Newsletter

Newsletter

VIAC what? The silent giant with over three billion Swiss francs in managed 3a pension assets is still (too) little known to the general public. We want to change this with this exclusive VIAC experience report. Thanks to our long-standing customer relationship with VIAC, you can find out first-hand what makes the Swiss pension pioneer so unique and what investment strategy we pursue for our own 3a pension.

Short & sweet

- VIAC is a Swiss fintech that has been shaking up the local pension market with its low-cost, purely digital investment products since 2017.

- The associated Terzo Pension Foundation of WIR Bank manages steadily growing 3a pension assets of over CHF 3 billion. CHF.

- The uniqueness of “VIAC 3a” is characterized by a colorful mixture of convincing arguments:

- Low fees: Depending on the investment strategy, the total costs vary between 0.00% and 0.44%.

- Attractive investments: Based on an investment universe of 70 index-based securities, there is a broad selection of investment strategies with different equity ratios from 0 to 99%, combined with four investment focuses: “Global”, “Switzerland”, “Sustainable” and – for advanced investors – “Own strategy”.

- High transparency: Information on performance, costs and each individual transaction can be called up at any time.

- Intuitive platform: The user-friendliness of the app on the smartphone as well as the desktop version is state of the art at VIAC.

- 1A support: The VIAC support team provides competent answers within a few minutes.

- Free life insurance: VIAC insures part of its customers’ pension assets against death or disability free of charge.

- VIAC is less suitable in particular for people who value a personal consultation in a nearby branch and/or attach importance to being able to manage both pension provision and independent saving and investing on a single platform.

- Bonus offer: As a new VIAC customer, you benefit from a lifelong fee waiver on the first CHF 1,000 of assets. Depending on which VIAC product you are interested in, simply send us a message with the reference “VIAC 3a Bonus”, “VIAC Vested Benefits Bonus” or “VIAC Invest Bonus” to mail@schweizerfinanzblog.ch.

Contents

- Our VIAC experience with bonus offer: Invest your first CHF 1,000 free of charge!

- About pillar 3a

- History of VIAC

- The VIAC product range

- Our many years of VIAC experience

- How does the “VIAC 3a” offer present itself?

- Swisscanto and Credit Suisse as main partners, UBS and iShares as wild cards

- Spoilt for choice: Which investment strategy is right for me?

- “Own strategy” with the highest degree of freedom

- What fees does VIAC charge?

- What reports & co. are available?

- Our VIAC experience with support

- Our VIAC experience with handling

- How safe is VIAC?

- How does the account opening process work?

- Conclusion from our VIAC experience

- And arguments against VIAC?

- Excursus VIAC Invest

- This might also interest you

- Update

- Disclaimer

Our VIAC experience with bonus offer: Invest your first CHF 1,000 free of charge!

If, after reading this VIAC experience report, you are just as convinced of VIAC as we have been for many years, then you can benefit from our existing customer relationship. How it works: Simply send us a message to mail@schweizerfinanzblog.ch – depending on your requirements – before opening an account, stating “VIAC 3a Bonus”, “VIAC Vested Benefits Bonus” or, for the new product, “VIAC Invest Bonus”.

We will then immediately send you a “Refer a friend” link with your personal bonus code. You then enter this when you open your account, which means that both parties benefit from a lifetime fee waiver on a pension sum of CHF 1,000. This offer is limited.

Transparency notice: Apart from a normal customer relationship as private individuals and the associated “refer-a-friend” program, there are no cooperation or commission models with VIAC.

About pillar 3a

This chapter is dedicated to those who want to remind themselves of our pension system in general and the 3rd pillar in particular. All others can jump directly to our VIAC experience report.

While the first pillar is a state pension scheme (AHV) that guarantees all Swiss citizens a retirement pension, the second pillar is an occupational pension scheme (BVG) in which both employers and employees pay regular contributions into a pension fund.

The 3rd pillar as a private pension provision is intended to supplement the first two pillars. A distinction is made between pillar 3a and 3b (free savings without maximum contributions and without a withdrawal limit). Pillar 3a is characterized by the following features:

- voluntary

- Tax-privileged: amounts paid in are deductible from taxable income

- limited in amount

- Limited withdrawal options: at the earliest five years before and at the latest five years after reaching AHV retirement age. Early withdrawal possible for home ownership, self-employment or emigration, among other things

- Attractive investment solutions thanks to well-functioning competition

Pension pioneer VIAC has made a significant contribution to the functioning competition. Previously, 3a investment solutions were characterized in particular by high costs and low returns.

The Federal Social Insurance Office (FSIO) has published further information on tied pension provision, as pillar 3a is officially known, here.

Who can pay how much into pillar 3a?

The following terms and conditions apply generally, i.e. also to a customer relationship with VIAC or its “VIAC 3a” product.

In principle, anyone over the age of 18 can open a 3a account. However, for a 3a deposit to be possible, income subject to AHV contributions must be earned. Without income, only a transfer of existing 3a assets is possible.

Employees who belong to a pension fund may pay a maximum of CHF 7,056 per year into pillar 3a (as at 2024). Self-employed persons who do not belong to a pension fund and employees who have not joined a pension fund (e.g. persons with very low incomes) can pay in 20% of their annual income, up to a maximum of CHF 35,280 (as at 2024).

