Newsletter

Newsletter

If you want to build up wealth in a long-term, self-determined and successful way, there is hardly any way around it: Investing in ETFs is the smartest way to invest money today. Exchange-traded index funds allow you to invest cost-effectively and transparently in thousands of companies worldwide with a single transaction – without an expensive fund manager. In this 6th lesson of our financial guide, you will find out what is behind the acronym, why ETFs have revolutionized investment and why you too can benefit from them.

< Lesson 5 | Overview | Lesson 7 >

Short & sweet

- An ETF (Exchange Traded Fund) is an exchange-traded index fund that passively replicates an equity index according to fixed rules.

- In contrast to actively managed funds, ETFs do without stock picking and expensive fund managers – and therefore only cost a fraction.

- Investing in ETFs means relying on a simple, cost-effective and scientifically sound investment principle – with minimum effort and maximum diversification.

- Legally, ETFs are special assets: your money is protected in the event of the insolvency of the provider, custodian bank or your broker.

- Numerous studies show that the majority of active funds do not outperform their benchmark index in the long term – the strongest argument in favor of passive investing in ETFs.

Contents

What is an ETF?

ETF stands for Exchange Traded Fund. These three words already contain the essentials.

Index fund means: An ETF replicates a specific stock market index – such as the MSCI World with over 1,000 companies from 23 industrialized countries. The ETF buys the shares contained in the index and holds them in the same proportion. If the index rises by 2%, the ETF also rises by around 2%. If the index falls, the ETF falls. No fund manager decides which shares to buy or sell – the index rules take care of that. This makes ETFs passive and distinguishes them fundamentally from traditional investment funds, where a management team actively tries to beat the market.

Exchange-traded means that you can buy and sell an ETF at any time during trading hours on the stock exchange – just like an individual share. Unlike traditional funds, which calculate a price once a day, with an ETF you can see what it is worth in real time.

And the costs? Because no fund manager has to analyze and select shares, a large proportion of the fees incurred by actively managed funds are eliminated. The annual costs (expressed as TER, Total Expense Ratio) for broadly diversified ETFs are typically between 0.1% and 0.3% of the invested capital – with a downward trend. This is because the intense competition among ETF providers means that fees are literally eroding. What cost 0.5% ten years ago is now available for a fraction of that. By comparison, active funds often charge five to ten times as much – year after year. What is particularly bitter is that the vast majority of these expensive funds do not even manage to beat the market. So you pay more and get less.

A brief history of ETFs

The idea of simply tracking the market rather than beating it is older than many people think. In 1975, John “Jack” Bogle founded the investment company Vanguard and shortly afterwards launched the first index fund for private investors – the “Vanguard 500 Index Fund”. The idea was revolutionary at the time and was ridiculed by Wall Street: a fund that didn’t even try to outperform the market? Bogle was right.

However, it was almost two decades before the idea took its next evolutionary step. On January 22, 1993, State Street Global Advisors launched the first exchange-traded index fund on the market: the “SPDR S&P 500 ETF” (stock ticker: SPY). The “Spider”, as it is colloquially known, tracks the 500 largest listed US companies – and is now the largest ETF in the world with assets under management of around 700 billion US dollars. By way of comparison, there were 6.5 million when it was launched.

Growth has accelerated massively since the 2000s. There are now over 20 trillion US dollars in ETFs worldwide – a figure with 13 zeros. The trend is not hype, but the logical consequence of superior product innovation.

