Newsletter

Newsletter

Over 2,000 ETFs on the SIX Swiss Exchange alone – how can you find the right one? The good news is that with a few clear criteria, the choice is reduced to a manageable selection. The even better news: For most investors, a single ETF is enough. In this 7th lesson of our financial guide, you will find out which criteria really count, how you can systematically clear the ETF jungle and how you can select the right ETF for you.

< Lesson 6 | Overview | Lesson 8 >

Short & sweet

- Choosing the right index is more important than choosing the ETF product: a broadly diversified, market capitalization-weighted equity index forms the basis.

- A single global ETF – such as the FTSE All-World or the MSCI ACWI – is sufficient for a complete global portfolio.

- The main selection criteria are low costs (TER), a convincing tracking difference, a high fund volume and physical replication.

- ETF providers that rely on MSCI indices should not be combined with those that use FTSE indices – otherwise there is a risk of gaps or overlaps in the portfolio.

- Currency hedging should be avoided for a long-term investment horizon for cost reasons.

Contents

- Not all ETFs are the same

- Finding the right ETF – the index comes first

- Choosing the right ETF: The most important criteria

- What the name of an ETF reveals

- The topic of currency

- Distributing or accumulating?

- Investing sustainably with ETFs

- Which ETF is right for me?

- Conclusion

- This might also interest you

- Updates

- Disclaimer

Not all ETFs are the same

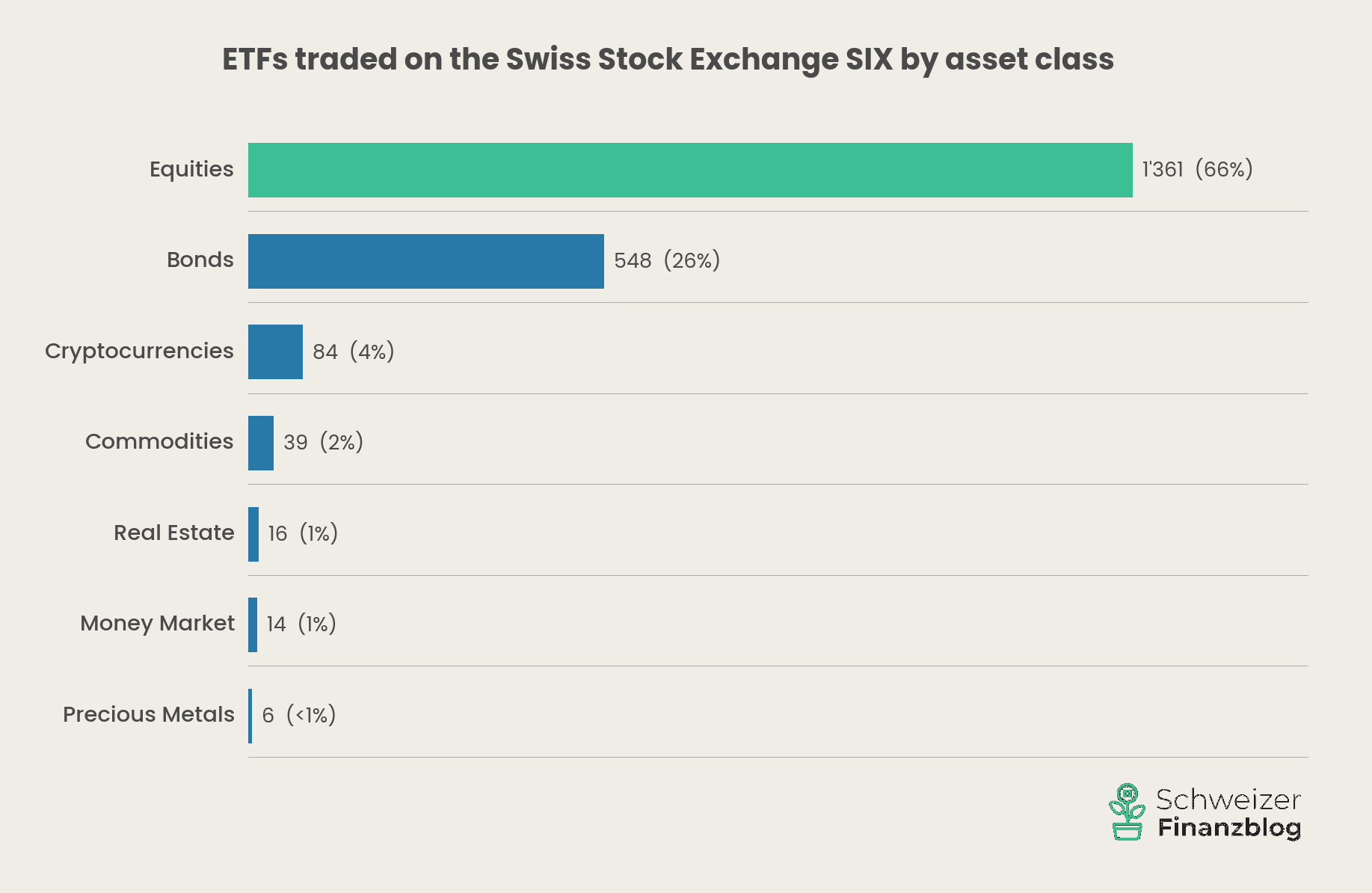

In lesson 6, you learned what ETFs are and why they are the ideal investment vehicle for you. But not all ETFs are the same. The universe is huge – and covers far more than just equities. On the Swiss stock exchange SIX alone, you can find over 2,000 ETFs on a wide range of asset classes: Equities, bonds, real estate, commodities and even cryptocurrencies. There are also ETFs that focus on specific sectors, themes, strategies or factors.

To build your portfolio, it is therefore crucial to choose the right category – before you start looking at individual products.

Bread-and-butter ETFs as the core of your portfolio

For long-term wealth accumulation – and this is our assumption in this guide – broadly diversified equity ETFs that track a global index by market capitalization are best suited as the basis of your portfolio. We do the same. These so-called core or bread-and-butter ETFs invest in thousands of companies and form the foundation of a solid global portfolio. Some providers also label these products explicitly: iShares, for example, uses the label “Core” for its standard products, as opposed to “Edge” for specialized and thematic ETFs.

In our ETF comparison Best ETFs Switzerland and Global, we focus exclusively on such core products – and they are also the focus of this lesson.

Specialist ETFs as satellites

There are also ETFs that invest specifically in individual sectors (e.g. technology), factors (e.g. small caps, value), strategies (e.g. dividends) or themes (e.g. clean energy, artificial intelligence). These products are narrower, less diversified and often more expensive – but can be interesting as a targeted addition.