History of VIAC

The idea of VIAC was born in 2015 with the vision of a pillar 3a solution that you can recommend to your best friends with a clear conscience. The founders were convinced that the solution, optimized down to the smallest detail, would show our generation a way to arm itself against the looming problems of old-age provision.

” The idea arose from our own need for a simple, understandable and, above all, efficient pension solution. Private pension provision will be indispensable in the future and must be accessible to the masses without any hurdles. “

Daniel Peter, initiator of VIAC

The following milestones shaped the still young history of VIAC:

- 2015 The idea of an attractive pension solution for all

- 2017 Launch of the first digital 3a pension app

- 2020 Launch of vested benefits solution

- 2021 Launch of VIAC Life to cover the risks of disability and/or death.

- 2022 Launch of VIAC mortgage

- 2023 Expansion of the investment universe to include the “bonds” asset class and – in addition to the provider Credit Suisse – index investments from Swisscanto

- 2024 Expansion of the investment universe to include a Bitcoin ETF

- 2024 Launch of VIAC Invest for private savings.

In short: VIAC has revolutionized the previously sluggish and overpriced pension solutions in Switzerland in terms of pricing, simplicity and transparency. It has done so without the big advertising bluster of the financially strong VIAC imitators, but very successfully: the 3a pension assets managed by the Terzo Investment Foundation of WIR Bank now amount to over CHF 3 billion. CHF.

The VIAC product range

Since VIAC was founded, its product range has been constantly expanded. It is currently presented as follows:

- Pillar 3a: Main product (“VIAC 3a”), which we will present in detail later.

- Vested benefits: 2nd pillar pension solution with a similar price and investment model to “VIAC 3a”.

- Private savings: VIAC’s latest product is called “VIAC Invest”. This is a free investment in a portfolio of shares, bonds and/or cash put together according to your risk profile and preferences. We will go into this in more detail at the end of this article.

- Life insurance: With “Life Basic”, free cover of CHF 2,500 in the event of death or disability for every CHF 10,000 of invested assets for VIAC pension customers. Optional “Life Plus” as fee-based, extended risk cover.

- Mortgage: Exclusively for VIAC pension customers; no negotiating poker, but uniform conditions for all (e.g. Saron margin of 0.65%); up to 100% financing possible in conjunction with VIAC pension assets.

VIAC has been offering an investment platform for free saving and investing like other robo-advisors(3 Swiss providers in comparison) or à la Swissquote (our Swissquote experience) since the beginning of December with “VIAC Invest”. We present this new product at the end of this article.

Below we focus on “VIAC 3a”, which is VIAC’s most popular product and is generally available to all adults with an income subject to AHV contributions.

– Partner offer –

– – – – –

Our many years of VIAC experience

We, Toni and Stefan, have been loyal VIAC customers from the very beginning. We both have several 3a accounts, which allows us to make staggered withdrawals at a lower tax rate later on. Year after year, we pay the highest possible amount into one of our 3a accounts with the highest risk profile. Every week, or every Tuesday on the so-called trading day, the newly added cash is invested in the securities on which the selected investment strategy is based.

As you can see, we have a high “skin-in-the-game” factor, which means that nothing stands in the way of a credible first-hand VIAC experience report.

How does the “VIAC 3a” offer present itself?

VIAC offers a comparatively wide range of 3a investment solutions, which means that VIAC should be suitable for most people. The only thing VIAC does not offer is active investment, which we reject due to the high costs without any expected additional return. The scientifically based VIAC investment universe consists exclusively of passive index funds and ETFs. The great diversity of VIAC is reflected in the following facts:

- 4 investment focuses: “Global”, “Sustainable”, “Switzerland” and – for advanced investors – “Own strategy”

- 6 risk levels: from interest-bearing accounts to 99% equity exposure

- 5 asset classes: Cash, equities, bonds, real estate, commodities and alternative investments

- 70 investment products (passive index funds and ETFs)

