Newsletter

Newsletter

Why does one investment yield an attractive return while another barely beats inflation? The answer lies in the magic triangle of investing – and in a conflict of objectives that no one can escape. In this second lesson of our financial guide, you will find out which three factors are decisive for your wealth accumulation, how they depend on each other and which goals you can pursue at the same time – and which not.

< Lesson 1 | Overview | Lesson 3 >

Short & sweet

- The magic triangle of investment shows that returns, availability and security cannot be maximized at the same time.

- If you prioritize two of these goals, you will inevitably have to cut back on the third – this applies to every asset class.

- Shares offer returns and availability, but little security. The bank account is safe and available, but offers little return. Medium-term notes or fixed-term deposits offer security and slightly higher returns – but the capital is tied up.

- Which combination is the right one depends on your risk profile – there is no universal best answer.

Contents

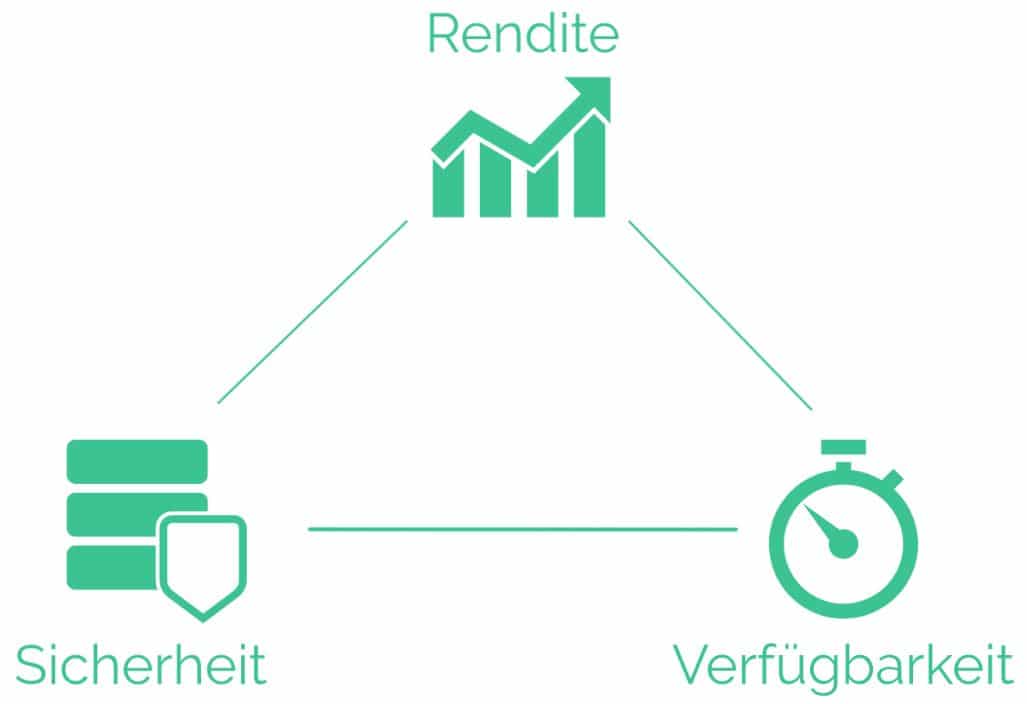

What is the magic triangle of investing?

The magic triangle of investment describes the three competing goals of investment: return, availability and security. The illustration below symbolizes these goals with the corner points of a triangle.

Returns: What are the benefits of the investment?

The yield describes the return on an investment and is the most important starting point for many investors. Typical sources of income are dividends, interest payments or price gains.

As a rule, the higher the targeted return, the greater the risks taken – there is no such thing as a consistently high return without corresponding fluctuations. This is precisely where the conflict of objectives in the magic triangle of investment begins.

For long-term wealth accumulation, it is crucial that income is reinvested wherever possible. The compound interest effect ensures that assets can grow exponentially over time.