This is where the core-satellite strategy, which we introduced in lesson 3, comes into play: The core of your portfolio consists of one or a few broadly diversified ETFs. The satellites are optional additions that you can use to deliberately focus on a specific region, theme or asset class such as real estate. If you are interested in factor-based approaches such as small caps or value, you can find an in-depth analysis in our article Is factor investing worth it?

Important: The satellites are optional, not mandatory. If you want to save yourself the effort, a pure core portfolio is just as good – often even better, because it is simpler and cheaper.

In the following chapters, we focus on the core: Which index do you choose and what criteria can you use to select the right ETF?

Finding the right ETF – the index comes first

The index determines which markets, regions and companies you invest in. The ETF itself is just the vehicle – the index is the tax. Therefore, if you want to find the right ETF, don’t start with the product, but with the index. As you learned in lesson 3, broad diversification is the key to a robust portfolio. In terms of index selection, this means that indices that cover entire regions or the whole world are preferable to a narrow country or sector index.

One ETF is enough – the simplest solution

If you want to keep things as simple as possible, choose a single global ETF that covers both developed and emerging markets. Two indices are suitable for this:

The FTSE All-World comprises over 4,200 large and medium-sized companies from around 50 countries. Its counterpart from MSCI, the MSCI ACWI (All Country World Index), covers a similarly broad market with around 2,500 positions. The even broader MSCI ACWI IMI variant also includes smaller companies (small caps) and has over 8,000 positions.

With a single ETF on one of these indices, you have a complete, market capitalization-weighted global portfolio – without having to worry about weightings between regions. It couldn’t be simpler.

Two ETFs – developed world and emerging markets separately

If you want to control the weighting between industrialized and emerging markets yourself, combine two ETFs: one on the developed world (e.g. MSCI World or FTSE Developed World) and one on the emerging markets (e.g. MSCI Emerging Markets or FTSE Emerging Markets).

Regional division – for more control

If you want to reduce the US dominance in the MSCI World – where US equities currently account for around 70% – you can divide the developed world into individual regions: North America, Europe and Asia-Pacific. As there is no single ETF for the Asia-Pacific region due to supply constraints, you need two: one for Asia-Pacific excluding Japan and one for Japan. Together with an emerging markets ETF, this results in a global portfolio of five to six ETFs – depending on whether you also want to add a Switzerland ETF.

This variant offers more control over the regional weighting, but also means more effort when rebalancing (see lesson 5).

MSCI or FTSE – but please don’t mix them

The two major index providers – MSCI (USA) and FTSE Russell (UK) – cover the global equity markets differently. Specifically, they do not always classify individual countries in the same way. For example, FTSE classifies South Korea and Poland as developed markets, while MSCI (still) classifies both countries as emerging markets.