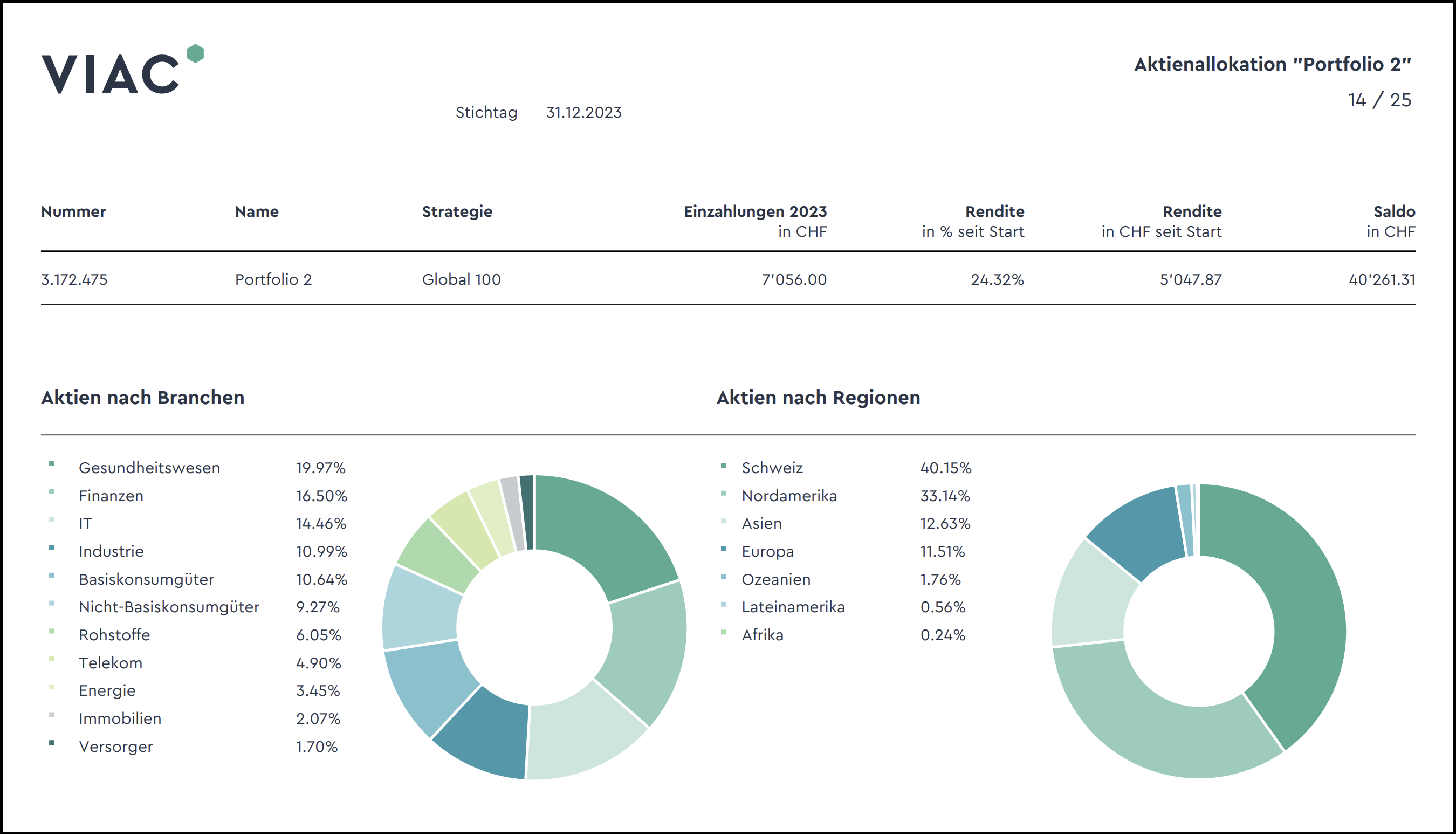

Award-winning VIAC investment strategies

VIAC investment strategies are regularly voted the test winner by the Handelszeitung. In this annual comparison, 3a funds from numerous providers are first grouped according to risk (equity component) and then evaluated in terms of costs and performance over three and five years.