The return after costs, taxes and inflation is also important: fees and inflation can significantly reduce the real return. For long-term investments in particular, it is therefore worth paying attention to cost-effective and efficient products – such as broadly diversified ETFs that track an entire asset class such as equities at low cost. Our article Best ETFs Switzerland and globally shows which ones are particularly convincing.

Availability: How liquid is the investment?

Availability – often also referred to as liquidity – describes how quickly an investment can be converted back into cash or bank deposits. The shorter this period is, the more liquid the investment is.

Not only the time, but also the costs of the conversion play a role. Sales fees, spreads or any penalty costs can reduce the amount actually available.

Liquidity depends heavily on the asset class: Exchange-traded securities such as ETFs or shares can be sold every trading day, while real estate or private equity investments are much less flexible.

In the context of the magic triangle, it is clear that high availability often comes at the expense of returns or security. If you want to access your money quickly, you usually have to compromise on one of the other two factors.

Security: How safe is my capital?

Security refers to the preservation of the invested assets. It describes the extent to which an investment is subject to fluctuations and how high the risk of permanent loss is.

Diversification is an important factor in increasing security. Risks can be reduced by spreading across different asset classes, regions and sectors.

At the same time, there is no such thing as absolute security with yield-oriented investments. Even broadly diversified portfolios are subject to short-term fluctuations.

In the magic triangle of investment, security is in conflict with returns and availability. Higher security often goes hand in hand with lower expected returns or limited flexibility.

Only two goals can be achieved at the same time

The magic triangle of investment makes it clear that all three goals – return, availability and security – cannot be maximized at the same time. If you prioritize two of them, you will inevitably have to compromise on the third. This basic rule applies regardless of the asset class or market environment.

There are three specific variants to choose from:

Option 1: High return + high availability = low security

Equities are an example of this combination. They can generate attractive long-term returns and can be sold at any time during stock market trading hours. At the same time, they are sometimes subject to considerable price fluctuations – temporary losses in value of 30% or more are not uncommon in the past.

The security depends heavily on how broadly diversified the investment is. If you invest in individual shares, you risk a total loss in extreme cases – for example if a company goes bankrupt. With a globally diversified equity fund – such as an ETF on the global equity market – a total loss is practically impossible, as thousands of companies would have to become worthless at the same time. Diversification therefore reduces the risk considerably – but it does not eliminate the conflict of objectives in the magic triangle.

This category also includes commodities such as oil, grain and precious metals – whereby gold is considered more of a store of value and inflation hedge than a traditional investment – as well as real estate shares and REITs (exchange-traded real estate funds). Cryptocurrencies, which are among the most volatile asset classes of all, are particularly speculative.

Another option in this area is P2P crowdlending: investors lend money directly to private individuals or companies and receive higher interest rates than on a savings account. The expected returns are attractive, but the credit default risk is real – deposit protection does not apply here. Find out more in our article Crowdlending: P2P Switzerland on the rise.

Variant 2: High availability + high security = low return

The classic bank account combines maximum flexibility with a high level of security: balances of up to CHF 100,000 per person and bank are protected in Switzerland by deposit protection, and the money is available at all times. However, because the bank cannot plan the capital for the longer term, the interest rate is correspondingly low. In the current interest rate environment, the return is barely sufficient to compensate for inflation – the real value of the capital is thus at best maintained or even gradually decreases.

So anyone who opts for maximum security and availability is taking a different risk: a gradual loss of purchasing power and foregoing real asset growth.

Option 3: High security + higher return = low availability

Typical of this combination are forms of investment where the capital is tied up for a fixed term – in return for a higher interest rate than on a traditional bank account, which can at least enable real value retention.