This sounds like a detail, but it has practical consequences: Anyone combining an ETF on the FTSE Developed World with an ETF on the MSCI Emerging Markets would have South Korea and Poland in their portfolio twice. Conversely, these countries would be completely absent from the MSCI World + FTSE Emerging Markets combination.

“Choose an index provider – MSCI or FTSE – and stick with it.“

The simple rule: stick with one index provider. If you use MSCI for the developed world, also choose MSCI for the emerging markets – and vice versa. With a single global ETF, the question does not arise anyway. You can find a detailed comparison of the country classifications of both providers in our ETF comparison.

Home bias: Why Swiss indices alone are not enough

Some people instinctively bet on the domestic stock market. But the best-known Swiss index, the SMI, contains only 20 stocks – Nestlé, Roche and Novartis together account for around 45%. This is the opposite of diversification. The broader SPI (Swiss Performance Index) with over 200 stocks is better, but remains a pure country index. In addition, neither the SMI nor the SPI are UCITS-compliant – there is less product diversity and competition than with global indices.

Swiss indices are therefore not suitable as the sole basis for a portfolio. Swiss equities are already represented in a global ETF such as the FTSE All-World with around 2% – so you are already there. If you still want a Swiss finish, for example to deliberately increase the proportion of Swiss francs in the portfolio, you can add a Swiss ETF as a satellite. However, this is a deliberate overweighting – and not a must. You can find specific products for this in our ETF comparison.

In lesson 3, we explained why a strong home bias is one of the most common and most expensive investment mistakes.

Choosing the right ETF: The most important criteria

Once you have decided on an index, it’s time to choose a specific product. This is because there are often dozens of ETFs from different providers on the same index. The good news is that with a few clear criteria, the field of ETF selection can be systematically narrowed down. In our ETF comparison Best ETFs Switzerland and Global, we apply a strict, multi-stage selection process – in the end, only a handful of products make it to the final. The most important criteria at a glance:

Costs (TER)

The Total Expense Ratio (TER) indicates the ongoing annual costs of an ETF. It is charged directly to the fund assets and continuously reduces your return. The lower the TER, the better. Today, you typically pay between 0.10% and 0.20% per year for broadly diversified global ETFs. ETFs with a TER of over 0.25% can hardly be justified for broad market indices.

Tracking difference – the underestimated key figure

The tracking difference is even more informative than the TER. It measures how much the actual performance of an ETF deviates from its benchmark index – and thus shows the overall picture: including additional income, for example from securities lending, which can partially or fully compensate for ongoing costs. A negative tracking difference means that the ETF has slightly outperformed its index despite the costs.

You will often not find the tracking difference directly on the providers’ factsheets. But you can derive it by comparing the fund performance with the index performance. Alternatively, you can use the platform trackingdifferences.com. As a rule of thumb, the tracking difference should be in the range of the TER – or even lower. If it is significantly higher, this indicates hidden costs.

Fund size

Although the ETF market is growing rapidly, ETFs are regularly closed or merged. Your invested money is not lost – it is protected as special assets – but the process is cumbersome and can incur costs. However, the main argument for a large fund volume is a different one: large ETFs are traded more frequently, which leads to narrower spreads and therefore lower trading costs for each purchase and sale.

If you want to be on the safe side, you should choose an established ETF – with a large fund volume. In our ETF comparison, we assume a minimum volume of CHF 500 million.

Replication method

There are basically two options available to you: Physically replicating ETFs actually buy the shares contained in the index – either in full or as an optimized selection (sampling). Synthetic ETFs, on the other hand, replicate the index via a swap with a counterparty, which entails additional risk. Synthetic ETFs are a discontinued model; we avoid them.

Issue date

An ETF should be on the market for at least five years. Only then can meaningful performance comparisons be made and the tracking difference assessed over a longer period of time. A newly launched ETF may be cheap – but whether it keeps its promises in the long term can only be assessed after a few years.

Fund domicile

The domicile of an ETF has tax consequences. For persons from Switzerland, ETFs domiciled in Ireland are generally the most favorable from a tax perspective, followed by Luxembourg. This is due to the double taxation agreements that affect the withholding tax burden. In practice, the domicile of the most common ETFs on MSCI or FTSE indices is almost always Ireland or Luxembourg – so you rarely have to actively worry about this.

You can find more detailed information in our article ETF taxes Switzerland: Optimize your portfolio with these 5 tax-saving tips.