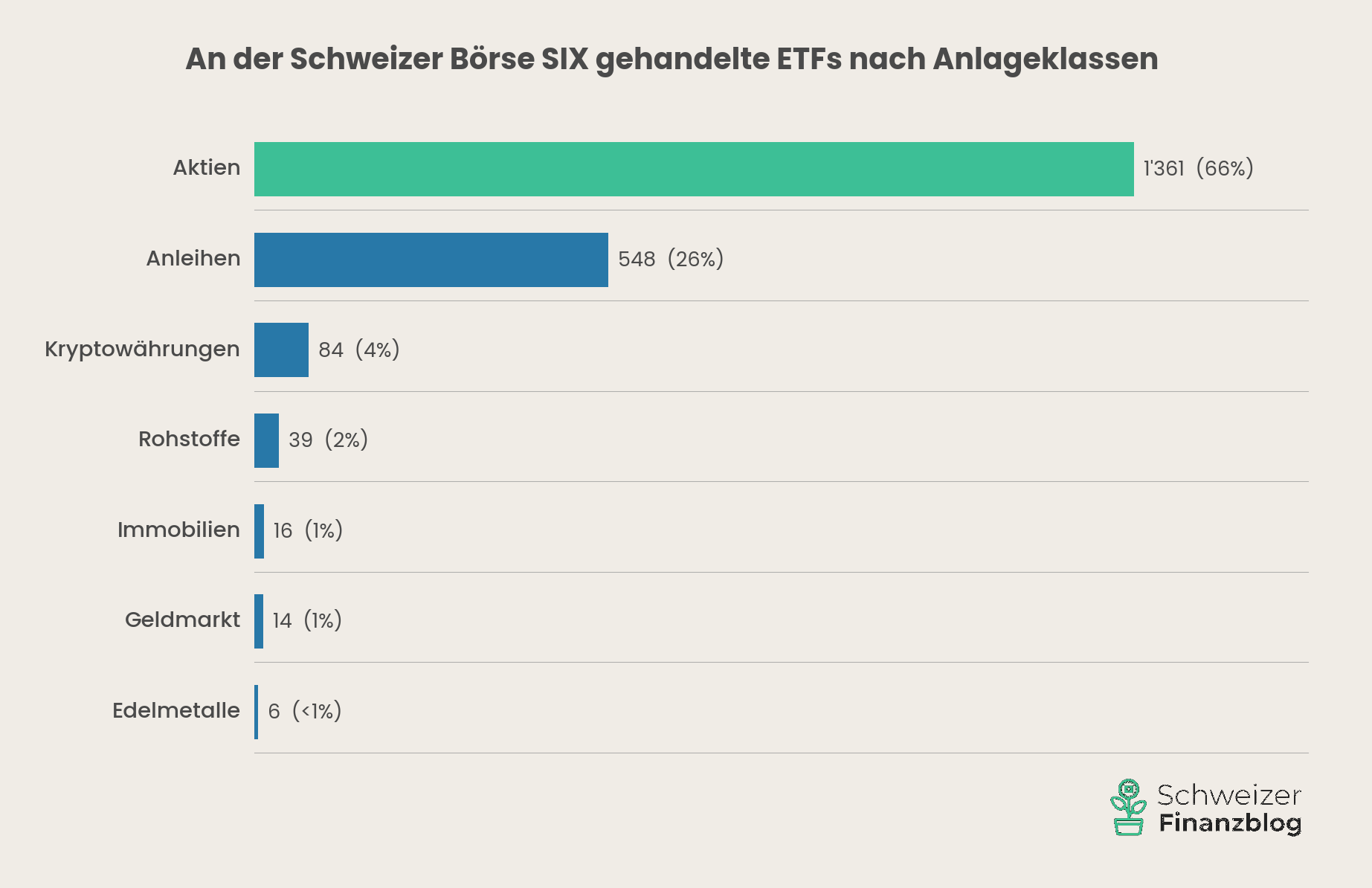

ETFs in Switzerland

The Swiss stock exchange SIX was one of the first in Europe to introduce an ETF segment – in 2000. Since then, the offering has grown rapidly: in 2026, over 2,000 ETFs will be listed on SIX. By comparison, there were still around 1,300 in 2018.

The Swiss market is dominated by the providers UBS and BlackRock (with the ETF label “iShares”). Globally, BlackRock and Vanguard are the undisputed market leaders.

How does an ETF work?

The basic principle is quickly explained: an ETF replicates a specific stock market index as closely as possible. To do this, the ETF provider buys the shares contained in the index and holds them in the same proportion as the index. If the index rises, the ETF rises. If the index falls, the ETF falls. No fund manager makes active decisions – the composition is determined solely by the index rules.

The index as the centerpiece

The underlying index is the actual core of an ETF. Indices such as the MSCI World or the FTSE All-World are calculated by specialized, independent providers – in the case of these two examples by MSCI (Morgan Stanley Capital International) and FTSE (Financial Times Stock Exchange) respectively. Strict rules define which companies are included, how they are weighted and when the composition is reviewed.