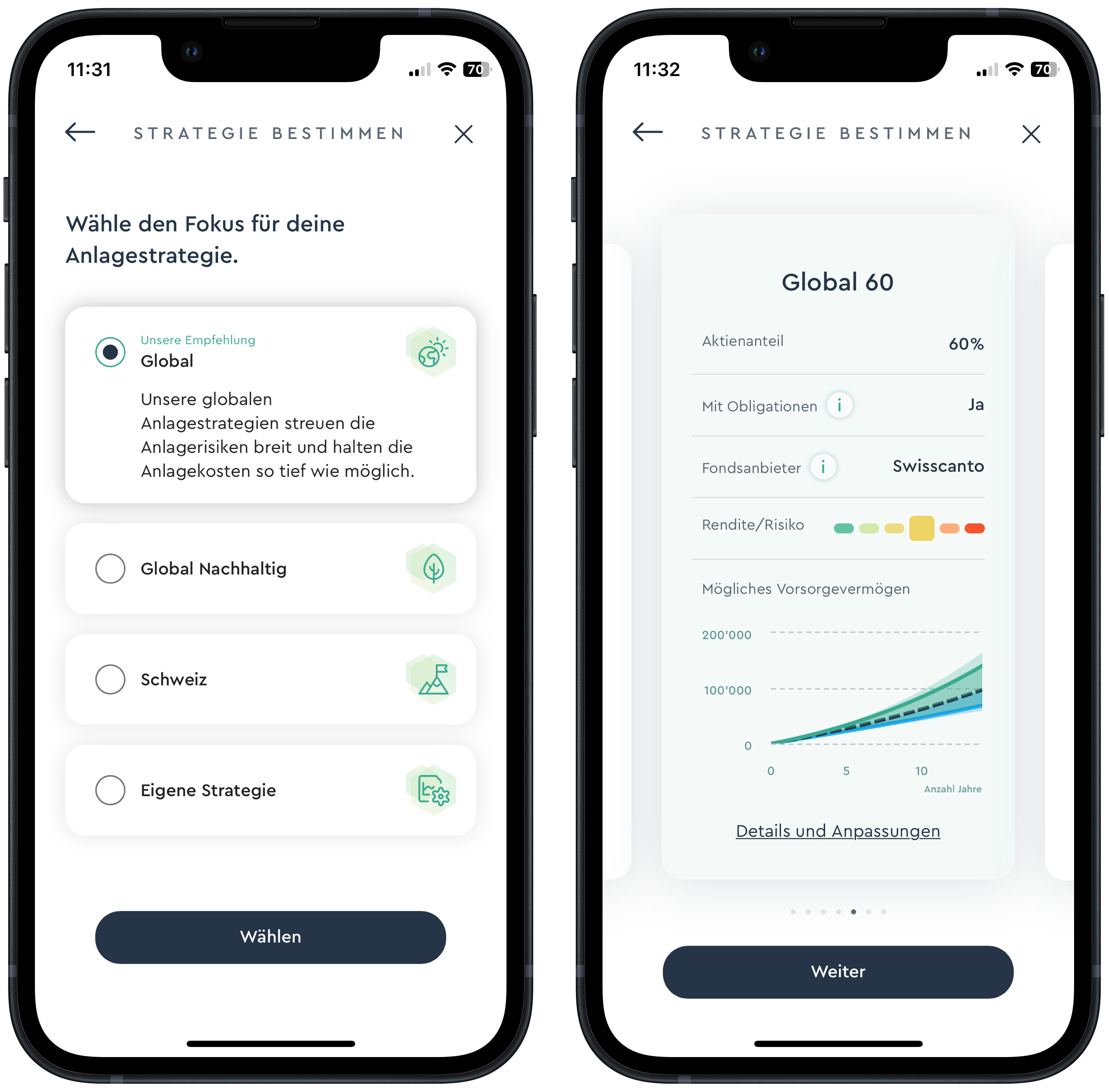

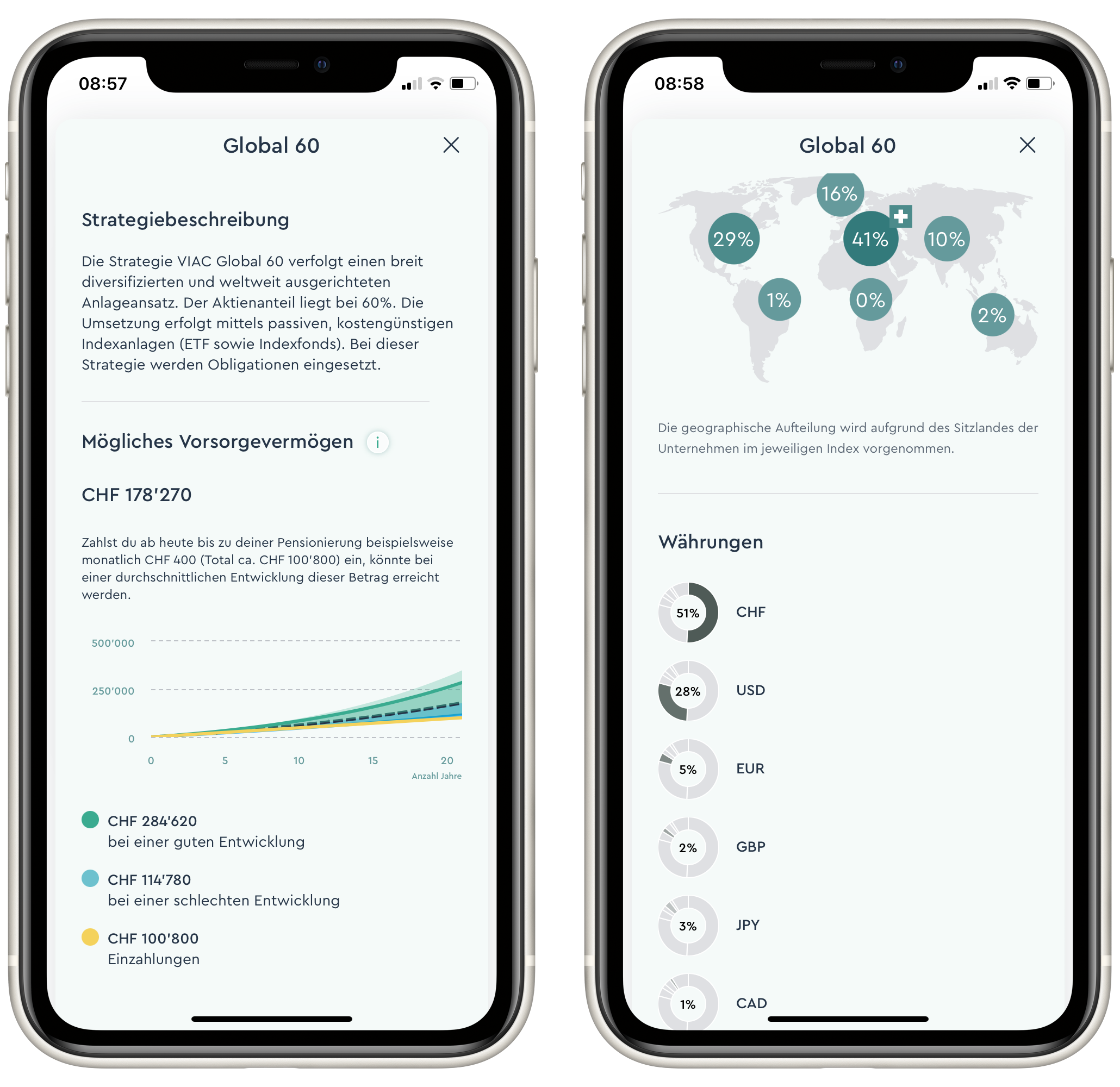

In the example above, we have chosen the “Global 60” investment strategy, which is a fairly balanced standard strategy in terms of risks and expected returns. The total costs are 0.40% per year. With this strategy, which you can change yourself at any time if necessary, you are invested in the following five asset classes with different weightings:

- 60% equities: 20% Switzerland, 34% industrialized countries, 6% emerging markets

- 25% Bonds: Corporate bonds Switzerland

- 10% real estate: 5% Switzerland, 5% world

- 4% Commodities: Gold

- 1% Liquidity: Interest-bearing account

There are two sub-variants to choose from for each standard strategy:

- With or without bonds: If you decide against bonds, the bond portion, in our example 25%, falls into liquidity. This makes the investment strategy somewhat less risky and less susceptible to fluctuations. The liquidity portion earns interest and is free of charge.

- Fund providers Swisscanto or Credit Suisse

Swisscanto only joined as a product provider in 2023 – probably due to Credit Suisse ‘s difficulties at the time and the associated client pressure. Both VIAC partners offer exclusively low-cost index funds that are almost identical or differ only in certain respects.

In addition, VIAC offers ETFs established on the market from the two international heavyweights UBS and iShares (Blackrock). These more expensive, often specialized products (e.g. Clean Energy, Bitcoin) are not available for the VIAC standard strategies, but can only be selected for the “Own Strategy”.

The publicly viewable securities list (scroll all the way down) represents the entire VIAC investment universe, including all index funds and ETFs of the aforementioned VIAC partners.

Spoilt for choice: Which investment strategy is right for me?

Tip: If you are confused by this variety of products and strategies, simply select the standard strategy suggested by VIAC. This is based on your profile and the information you provided when you opened your account.

You can also use the following rule of thumb: The longer your investment horizon and the greater your risk tolerance, the higher the proportion of equities you can choose.

Due to our still long investment horizon of more than ten years, both Toni and Stefan pursue their own strategies at the highest risk level. In contrast to the VIAC standard strategy “Global 100”, which also belongs to the highest risk level and which Stefan also pursues, the proportion of Swiss equities in our individually compiled portfolios is lower. In this way, we want to counteract the “home bias”. You can find out more about home bias and other psychological pitfalls in our article Behavioral Finance: How to avoid the 13 biggest investment mistakes.

Important: You can change your strategy at any time with just a few clicks. The new strategy comes into effect on the following Tuesday on the so-called trading day. VIAC takes care of the associated securities transactions. They are displayed transparently on the platform.

Regardless of which strategy(ies) you choose, with VIAC you can have up to five different 3a accounts, which allows you to make staggered withdrawals at a lower tax rate or to “break” the applicable tax progression.