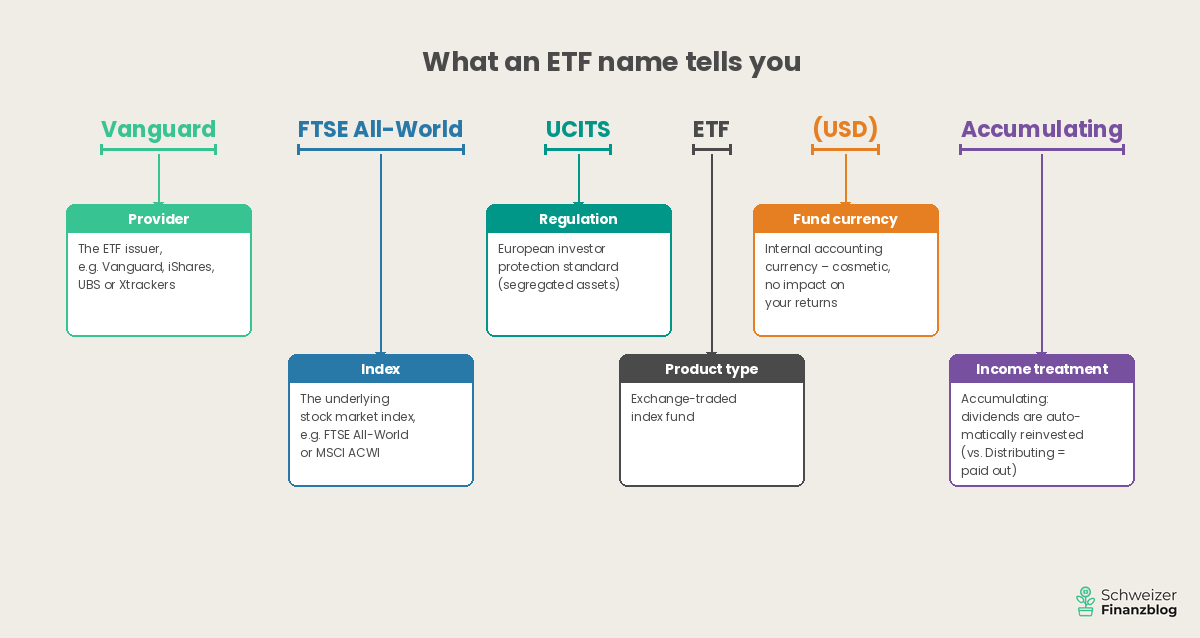

What the name of an ETF reveals

ETF designations seem cryptic at first glance, but they follow a clear pattern. Let’s take a concrete example:

Vanguard FTSE All-World UCITS ETF (USD) Accumulating

- Vanguard – the ETF provider (also: issuer)

- FTSE All-World – the underlying index

- UCITS – the ETF complies with European fund regulation (investor protection standard)

- ETF – exchange-traded index fund

- (USD) – the fund currency (see the “Currency” section below)

- Accumulating – reinvesting, i.e. dividends are automatically reinvested (in contrast to “distributing” = paying out)

If you know these components, you can decode any ETF name within seconds. In our article Understanding ETF abbreviations: 1C, UCITS, MSCI & Co. explained simply, you will find a detailed overview of all common abbreviations.

The topic of currency

When it comes to currency, there is a regular need for clarification in our community – understandably so, as there are three different currency levels:

The fund currency is the settlement currency of the ETF. It is often stated in the name (e.g. “USD” or “CHF”). The fund currency is cosmetic: whether the ETF calculates internally in USD or CHF does not change your return. However, there is a practical difference with distributing ETFs: the fund currency determines the currency in which the dividends are paid out.

The trading currency is the currency in which you buy and sell the ETF on the stock exchange. Many ETFs can be traded on SIX in both CHF and USD. If you buy in CHF, you save the costs of currency exchange with your broker.

The security currency is the currency in which the individual shares in the ETF are listed – i.e. US dollars for Apple, euros for ASML, yen for Toyota. You cannot influence this level, and this is precisely where the much-discussed currency risk lies: if the dollar loses value against the franc, the franc value of your US positions will fall – even if the share prices in dollars remain stable. Important: This risk is exclusively related to the security currency, not the fund or trading currency.

Why currency hedging is unnecessary

Some ETFs offer currency hedging. This sounds like less risk, but it comes at a price: in addition to an often higher TER, there are implicit costs resulting from the interest rate difference between the currencies. In the case of the Swiss franc against the dollar, these costs can add up considerably over the years.

For people with a long-term investment horizon, currency hedging does not generally make sense. Experience shows that over periods of ten years or more, currency fluctuations largely balance each other out. However, you pay the hedging costs every year – regardless of whether the Swiss franc rises, falls or moves sideways.

Our advice: avoid currency hedging and save yourself the costs.

Distributing or accumulating?

There are two options to choose from for the appropriation of profits:

Distributing ETFs pay out the dividends collected to your account on a regular basis – typically quarterly or semi-annually. You see the incoming payments and are free to decide what to do with the money.