For you as an investor, this means that the choice of index determines which countries, regions and sectors you invest in – and therefore a large part of your future returns. We will take a closer look at whether you can find the “right” index and ETF in lesson 7.

What the name of an ETF reveals

Anyone reading an ETF name for the first time can easily feel overwhelmed. Let’s take an example: “Vanguard FTSE All-World UCITS ETF (USD) Accumulating”. It sounds cumbersome, but it follows a clear logic:

Vanguard is the provider – i.e. the fund company that issues the ETF. FTSE All-World refers to the underlying index – in this case a global share index with over 4,000 companies from industrialized and emerging countries. UCITS stands for “Undertakings for Collective Investment in Transferable Securities” and means that the ETF is subject to strict European investor protection guidelines. For you, this means: high transparency, diversification requirements and regulatory supervision. Practically all ETFs tradable in Europe bear this abbreviation. ETF – you know that now. And (USD) Accumulating? USD indicates the fund currency – i.e. the currency in which the fund assets are calculated. “Accumulating” describes how dividends are handled. We will explain what these terms actually mean for you in lesson 7.

You don’t have to memorize these abbreviations. But once you have them figured out, every ETF name loses its horror. In our article Understanding ETF abbreviations: 1C, UCITS, MSCI & Co. simply explained you will find a complete overview of all common abbreviations.

Legal special assets

One point that is particularly reassuring for beginners: ETFs are legally separate assets in Switzerland (regulated by the CISA). This means that your invested money is held separately from the assets of the ETF provider and the custodian bank. If the provider or the bank goes bankrupt, your ETF share remains in your possession.

This also applies to your broker: Your ETF shares are held separately as securities and belong to you, not the broker – regardless of whether you buy through Swissquote, a cantonal bank or a foreign provider. Even if your broker gets into financial difficulties, your securities are protected. You would simply have to transfer them to another broker. With equity ETFs on established indices, a total loss of your investment is therefore practically impossible.

Why ETFs are the best thing that could happen to your money

Enough theory – now it’s getting personal. Before ETFs, the world looked like this for private investors: You could entrust your money to a fund manager who charged high fees and outperformed the market in the majority of cases. Or you could buy individual shares yourself – with the risk that one wrong bet could destroy half your portfolio. There was hardly a third option.