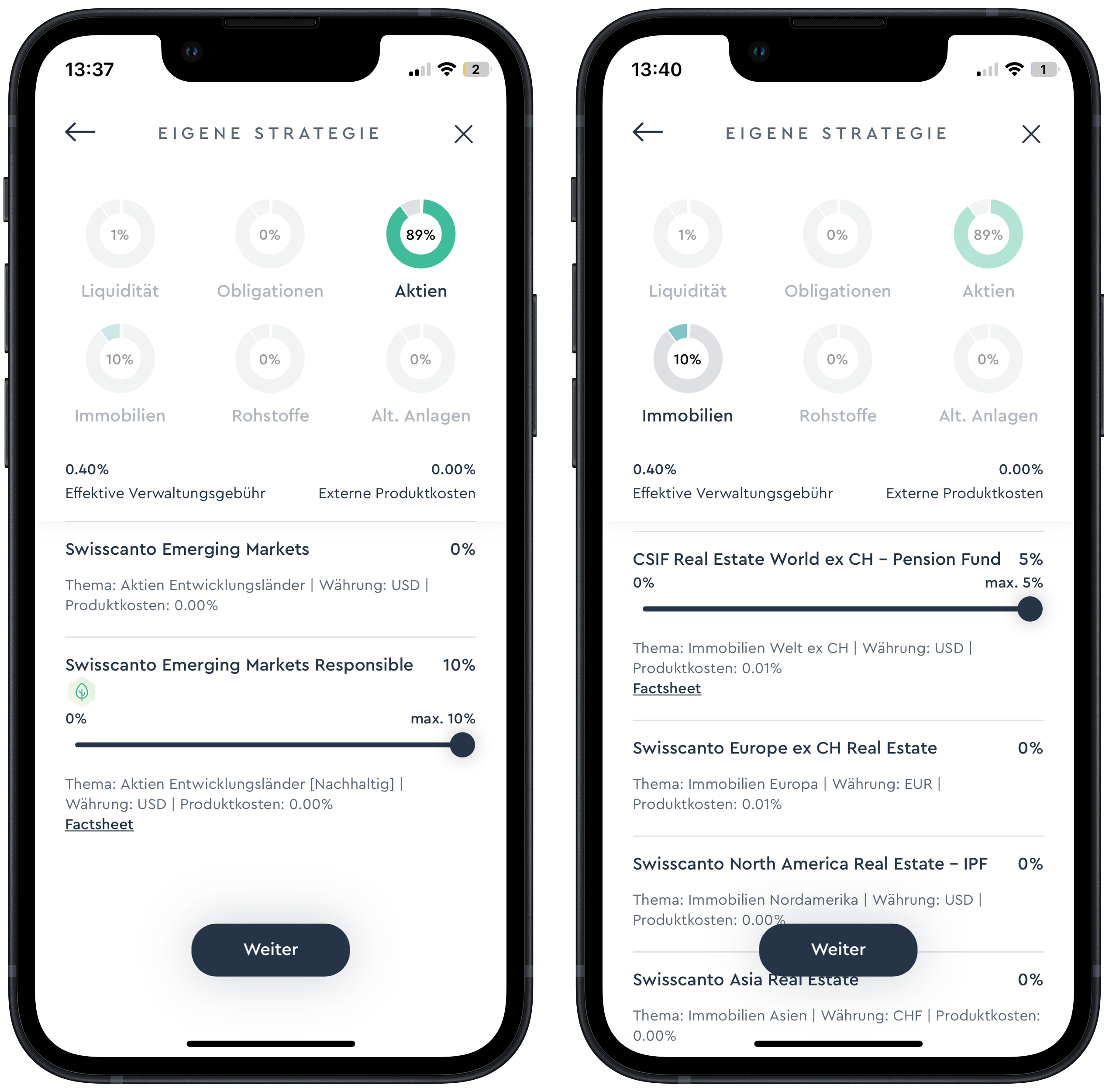

“Own strategy” with the highest degree of freedom

The “Own strategy” makes sense for you if you want to consider additional asset classes (e.g. alternative investments), diversify more broadly within an asset class (e.g. with small caps equities), prefer a different regional weighting (e.g. less Swiss share) and/or want to hedge the portfolio at least partially against currency risks.

However, “anything goes” is not possible, even with its own strategy. This is because VIAC sets a limit for each of the 70 or so securities on offer. For example, it is not possible to invest large amounts in particularly risky investments such as emerging market equities or the newly added Bitcoin ETF from iShares. VIAC and the state regulator in particular want to protect you from overly wild speculation trips.

What fees does VIAC charge?

The total costs, consisting of management fees and product costs, range from 0.00% to a maximum of 0.44% per year, depending on the strategy and investment focus. This includes

- Deposit fee

- Product fee

- Foundation fee

- Transaction fees

- Administrative fee

- Basic cover in the event of disability or death

The two low-risk strategies “3a Account” and “Account Plus” (cash with 5% equity component) are free of charge for all investment focuses. Fair: Unlike with other providers, the cash component is always free of charge with VIAC, regardless of the strategy selected.

Furthermore, you do not pay a basic fee, retrocessions, performance fee, balancing fees or fees for deposits and withdrawals.