Accumulating ETFs automatically reinvest the dividends in the fund. The money remains in the ETF and continues to work immediately. You do not see any incoming payments, but the price of the ETF rises accordingly.

We prefer accumulating ETFs for long-term asset accumulation. The reason: automatic reinvestment makes optimum use of the compound interest effect – without you having to be active. You also save the transaction costs that are incurred when reinvesting distributions manually.

However, distributing ETFs can certainly make sense – for example, if you want regular income or want to use the distributions specifically for rebalancing (see lesson 5).

The choice is irrelevant for tax purposes in Switzerland: dividends are subject to income tax in both cases – regardless of whether they are distributed or reinvested.

Investing sustainably with ETFs

If sustainability is important to you when investing, the ESG aspect (environmental, social, governance) also plays a role in the question “which ETF is right for me?”. There is now a growing selection of ETFs that filter companies according to environmental, social and corporate ethical standards.

However, the ESG market is confusing: there is no uniform definition of “sustainable” and the differences between providers are considerable. Some ESG ETFs only exclude the most obvious offenders (e.g. arms manufacturers, coal), while others filter much more strictly and reduce the investment universe significantly – with corresponding effects on diversification.

In our guide, we focus on standard ETFs without ESG filters, as these are more broadly diversified and generally have lower costs. If you are interested in sustainable ETFs, you can find a detailed analysis in our article Green stocks: 40 ETFs compared.

Which ETF is right for me?

Let’s summarize. If you want to choose an ETF that fits your global portfolio, these points are the most important:

- Index first: Choose a broadly diversified, market capitalization-weighted equity index. For most investors, a single global ETF is the best solution.

- Keep costs low: Look for a TER of no more than 0.25% and a tracking difference that is as close to zero as possible – or even negative.

- Size counts: A fund volume of CHF 500 million or more provides security and liquidity.

- Physically replicating: Avoid synthetic ETFs.

- No currency hedging: In the long term, hedging products cost more than they bring.

- Do not mix index providers: Either MSCI or FTSE – consistently.

This gives you the tools you need to find the right ETF from the huge range of ETFs on SIX. In our detailed ETF comparison Best ETFs Switzerland and globally, we have done just that: In a strict, multi-stage selection process, we combed through the entire offering and chose the best products.

– Partner offer –

Still looking for the right financial solution? Our recommendations – with attractive starting bonuses.

– – – – –

Conclusion

Choosing the right ETF for you is not rocket science – if you know what’s important. The index determines where your money goes; the product criteria ensure that as little of it as possible is lost along the way. And for the simplest option, a single, broadly diversified ETF covering the whole world is enough.

In lesson 8, we get down to business: we show you step by step how to buy your first ETF via an online broker – from opening a custody account to placing your first order.

You can find an overview of all the lessons here: Learning to invest – in eight lessons.

This might also interest you

Updates

2026-04-24: Article completely revised and updated.

Disclaimer

Disclaimer: Investing involves risks of loss. You must decide for yourself whether you want to bear these risks or not.

Errors excepted: We have written this article about choosing the right ETF to the best of our knowledge and belief. Our aim is to provide you as a private investor with the most objective and meaningful financial information possible. However, should we have made any errors, forgotten important aspects and/or no longer have up-to-date information, we would be grateful if you could let us know.

24 Kommentare

Hallo zusammen,

zuerst einmal vielen Dank für eure transparenten und gut recherchierten Artikel!

Ich bin Auslandschweizer (DE) und überlege mir, ob ich mein zZ. in der CH aktiv verwaltetes Depot in ein passives Depot mit ETFs umwandle. Gründe dafür:

– Aktiv verwaltet bedeutet hohe Steuern, da bspw. in DE auch Verkäufe besteuert werden und nicht nur die Renditen.

– Viel Kosten für Steuererklärungen, -auszüge, Doppelbesteuerung etc.

In DE haben wir bereits ein passives Depot und haben gute Erfahrungen damit gemacht. Nun ist meine Frage:

– Ist es “besser”, sich in der CH ein passives Depot z.B. bei Swisspquote aufzubauen und keinen Währungsumtausch zu machen bzw. weiterhin im CHFr. inverstiert zu bleiben, mit weniger Inflation, weniger Währungsschwankungen ODER

– den Währungsumtausch in EUR zu vollziehen, an deutschen Börsen die ETFs kaufen und das Depot in DE aufzubauen – was steuerlich am einfachsten wäre, aber eben mehr Inflation, weniger Stabilität, aber ev. bessere Kaufbedingungen an den dt. Börsen bietet.

– oder spielt es keine oder kaum eine Rolle, da das Kapital einvestiert ist?