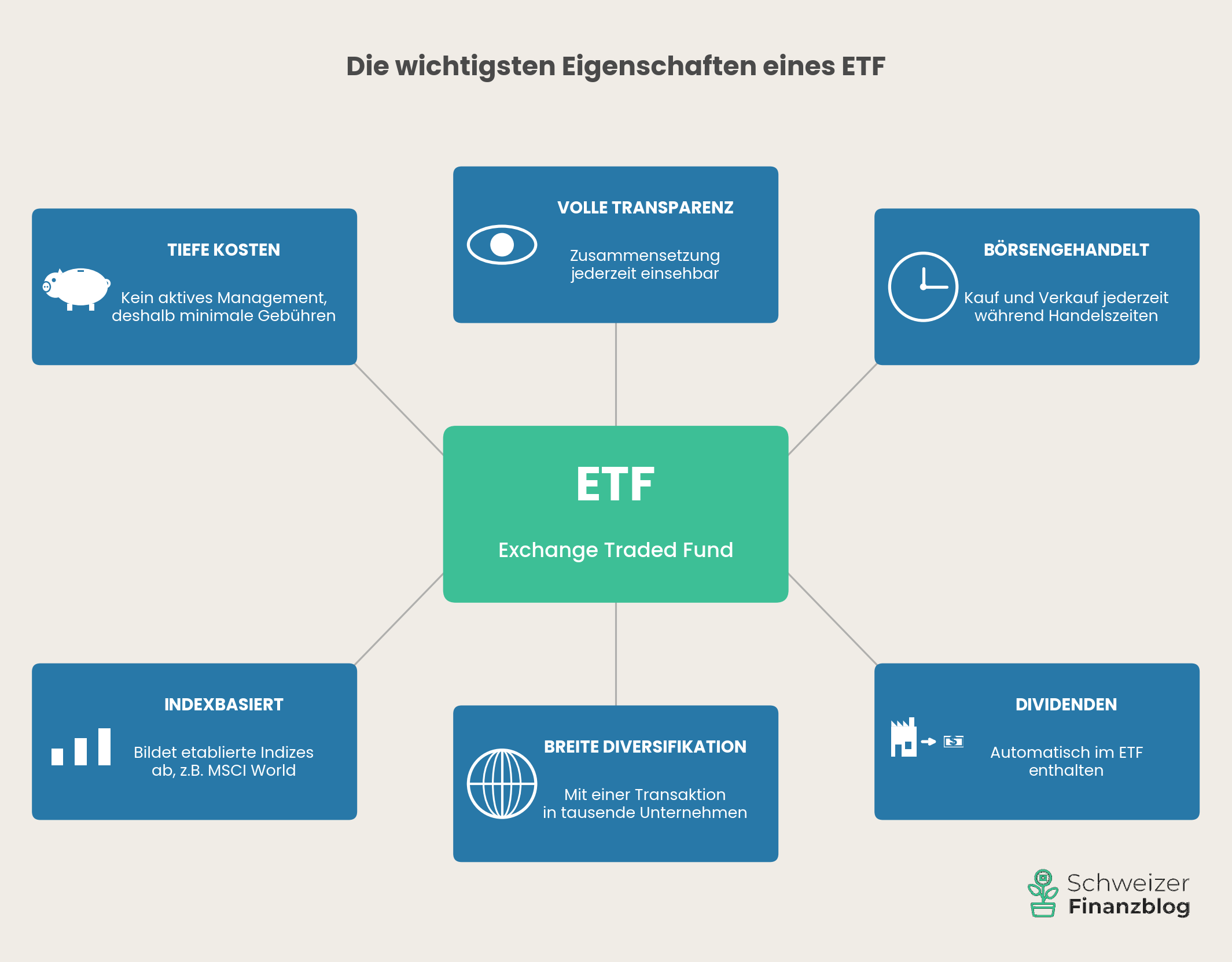

ETFs have fundamentally changed this game. They make something possible that was previously unthinkable: investing in ETFs means participating in thousands of companies worldwide with a single transaction and no minimum amount – at costs that are so low that you hardly notice them.

A simple calculation shows just how powerful this is. If you invest CHF 100,000 in an active fund with 1.5% fees per year, you will lose a six-figure amount in returns over 30 years – the compound interest effect means that the damage far exceeds the pure fees. With an ETF with 0.2%, this amount remains in your assets. We therefore put it bluntly: If you want to invest broadly diversified and for the long term, there is no better instrument than an ETF.

But it’s not just about money. ETFs offer a combination of features that no other investment product combines in this form: full transparency about the securities they contain, daily tradability on the stock exchange, entitlement to dividends and – as described in the previous chapter – legal protection as special assets.

Double your assets every nine years with an ETF

And what does it actually achieve? Anyone who has invested broadly in the global stock market in recent decades has achieved an average return of around 8% per year. That sounds unspectacular – until you factor in the compound interest effect : At 8%, your assets double roughly every nine years (rule of thumb: 72 divided by the interest rate). CHF 100,000 becomes over CHF 1,000,000 in 30 years. Of course, past returns are no guarantee for the future. But the historical evidence over more than a century is impressive.

The accolade from Warren Buffett

A remarkable scene from 2017 shows that ETFs and passive investing are not the idea of outsiders, but a strategy that even the most successful active investors recommend. At Berkshire Hathaway’s annual meeting – in front of 40,000 shareholders – Warren Buffett asked Jack Bogle, who was almost 88 years old at the time, to stand up. Bogle, the founder of Vanguard and inventor of the index fund, was sitting in the audience. Buffett said that no one had done more for American private investors than Bogle, and that his idea would save them hundreds of billions of dollars over time.

“If ever a statue is erected to the person who has done the most for investors, Jack Bogle is the clear choice.“

Warren Buffett

So when the world’s most famous active investor advises his followers to bet on the passive equivalent – that says it all.

Why your bank doesn’t recommend ETFs

Imagine you go to your Raiffeisen advisor and say: “I would like to invest CHF 100,000 in a single global ETF.” The likelihood of him nodding enthusiastically is low. Instead, he’ll probably recommend an in-house strategy fund – “Raiffeisen Futura” or similar – plus perhaps currency hedging and a regular consultation. All this sounds sensible, but will quickly cost you 1.5% or more per year. With CHF 100,000 and a 30-year investment horizon, we’re talking about a difference of several tens of thousands of francs compared to a simple ETF solution.

