Newsletter

Newsletter

We Swiss are often said to be good with money. But do we really live up to this reputation in an international comparison? And how is the savings of Mrs. and Mr. Swiss actually distributed among private households? Do we save in general or is saving limited to the high income brackets? You can find the answers to these questions in this article.

Contents

The Swiss save around a fifth – only China saves more

A look at the latest OECD data, which compares the savings rates of private households in more than 30 OECD countries, seems to confirm the Swiss’s alleged propensity to save: After all, with a savings rate of 18.8% (2016), Switzerland is in second place worldwide behind China (2015: 37.1%), followed by Sweden (2016: 16.6%) and far ahead of countries such as Germany (2016: 9.7%), Austria (2016: 7.9%) and the USA (2016: 5.0%). ![]()

These values are in relation to disposable household income. Compulsory savings in the form of mandatory occupational pensions, which Switzerland – unlike the USA, for example – has, are not included. Swiss households therefore have an above-average, voluntary propensity to save compared to other countries.

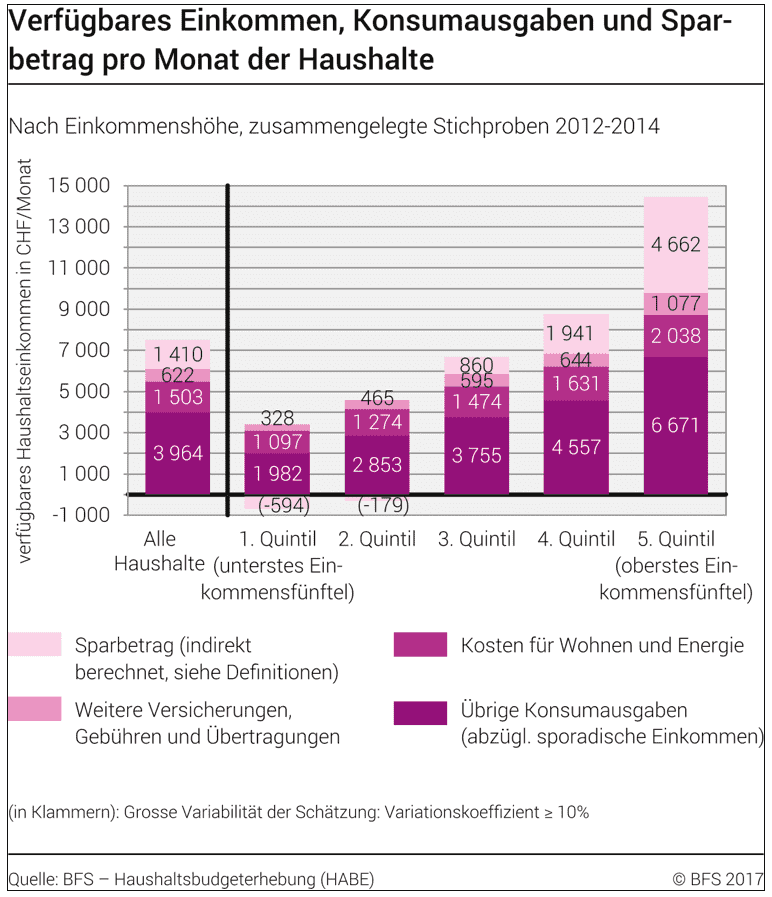

Four-figure savings on the high side – every month!

What does this mean in concrete terms, i.e. how many francs can Swiss households put aside? According to the Federal Statistical Office, the average (voluntary) savings amount for the years 2012 to 2014 is exactly CHF 1,410 per month and household (see Figure 1).

– Partner Offer –

Saving is before investing: According to our experience and due to the low costs for ETFs, “DEGIRO” is currently a particularly attractive broker (link to DEGIRO review). If you are interested, you can register with DEGIRO via our partner link, which will give you trading credits of CHF 100 (with conditions) and support our blog at the same time.

– – – – –

40 percent of Swiss households do not save

If we take a closer look at the sample, it is noticeable that the propensity to save among Swiss households varies greatly and – unsurprisingly – depends on income. The 40 percent (1st and 2nd quantile) households with the lowest incomes even have a negative (!) savings amount. Only from the third quantile onwards does the monthly savings amount become positive at CHF 860, rising sharply from CHF 1,941 (4th quantile) to CHF 4,662 (5th quantile or top fifth of income).

Conclusion

We Swiss may be remarkable savers from an international perspective and based on average figures, but this picture is put into perspective when looking at the savings rate per household and income bracket: to put it bluntly, we can summarize that half of Swiss households save and the other half live more or less from hand to mouth.

In the next blog post, we want to explore the question of what happens to the money saved in times of historically low interest rates and take a closer look at the financial situation of Mr. and Mrs. Schweizer.

You can get a complete overview of the topic of “Investing” here: Learning to invest – in eight lessons.

2 Kommentare

Toller Beitrag! In Deutschland ist die Sparquote so hoch, weil es historisch gefördert wurde. Doch heute mit Null- oder gar Minus-Zinsen wird man dadurch (und durch durch Inflation) beim Sparen enteignet. Ein Umdenken zum Investieren, weg vom Sparen ist daher notwendig. Das Geld also nicht einfach auf dem Konto liegen lassen, sondern dann auch in Vermögenswerte wie Qualtitätsaktien oder Gold investieren. Ob sich das 2020 noch lohnt und ob Vermögenswerte in CHF bei einem eventuellen Euro-Crash noch sicher sind…? Darüber schreibe ich auf meinem Blog. LG Eric

Spannender Beitrag. Ich spare, zum Beispiel mit einem Vergleich der Krankenkasse indem ich diese wechsle um weniger für Beiträge zu zahlen Dann gebe ich das Ersparte wiederum für Ferien oder Ähnliches aus.