Ich bin in diesen Fragen etwas überfragt und freue mich auf Antworten. Beste Grüße,

Heinrich

Hoi Heinrich

Wenn du investiert bist, hängt das Währungsrisiko primär mit der Herkunft der in diesem Fonds befindlichen Unternehmungen zusammen und nicht damit, ob du deinen ETF in EUR oder CHF gekauft hast. Also wenn du beispielsweise in einen ETF investiert bist, der den MSCI World mit rund 70% US-Unternehmen abbildet, so besteht das Währungsrisiko zu einem grossen Teil im Verhältnis USD und deiner Referenzwährung, unabhängig davon, ob deine Handelswährung EUR oder CHF ist.

Beste Grüsse

SFB

Hmmm… man kann selbstverständlich auch zu sehr in die Details gehen, ohne, dass es vermutlich viel bringt. Jedoch bin ich der Meinung, dass mit wenigen (<3-5 Titeln) keine wirklich breite Diversifikation möglich ist; zu sehr gibt es m.E. dann trotzdem Klumpen (z.B. durch zu grossen USA Anteilen). Deshalb gefällt mir dieses Portfolio an ETF mit entsprechenden Portfolio-Anteilen gut und bin gespannt auf eure Meinungen (selbstverständlich erwarte ich keine Anlageempfehlungen, aber kritische Anmerkungen, Alternativvorschläge zur Titelauswahl etc. sind willkommen):

*Nordamerika (25%) – Vanguard FTSE Emerging Markets

*Europa (25%) – iShares Core MSCI Europe

*"Home Bias" (5%) – UBS ETF (CH) SPI Mid (CHF)

*Asien-Pazifik ohne Japan (10%) – Vanguard FTSE Developed Asia Pacific ex Japan

*Japan (5%) – iShares Core MSCI Japan IMI

*Schwellenländer (15%) – Vanguard FTSE Emerging Markets

*Immobilien ohne USA – (10%) Vanguard Global ex-US Real Estate ETF

*Immobilien USA (5%) – iShares US Property Yield

Es sei noch erwähnt, dass weder Courtagen noch Depotführungsgebühren für mich relevant sind, da ich über eine Konzernzugehörigkeit in den Genuss äusserst attraktiver Vorzugskonditionen komme (somit ist das Thema "Trading Bank" auch erledigt)

Freundliche Grüss, Guido

…das scheint uns eine sinnvolle Aufteilung zu sein. Jetzt benötigst du nur noch einen langen Anlagehorizont (>10 Jahre) und die nötige Portion Standfestigkeit bei künftigen Börsenturbulenzen… Viel Erfolg!

Danke. Das wünsche ich uns allen! 🙂

Vielen Dank für diesen wertvollen Artikel. Leider scheint mir bei eurer Entscheidungshilfe kein einziger nachhaltiger ETF dabei zu sein. Gibt es hier eurerseits auch Auswertungen? Ich denke, es handelt sich hierbei um ein wichtiges Kriterium.

Hoi Chelsea

Ja, es gibt unsererseits Auswertungen von nachhaltigen ETFs. Schau’ doch mal in den Artikel “Grüne Aktien: 40 ETFs im Vergleich” rein. Da wirst du bestimmt deine grünen Wunsch-ETFs finden:-)

Beste Grüsse

SFB

Hallo zusammen

Vielen Dank für eure hilfreichen Artikeln!

Ich versuche euren Hinweis am Anfang des Artikels besser zu verstehen, dass “ETFs auch an ausländischen Börsenplätzen erwerben, was jedoch steuerlich etwas aufwändiger sein kann.”

– Was bedeutet “steuerlich etwas aufwändiger sein kann” genau?

– Was sind Beispiele von Vor- und Nachteilen ETFs an der Schweizer Börse zu kaufen?

– Was sind Vor- und Nachteile ETFs an den ausländischen Börsen z.B. Euronext Amsterdam (EAM) und Xetra (XET) im Portfolio zu haben?

Wie würdet ihr die Fragen beantworten um die Auswahl des Börsenplatzes besser verstehen zu können.

Besten Dank und liebe Grüsse

Hoi Larissa

Vielen Dank für deine interessante Mitteilung. Vorweg: In Bälde werden wir das Steuerthema in einem separaten Artikel vertiefen. Zu deinen Fragen:

– Es handelt sich hier um eine Kann-Formulierung und selbst diese scheint uns aus heutiger Sicht zu stark. Steuerlicher Mehraufwand könnte allenfalls resultieren, wenn du an einer Fremdbörse einen ETF kaufst, welcher die Steuerverwaltung (noch) nicht gelistet hat. In diesem Fall ist eine manuelle Eingabe des ETF-Produkts in der Steuererklärung nötig. (Normalerweise ist es ja so, dass die steuerrelevanten ETF-Daten mit Eingabe der Valoren-Nr. automatisch ausgefüllt werden.) Steuerlicher Mehraufwand ist weniger mit der Wahl des Börsenplatzes verbunden, sondern hängt eher mit dem Domizil des ETF zusammen. So werden beispielsweise bei US-ETFs ein Teil der Dividende zurückbehalten, welche mittels Ausfüllen des separatem Steuerformular DA-1 teilweise wieder zurückgefordert werden kann. Voraussetzung für solche Rückerstattungen der Quellensteuern sind Doppelbesteuerungsabkommen zwischen der Schweiz und dem entsprechenden ausländischen Staat.