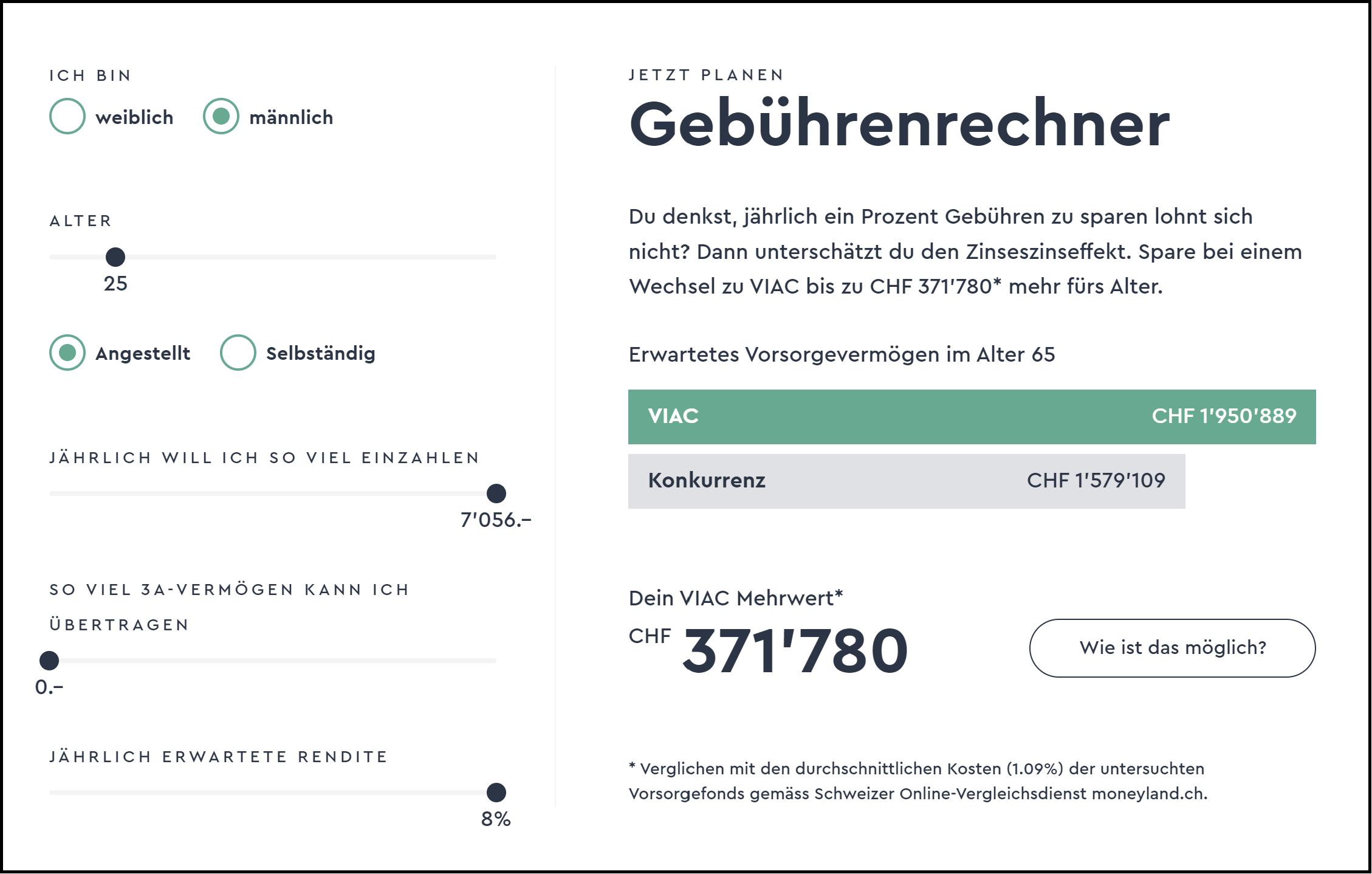

With a fee range of 0.00% to 0.44%, VIAC is undoubtedly one of the cheapest providers on the market. Traditional pension providers with an active investment approach in particular often cost several times more than VIAC.

The total costs at UBS and Swiss Life for their pension funds “UBS Vitainvest – World 100% Sustainable” and “Swiss Life BVG-Mix 75” are a horrendous 1.62% and 1.64% per year respectively (as at April 2024).

Even if the lower average costs on the market of 1.09% compared to these extreme examples are taken into account, the compound interest effect results in a huge increase in pension assets in the long term, as the illustration below clearly shows.

If you are faced with excessive fees, you should not only consider changing provider (for future deposits), but also transferring your existing 3a assets. You can start this process easily via the VIAC app and it only takes a few steps (see explanations in the illustration below).

What reports & co. are available?

VIAC is not stingy with information. On the contrary: VIAC is characterized by a high level of transparency and informative reporting:

In addition to the annual tax statement, VIAC delivers a comprehensive semester report including a market review to your digital mailbox.

In addition, you can keep up to date with your 3a pension solution at all times, down to the level of individual transactions:

- Deposits

- Purchases and sales of securities

- Interest payments

- Dividends received

- Charges

Our VIAC experience with support

Let’s keep it short: VIAC’s support is simply phenomenal and far superior to all other financial providers we have tested so far!

And we know what we’re talking about: Over the years, we’ve come across numerous tricky questions that we’ve asked the VIAC support team via chat. Regardless of whether we were looked after by Carl, Christian, Darius, Emir, Jonas, Lionel, Marco or Simon: There was never anything to complain about. Based on our many years of VIAC experience, we would like to summarize the following two positive points about the support:

- High level of expertise: The VIAC support team masters even complex and/or in-depth requests with flying colors.

- Extremely fast response time: inquiries are usually dealt with within a few minutes.

What may come as a surprise at first is that the digital-savvy VIAC does not use bots for support, but only flesh-and-blood consultants (we have never had contact with female consultants before). That’s a good thing, because let’s be realistic: these support bots are unfortunately usually only good for trivial standard queries or are all too often simply overwhelmed.

Our VIAC experience with handling

VIAC is available as an app on your smartphone, as well as the classic way via the Internet on your desktop. According to our VIAC experience, both views offer you the same useful functions, such as

- Asset overview in total or at account level, broken down into asset classes, regions and currencies

- Information about the selected strategy/strategies and the option to adjust them at any time (regular rebalancing and rebalancing associated with strategy adjustment take place weekly or on Tuesdays on the so-called Trading Day).

- Securities overview per account with detailed product information on the individual index funds and ETFs and their weighting in your own portfolio

- Current transactions such as purchases and sales, incoming interest (for cash) and dividends (for distributing ETFs) as well as fee charges (the annual fees are also shown separately, broken down into management fees and product costs)

- Chat function with direct exchange with the VIAC support team.

In 2023, VIAC launched a comprehensive redesign, which once again significantly improved the appearance and user-friendliness (“look & feel”).

How safe is VIAC?

“Insolvency of the custodian bank” risk

All money that is not invested is held by VIAC’s partner bank “WIR”. Your Terzo pension foundation already manages over CHF 3 billion in 3a pension assets. CHF in 3a pension assets. So if WIR Bank gets into financial difficulties, it is the responsibility of the pension foundation to take the necessary measures to protect the pension assets (this may result in a change of custodian bank, for example).

Important: With the bankruptcy privilege, your account assets up to CHF 100,000 are given preferential treatment in the event of insolvency of the bank holding the account. Privileged assets end up in bankruptcy class 2. As additional security, the custodian bank must hold domestic claims or other assets located in Switzerland (usually mortgages) amounting to 125% of its privileged deposits.

The securities, i.e. in the case of VIAC these are index funds and ETFs, are considered special assets, are held separately and are not included in the bankruptcy estate in the event of the custodian bank’s insolvency. You can find more information on this under Esisuisse.