The same applies to UBS, PostFinance and your cantonal bank. The business model of these institutions is based on fees for advice, administration and in-house products. An ETF that costs 0.2% and does not require an advisor simply does not fit into this model. This does not mean that your bank advisor is maliciously harming you – he recommends what is in his range. But his range is not put together in your interests, but in the interests of the bank.

Stefan experienced it himself during his training as a financial advisor: structured products, options, strategy funds and life insurance policies were dealt with at length – all of them high-margin products. ETFs? A side note. There is a simple reason why we focus on ETFs on this financial blog: we are independent

Supposed hedges are particularly expensive: Currency hedges, capital protection products or “dynamic” strategies that shift into bonds in the event of turbulence. What sounds like security at first glance actually eats up returns over a long investment horizon. With these products, you feel the price twice – as a lower return and as a hefty fee.

The rule of thumb is therefore uncomfortable, but honest:

“The most obvious way – just go to the house bank and have it done – is often the most expensive.“

The honest flip side

As convincing as the advantages are – if you want to provide honest information, you also have to show the other side. We do not see any relevant disadvantages with ETFs compared to active funds or individual shares. But there are risks and peculiarities that you should be aware of.

The market risk

The greatest risk is not borne by you because of the ETF, but because of the market. If the global stock markets fall by 30%, your ETF will fall by 30% with them – because it tracks the market, no more and no less. The decisive difference to individual shares: a total loss is practically impossible with a broadly diversified ETF. And experience shows that global portfolios have always recovered even after sharp falls – as we showed in lesson 1 using historical data.

No voting rights

Anyone who owns individual shares has a say at the Annual General Meeting. This is not the case with an ETF: the voting rights are exercised by the fund company – i.e. by providers such as BlackRock or Vanguard. Be honest: when was the last time you attended a general meeting? For the vast majority of private investors, this is a theoretical disadvantage that is irrelevant in practice.

Deadly boring – and just right

An ETF on the MSCI World will never deliver the return of a Tesla share in its best year. But never the crash of a Credit Suisse. ETFs are the opposite of thrills – and that is not a bug, but a feature. If you want to build up assets over the long term, you don’t need adrenaline, but discipline and patience. The fact that ETFs are “boring” is perhaps their greatest advantage.

Counterparty risk – rather theoretical

One last point, for the sake of completeness: so-called synthetic ETFs – which do not track an index by buying the shares it contains, but by means of a swap – are subject to counterparty risk. The same applies to ETFs that engage in securities lending. In practice, these risks are strictly limited and hedged by regulation. Synthetic ETFs are also in sharp decline. If you want to be on the safe side, simply opt for physically replicating ETFs – which we recommend anyway. You can find out exactly what “physically replicating” means in lesson 7.

– Partner offers –

Still looking for the right financial solution? Our recommendations – with attractive starting bonuses.

– – – – –

Conclusion

ETFs have democratized investment. What used to be reserved for institutional investors with budgets in the millions – broadly diversified, cost-effective and rule-based investment in the global markets – is now open to anyone and everyone. With a single transaction. And it’s getting better and better: fees are falling all the time, the range is constantly growing – investing in ETFs is more attractive today than ever before.

The idea is as simple as it is effective: instead of trusting an expensive fund manager, who doesn’t beat the market in the majority of cases anyway, you simply track the market. You save on fees, avoid unnecessary risks from individual stocks and benefit from the full breadth of the global economy. The fact that even Warren Buffett – probably the most successful stock picker of all time – recommends precisely this approach for private investors speaks for itself.

Of course, ETFs carry market risk – but that is not an argument against ETFs, but against unrealistic return expectations. For those who have understood the basics from the previous lessons – think long-term, diversify broadly, keep costs low – ETFs are the ideal tool for putting this strategy into practice.

The crucial question remains: Which ETF should you buy? We take a closer look in lesson 7: What you should look for when choosing.

You can find an overview of all the lessons here: Learning to invest – in eight lessons.

This might also interest you

Updates

2026-04-17: Article completely revised and updated.