– Vorteile Heimbörse: Handelswährung bei vielen Produkten (insbes. bei Anbieter Vanguard) in CHF möglich, womit die Wechselgebühren entfallen; oft attraktivere Gebühren (z.B. tiefere Courtagen bei Postfinance, keine jährliche Fremdbörsengebühr bei DEGIRO); Nachteil Heimbörse: oft geringeres Handelsvolumen und deshalb grösserer Spread; ETF-Angebot ist zwar mittlerweile umfassend, aber dennoch beschränkt; aktuell keine Gratis-ETFs bei DEGIRO

– Vorteile ausländische Börsen: Vgl. Punkt oben mit “umgekehrten Vorzeichen”;-)

Beste Grüsse

SFB

An dieser Stelle einfach einmal ein Danke, dass ihr euch die Zeit nehmt verständlich und ausführlich zu antworten.

BG, Larissa

Hallo zusammen

Wie sieht es mit den Steuern aus, wenn man in einen ETF mit Domizil in Irland investiert?

Werden die Steuern automatisch beim Kauf abgezogen? (zb bei Swissquote)

Habit ihr einen Artikel dazu? Habe auf die schnelle nichts gefunden. 🙂

Besten Dank & Liebe Grüsse

Guten Tag Lars

Gute Idee mit dem Steuerartikel, der aktuell in unserer Sammlung noch fehlt. Steuerlich sind die in der Schweiz stark verbreiteten ETFs mit Domizil Irland sehr “pflegeleicht”. So sind Verrechnungssteuer und Rückforderungsanträge anderer Art, kein Thema. Unabhängig des Domizils des ETFs gilt in der Schweiz hingegen:

1) Dividenden, unabhängig davon, ob es sich um einen ausschüttenden oder thesaurierenden ETF handelt, sind als Einkommen zu versteuern.

2) Das in ETFs angelegte Vermögen unterliegt der Vermögenssteuer.

3) Realisierte Kapitalgewinne aus ETF-Verkäufen sind steuerfrei.

Beste Grüsse

SFB

Hallo liebes Finanzblog-Team

Vielen Dank für eure hilfreichen Artikel.

Ich habe auch eine Frage…

Was hält ihr von folgenden ETF?

CSIF FTSE EPRA/NAREIT Developed Green Blue

ISIN: IE00BMDX0K95

Er ist ein mittelgrosser ETF und noch jung, da er erst im 2020 aufgelegt wurde.

Was mich verunsichert, an keinem Tag an dem ich geschaut habe, wurde er an der Schweizer Börse SIX gehandelt. Da ich bei Degiro keine Gebühr zahlen muss, wenn ich an der SWX anstelle der Xetra kaufe, bevorzuge ich diesen eigentlich an der SIX in USD zu kaufen anstelle in Euro an der Xetra.

Was ist eure Meinung dazu? Und allgemein zu diesem ETF?

Ich wäre mega dankbar für eine Antwort.

Liebe Grüsse

Hoi Reto

Hierbei handelt es sich um einen Branchen-ETF “Immobilien” mit Nachhaltigkeitsfokus und breit diversifiziert über diverse Regionen der entwickelten Welt und mit einem Gesamtnettovermögen von rund 170 Mio. USD. Die TER beträgt gemäss CS Factsheet 0.25%, was wir fair finden. (Interessanter wäre dann die Tracking Difference, wofür dieser ETF aber noch zu jung ist.) Als Beimischung spricht unseres Erachtens nicht viel gegen diesen ETF. Einzig das von dir erwähnte, offenbar geringe Handelsvolumen kann dazu führen, dass der Spread etwas grösser ist und somit die Transaktionskurse etwas weniger vorteilhaft sind. (Durch die Market Makers kommt aber auf alle Fälle eine Transaktion zustande.)

