcomparison

Looking at the crowdfunding volume per capita in an international comparison, Switzerland is one of the more relevant markets worldwide. As Figure 6 shows, Switzerland is in 7th place (2017), far behind the leaders USA and the UK, but surprisingly well ahead of our neighbors. It should be noted that the figures relate to all categories of crowdfunding (see Figure 1), i.e. not just crowdlending.

Theses on crowdlending

Based on the Crowdfunding Monitor 2019, the following market theses can be derived for crowdlending:

- Sustained growth

Crowdlendig grew by around 40% in Switzerland in 2018. Continued growth in the double-digit percentage range is also expected for the coming years. - Market concentration and market shakeout

The trend towards market concentration of three to five providers will become even more pronounced. This is because there are still too many platforms in Switzerland that are online but have only financed very few projects to date. These will disappear again in the short to medium term. On the other hand, market entries are likely to become increasingly rare. - Crowdlending is moving away from the basic idea

In crowdlending, more and more platforms are carrying out transactions between borrowers and lenders without a public tender and many loans are no longer financed by a swarm, but by a single professional investor. This reduces the importance of private individuals.

This might also interest you

Disclaimer

Disclaimer: Investing involves risks of loss. You must decide for yourself whether you want to bear these risks or not.

Errors excepted: We have written this article to the best of our knowledge and belief. Our aim is to provide you as a private investor with the most objective and meaningful financial information possible. However, should we have made any errors, forgotten important aspects and/or no longer have up-to-date information, we would be grateful if you could let us know.

4 Kommentare

Vielen Dank für den guten Artikel, was wäre denn deine Empfehlung für einen Schweizer P2P Anbieter?

Guten Tag Tinki

Merci für dein positives Feedback! Erfahrungen mit Schweizer P2P-Anbietern haben wir mit Cashare (Toni: nicht empfehlenswert, da Rendite gegen 0% tendiert; Klumpenrisiko) und Creditgate24 (Stefan: prüfenswert) gesammelt. Bei Creditgate24 gefällt insbesondere die automatisierte Risikostreuung mittels Solidarbeitrag. Vorteil: kein Klumpenrisiko bzw. relativ stabile Erträge; aktuell liegt die Rendite bei gut 4%, vor Corona bei rund 5% bei einem über alle Bonitätsstufen gemischtem Portfolio).

Beste Grüsse SFB

Also Cashare habt ihr wohl nicht so gut getestet. Wie kann man dort auf 0% kommen? Und was versteht ihr unter Klumpenrisiko? Das liegt doch echt nicht an der Plattform sondern am Investor Toni! Ich fahre bei Cashare mit Grundpfand gesicherten Krediten rund 8,5% ein und von den gesicherten Krediten ist noch nie einer weggebrochen!

Super spannend! Ich hätte nich gedacht dass die Schweiz so dicht am Baltikum in Bezug auf P2P ist! In Sachen Rendite liegen die Baltischen Plattformen aber noch weit vorne. Auch die Usability und Aufbereitung für die Steuern ist dort weiter vorangeschritten, da die Plattformen in der Regel deutlich älter sind. Mein Favoriten sind dabei Mintos und Bondora – wo es sogar eine Tagesgeld Funktion mit 6,75% Zins gibt. Ganz liebe Grüsse von Eric