Disclaimer

Disclaimer: Investing involves risks of loss. You must decide for yourself whether you want to bear these risks or not.

Errors excepted: We have written this article “Investing in ETFs…” to the best of our knowledge and belief. Our aim is to provide you as a private investor with the most objective and meaningful information possible on the subject of finance. However, if we have made any mistakes, forgotten important aspects and/or are no longer up to date, we would be grateful if you could let us know.

12 Kommentare

Lieber Stefan, lieber Toni

Vielen, vielen Dank für eure tollen Beiträge! M.E. ist ein Besuch auf euren Blog für alle Privatinvestoren in der CH ein Muss!

Zum Thema Währungsrisiko hätte ich noch eine Frage:

Leider gibt es den IE00BK5BQT80 an der SIX in der thesaurierenden Variante nicht, so dass ich diesen ETF via Swissquote an der Xetra in € gekauft habe. Aufgrund des aktuell starken CHF gegenüber dem € habe ich hier aktuell eine Performanceeinbusse.

Ich überlege mir, sobald sich der Wechselkurs CHF|€ wieder stabilisiert hat (1:1), alle Anteile zu verkaufen und die Summe im ETF IE00B6R52259 an der SIX anzulegen, da dieser ETF auch global diversifiziert ist und die Handelswährung in CHF ist.

Würde ich somit besser fahren resp. das Handelswährungsrisiko komplett reduzieren?

Vielen dank für eure Unterstützung!

Beste Grüsse

Gia

Liebe Gia

Merci fürs Lob! Bitte beachte, dass das Währungsrisiko nicht mit der Handelswährung zusammenhängt, sondern mit der Währung der im Index abgebildeten Unternehmen. Wenn du also in einen ETF investierst, welcher zu einem grossen Teil US-Firmen enthält, dann hängt das Währungsrisiko primär von der Entwicklung vom USD im Verhältnis zu deiner Heimwährung ab, unabhängig davon, welches die Handels- oder Fondswährung ist. Mit der Handelswährung sind lediglich Währungswechselgebühren, welche je nach Broker unterschiedlich hoch ausfallen, verbunden. Wenn du diese vermeiden möchtest, solltest du vorzugsweise in ETFs mit Handelswährung CHF investieren.

Beste Grüsse

SFB

Vielen Dank!

Liebe Grüsse

Gia

Liebe Blogger,

Ich plane, 2/3 meines PK-Vermögens in ETF (Mix mit ESG) anzulegen; würdet ihr sagen, es ist eine gute Idee, auf ausschüttende ETF zu setzen, damit ich meine Rente aufbessern kann?

Gruss aus Basel

Hoi Christoph

Ja, dies dürfte in deiner Situation und wenn du einen längeren Anlagehorizont (ca. 10 Jahre) verfolgst eine gute Idee sein, da dieser Zustupf zu deiner Rente ohne zusätzliche Gebühren verbunden ist und automatisiert, d.h. bequem ohne dein aktives Zutun erfolgt (im Gegensatz zum Verkauf von ETF-Anteilen). Wenn du im grösseren Stil und systematisch Vermögen abbauen möchtest, ohne vorzeitig Pleite zu gehen, könnte dich dieser Artikel über Entnahmepläne interessieren.

Beste Grüsse

SFB

Noch eine Frage: wenn man z.B. 250 CHF montlich per ETF spart, lässt sich überhaupt ein Portfolio Allokation – 60% MSCI World, 30% MSCI Emerging Markets und 10% Immobilien ETF erreichen oder ähnlich?

Ich kenne die Preise für die einzlenen ETFs (noch) nicht, aber wenn jeder ETF 100 CHF kostet, lässt sich diese Allokation monatlich schwer mit den 250 CHF einhalten oder? Oder kann man von jedem ETF kleinere Tranchen kaufen, die weniger als z.B. 100 CHF kosten, um dann so die Allokation monatlich einzuhalten?

Ja klar, das lässt sich gut erreichen. Statt aber 250 CHF mühsam Monat für Monat für drei ETFs zu splitten und drei manuelle Trades zu machen, ist es doch viel einfacher, wenn du die 250 CHF in jeweils nur einen ETF investierst. Nach einigen Monaten wirst du dann deine Zielallokation ungefähr erreichen. Danach investierst du die 250 CHF jeweils in jenen ETF, welcher von der Zielallokation am stärksten abweicht. Du wirst feststellen, dass die prozentualen Abweichungen von der Zielallokation mit steigender Anlagesumme immer kleiner werden.