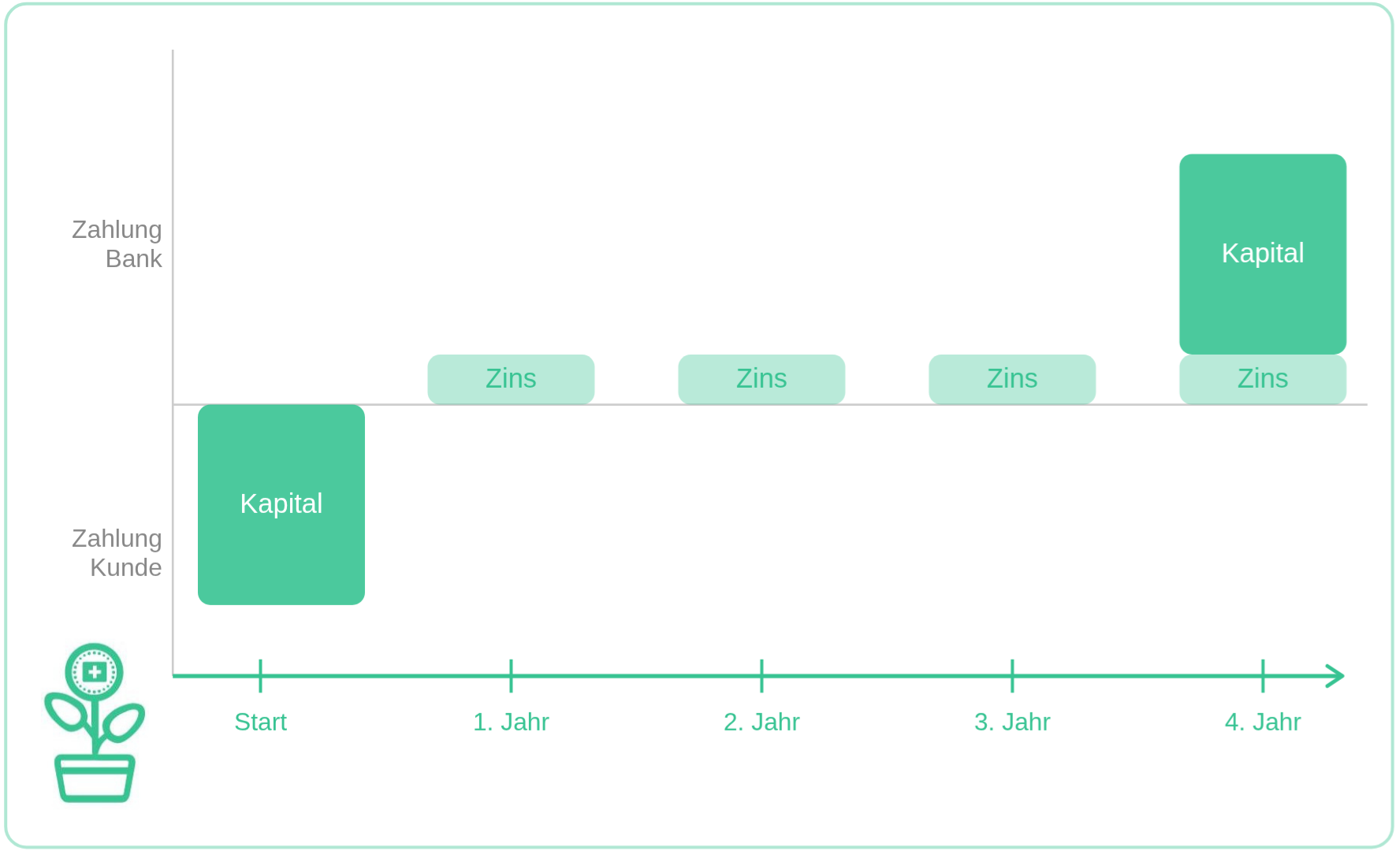

Medium-term notes are fixed-interest securities issued by banks. Investors lend their capital to the bank for a defined term – usually between two and ten years – and receive regular interest payments in return. As the bank can manage the capital more predictably, it pays an interest premium over the savings or private account. Deposit protection also applies up to CHF 100,000 per person and bank.