Wenn du ganz vorsichtig sein möchtest, dann gibst du diesem ETF noch zwei, drei Jahre Zeit, bevor du in ihn investierst. Wenn dich dieser ETF aber grundsätzlich überzeugt und du für dich keine vergleichbaren Alternativen auf dem Markt siehst, dann ist womöglich jetzt der richtige Zeitpunkt für ein Investment – vorzugsweise in Tranchen. Ob SIX oder Xetra ist für uns nicht matchentscheidend – hier gilt es nach deiner individuellen Präferenz abzuwägen: USD vs. EUR, unterschiedliche Handelsvolumen, (moderate) DEGIRO-Gebühren für ausländische Börsenplätze etc.

Beste Grüsse SFB

Hallo

Super hilfreicher Artikel. Danke.

Ich habe eine Frage u d zwar möchte ich den FTSE EPRA/NAREIT Index besparen. Ich habe zwei ETF‘s zur Auswahl, ein irischer (ausschüttend) oder Luxemburg (thesaurierend). Ich möchte via Degiro Custody eigentlich nur thesaurierende ETF‘s besparen, bin mir aber nicht sicher, ob ich steuerliche Nachteile beim ETF mit Domizil Luxemburg habe.

Ich bedanke mich sehr für eine Antwort.

Liebe Grüsse

Hoi Timo

Beide Domizile (IE + LU) stehen im Ruf, steuerlich für ETF-Anleger sehr attraktiv zu sein. Es hängt letztlich von der Region der Aktien ab. USA: Vorteile IE; Europa und Schwellenländer = etwa gleich attraktiv (Quelle: Hinder Asset Management)

Beste Grüsse SFB

Hallo zusammen

Vielen Dank für diesen tollen, ausführlichen Artikel.

Ihr habt bezgl. Diversifikation noch Rohstoffe und Immobilien erwähnt.

Gibt es hierzu einen weiteren Beitrag? Ich bin seit Tagen am Überlegen ob ich je ein ETF auf Immobilien und ROhstoffe in mein Portfolio zur Diversifikation aufnehmen soll…

Danke für eine Antwort und liebe Grüsse

Hoi Eliana

Ja, zum Immobilien-Thema kommt sicher noch ein Artikel. Immobilien-ETFs sind als Beimischung sicher eine prüfenswerte Option. Die Ausschüttungsquote ist oft überdurchschnittlich hoch, die Kursentwicklung eher moderat. In Rohstoffe sind wir nicht investiert und haben dies auch nicht vor.

Beste Grüsse SFB

Hallo zusammen,

ich habe eine kurze Frage hinsichtlich eines ETF, dessen Fondwährung USD ist. Macht das einen Unterschied, ob ich in über einen Sekundärmarkt in USD oder EUR investiere? Bsp. ich möchte 5000 CHF in den Fonds investieren und kann über die Xetra in EUR oder über die London Exchange in USD investieren.

Danke schonmal.

Toller Artikel. Vielen Dank!

Ich habe ein Konto bei Degiro eröffnet und in den einzigen MSCI World investiert der dort gratis gehandelt werden kann. Dieser wird in Euro geführt. Nun möchte ich gerne noch einen Emerging Markets ETF dazu nehmen.

Beim Emerging Marktes ETF werde ich wohl eher einen wählen bei dessen Handel Gebühren anfallen, da mich jener der gratis gehandelt werden kann nicht sonderlich überzeugt (DE000ETFL342).

Was ich mich generell frage ist: Macht es Sinn gleiche ETF’s in verschiedenen Währungen zu haben um sich gegen Kursschwankungen abzusichern? Oder würdet ihr sowieso immer einen ETF wählen, der in CHF gehandelt wird um Wechselgebühren zu sparen?

kann es sein, dass Vanguard nur ausschüttende ETFs anbietet? Bin auf der Suche nach zwei ETF, welche thesaurierend sind.

ja das ist korrekt (vgl. auch Homepage von Vanguard Schweiz).

LG SFB

Super, danke für eure kurze Einführung, genau was ich gesucht habe!

Frage: Ist das Investieren als Schweizer in zwei ETF, die beide in USD gehandelt sind, nicht ziemlich risikoreich?

Fragen eines Noobs:

– gibt es ähnliche Indizes, die auf CHF basieren? Würdet ihr das empfehlen? Weshalb ja, weshalb nicht?

Hoi Simon

Nein, grundsätzlich erachten wir ETFs, welche in USD gehandelt werden bezüglich des Währungsrisikos als nicht sehr risikoreich. Denn die Handelswährung ist diesbezüglich nicht entscheidend. Vgl. hier auch unseren Artikel ETFs: Die Revolution der Geldanlage, Kapitel 7.

Falls du in ETFs investieren möchtest, deren Handelswährung CHF ist, so könnte der Anbieter Vanguard eine prüfenswerte Option sein. ETF-Pionier Vanguard bietet nicht nur praktisch all seine ETF-Produkte in CHF an, sondern ist auch bekannt für seine fairen Gebühren.

Beste Grüsse

SFB