Super, vielen Dank!

Alles klar, danke. Ich schätze Eure Hilfe. Wenn ich es richtig sehe, dann sind bei Degiro der IShares MSCI World und der IShares MSCI Emerging Markets kostenlos. Dann spielt es keine Rolle wenn ich diese nehme statt den MSCI ACWI allein?

Bei DEGIRO wird auch eine fremdländischen Börsen Gebühr erhoben. Bei dieser spielt es aber keine Rolle wie viele ETFs man kauft und eine andere Gebühr, die von der Anzahl ETFs abhängt gibt es bei DEGIRO nicht oder?

Ist es ein Problem wenn man thresaurierende ETFs (MSCI World, MSCI Emerging Markets) mit Immobilien ETF (ausschütend) mischt? Das hat keine negativen Konsequenzen?

hier unsere Antworten zu deinen drei Fragen:

1) Was die Courtagen betrifft, so spielt es keine Rolle. Denn diese entfallen bei den DEGIRO Gratis-ETFs. Und die Wechselgebühren werden prozentual erhoben (d.h. 0,25% pro investierten Summe), was auch keinen Unterschied macht, ob du einen oder mehrere ETFs in Fremdwährung kaufst.

2) Auch bei der Gebühr für die “Einrichtung von Handelsmodalitäten” ist nicht die Anzahl ETFs entscheidend, sondern die Anzahl fremder Börsenplätze. (Bei Handel über die SIX erhebt DEGIRO für CH-Kunden keine Gebühr.) Wenn also die von dir gewünschten ETFs über den gleichen ausländischen Börsenplatz gehandelt werden, so fällt diese Gebühr nur einmal an.

3) Nein, wir sehen da kein Problem.

Beste Grüsse

SFB

Hallo Team, dürfte ich zwei Fragen stellen?

1) Wenn ich drei ETFs über DEGIRO kaufe für mein Portfolio (MSCI World, MSCI Emerging Markets, und ein Immobilien ETF) zahle ich dann 3 mal die Gebühren bei DEGIRO? Wäre es dann nicht besser ich würde nur in den MSCI ACWI investieren und einen Immobilien ETF um die Gebühren tief zu halten? Vor allem, da ich zu Beginn zw. 100 – 1000 investieren möchte.

2) Gibt es eine Fausregel zur Gewichtung von MSCI World und MSCI Emerging Markets? ZB. 70% World, 30% Emerging Markets?

Hoi Mirko

Ja klar, du kannst immer Fragen stellen, zu all unseren Artikeln, auch zu älteren Exemplaren, wie der vorliegende.

1) Bei den Gratis-ETFs von DEGIRO spielt die Anzahl ETFs bezüglich der Gebühren keine Rolle. Bei allen anderen ETFs kommt eine Pauschalgebühr pro Transaktion zur Anwendung. Das heisst, wir sehen es wie du. Gebührenmässig fährst du in diesen Fällen (d.h. bei nicht Gratis-ETFs) besser, wenn du dich auf einen einzigen ETF konzentrierst. Bei den von dir genannten Beträgen würden wir diese Variante klar vorziehen (d.h. einen globalen ETF basierend auf MSCI ACWI oder FTSE All-World). Vgl. bei Bedarf auch unseren Artikel über die besten ETFs.

2) Nein, eine Faustregel ist uns nicht bekannt. Wenn du eine “neutrale” Gewichtung anstrebst (d.h. schlicht nach Marktkapitalisierung, wie sie im MSCI ACWI oder FTSE All-World abgebildet wird), dann wäre das Verhältnis etwa 9:1. Manche Anleger gewichten die Emerging Markets jedoch bewusst etwas stärker (z.B. 8:2 oder gar 7:3, wie von dir erwähnt), weil sie damit bzw. durch die Faktorprämie “Political Risk” langfristig eine bessere Rendite erhoffen. Vgl. bei Bedarf auch unseren Artikel über Factor-Investing.

Beste Grüsse

SFB