Fixed-term deposits work in a similar way: Here too, an amount is invested for an agreed term and earns interest at a fixed rate. The main difference to a medium-term note is that a fixed-term deposit is not a security – it is purely a bank deposit that also benefits from deposit protection.

The common price of both forms of investment is limited availability: anyone who wants to access their money early is dependent on goodwill solutions from the bank or must expect losses.

Note: In the current low interest rate environment, interest rates on medium-term notes and fixed-term deposits are also modest. Nevertheless, it is worth comparing providers, as the conditions can vary considerably depending on the bank.

Individual risk profile influences the magic triangle of investment

What your personal magic triangle looks like is not an abstract question – it depends directly on your individual risk profile. This is made up of your risk appetite and your risk capacity.

Your risk appetite: How much risk are you willing to take?

This describes your risk appetite – i.e. your psychological attitude towards fluctuations and possible losses. If you sleep peacefully, even if the portfolio temporarily loses 20 percent of its value, you have a high risk appetite. If, on the other hand, you panic every time prices fall, you should invest more conservatively – regardless of what is mathematically possible. Risk appetite is subjective in nature and is shaped by experience, personality and financial education, among other things.

Your risk tolerance: How much risk can you take?

This describes your risk capacity – i.e. your objective financial situation. It depends on how much capital you have available, what obligations you have and when you expect to need the invested money. If you have high fixed expenses or are dependent on the capital in the foreseeable future, you simply have less scope for risk – regardless of your personal attitude.

The interplay between risk appetite and risk capacity

Both factors together determine which of the three goals in the magic triangle should be your priority.

One example: Anyone planning a major expenditure in the next two to three years – such as buying a home – should focus their assets primarily on high availability and security. Even those who are generally willing to take risks and are relaxed about price fluctuations would be ill-advised to make risky investments in this situation. The ability to take risks – reduced here by the short investment horizon – sets a clear limit that overrides the willingness to take risks.

In short: risk appetite describes what you want – risk capacity describes what you can afford. For a sound investment strategy, both must be in harmony.

– Partner offer –

Still looking for the right financial solution? Our recommendations – with attractive starting bonuses.

——

Conclusion

The dream of a high-yield investment that is available at any time and 100% secure has come to an end. Unfortunately. As in other areas of life, we cannot avoid compromises when it comes to investing.

Which combination is the right one depends on your personal situation: your risk appetite and your risk capacity – which also includes your investment horizon. There is no universal best answer – only the one that suits you.

In lesson 3, we take a closer look: How can smart diversification optimize the risk/return ratio – and what does that mean for your portfolio in concrete terms?

You can find an overview of all the lessons here: Learning to invest – in eight lessons.

This might also interest you

Updates

2026-03-27: Text and illustrations completely revised.

Disclaimer

Disclaimer: Investing involves risks of loss. You must decide for yourself whether you want to bear these risks or not.

Errors excepted: We have written this article on the magic triangle of investing to the best of our knowledge and belief. Our aim is to provide you, as a private investor, with the most objective and meaningful financial information possible. However, if we have made any mistakes, forgotten important aspects and/or are no longer up to date, we would be grateful if you could let us know.

2 Kommentare

Vielen Dank für diesen tollen Artikel. Ich glaube bei der zweiten Variante kann man auch mit Gold handeln? Oder ist das eher nicht sicher?

Hoi Enya,

gemäss Gerd Kommer sind Gold-Anlagen aus folgendem Grund keine sichere Anlage: “Gold ist alles andere als eine solide Anlage: Mehr als 50 Prozent der weltweiten Goldbestände liegen in den Tresoren der Zentralbanken und könnten von diesen jederzeit auf den Markt geworfen werden.”

Zitat: https://www.gerd-kommer-invest.de/wp-content/uploads/getabstract-Kommer-souveraen-investieren-mit-indexfonds-und-etfs.pdf

VG Dirk