The VIAC login fulfills the same security standard as the e-banking of various Swiss banks. Access to the VIAC account is protected with your personal password. As soon as you want to make significant changes, you will also be sent a code by SMS for maximum security, which you must enter for confirmation. Your account is therefore well protected against unauthorized access by so-called two-factor authentication.

Risk “Realized price losses”

This risk is not related to VIAC or its custodian bank, but to your portfolio composition (“asset allocation”) and your investment horizon. The higher your risky asset allocation (e.g. in the form of shares) and the shorter your investment horizon, the greater the probability of this risk occurring.

The worst-case scenario would therefore be if you still had a high proportion of equities shortly before withdrawing your pension assets and there was a severe stock market crash at the same time. For risk reasons, we therefore consider it absolutely essential that you gradually reduce the high-risk shares several years before withdrawal or switch to lower-risk investments such as cash and/or bonds.

With VIAC you are very flexible in this respect, i.e. every week on the so-called Trading Day you can pursue a new, for example lower-risk strategy with just a few clicks.

How does the account opening process work?

Before opening an account: If you would like to benefit from a fee discount as a new VIAC client, simply accept our invitation and VIAC will manage your first CHF 1,000 free of charge for life. You will receive the corresponding invitation with your personal bonus code when you send us a message with the note “VIAC 3a Bonus”, “VIAC Vested Benefits Bonus” or “VIAC Invest Bonus” to mail@schweizerfinanzblog.ch.

You can then access a really attractive pension solution in just a few minutes in purely digital form: simply download the app or start the opening process (“Register”) at www.viac.ch, have your ID or passport ready and – if you wish – enter our bonus code at the end of the registration process.

Please do not be alarmed: As part of the onboarding process, your investment type is determined using six simple questions. Based on this, a VIAC standard strategy (account, 20, 40, 60, 80, 100) will be suggested to you. If you do not agree with the investment strategy suggested by VIAC, you can of course override it at any time.

Conclusion from our VIAC experience

The pension market is lucrative and highly competitive with numerous providers. How should VIAC differentiate itself? We think that VIAC doesn’t just have one single aspect that stands out positively, but rather its overall package. According to our VIAC experience, this overall package consists of a bundle of advantages. We have summarized the five most important arguments for a “VIAC 3a” pension solution below:

Argument 1: Low costs

We consider VIAC’s pricing model to be very fair: you pay no fees at all for cash in your portfolio. On the contrary: you receive interest of 1.15% (as of April 2024). Fees are only charged for the invested part of your portfolio (equities, bonds, real estate, etc., but not cash held in your account), with a maximum cost cap of 0.44%. This means that VIAC is on average around 65% cheaper than comparable offers. In addition, thanks to the free Life Basic, you receive up to 25% in addition to your saved 3a assets in the event of disability or death.

Argument 2: Attractive investment products

The VIAC investment universe consisting of passive index investments is extremely diverse. No fewer than 70 products from different asset classes such as equities, bonds, real estate, commodities and, most recently, bitcoins are available to you.

Argument 3: High transparency

You can get a picture of the costs and performance of your pension solution at any time, both consolidated and in relation to the individual investment. You also have access to your accounts at all times and can adjust your investment strategies if your needs change.

Argument 4: Intuitive platform

Following the last comprehensive release in 2023, we consider the VIAC app to be extremely user-friendly and informative. All transactions are easy to carry out via the app. If you don’t want to make strategy changes etc. via your smartphone, you can use the equally impressive desktop version of VIAC as an alternative.

Argument 5: 1A customer support

The rule of thumb that the cheaper the prices, the worse the service definitely does not apply to VIAC. On the contrary: VIAC’s customer support is really top-notch. And we know what we’re talking about. Because during our long-standing customer relationship with VIAC, we have had many tricky queries that were all resolved within a few minutes.

And arguments against VIAC?

VIAC came up with a unique offering back in 2017 that really shook up the then sluggish and overpriced pension market.

According to our VIAC experience, their pension platform has continuously improved over the years. That’s why we are actually completely satisfied with VIAC at the moment and have to look for the fly in the ointment or put ourselves in other people’s shoes to find the following supposedly critical points:

- No branch network: Old-school customers who value a personal conversation in a nearby branch are unlikely to be happy with the digitally oriented VIAC.

- Too many choices: VIAC offers dozens of standard strategies, spread across the three investment focuses “Global”, “Sustainable” or “Switzerland”. The majority of these strategies can then also be specified in terms of the asset class “Bonds” (with or without) and the securities provider (Swisscanto or Credit Suisse). Many (like us) appreciate these options, while others feel overwhelmed by them. The latter may therefore be better served by simply following VIAC’s strategy proposal, based on the questions answered when opening the account, or by looking for an alternative provider with fewer investment options.

If there are any additional pros and cons for you and/or you appreciate the special advantages of another 3a provider, please let us know in the comments below.

Excursus VIAC Invest

It is obvious: in the highly competitive market of free, private saving and investing, it will be very challenging for any new player to succeed. In other words, nobody has been waiting for the 17th robo-advisor. We are therefore not really surprised (also because it suits VIAC) that VIAC wants to and can score points with attractive pricing:

- Management fee of 0.25%, only on the invested capital (0.00% until the end of 2025)

- Product costs of max. 0.25%only on the invested capital

- Lifetime fee allowance of 2,000 for the first 25,000 customers

- Sign-up bonus of up to CHF 100 for the first 25,000 customers (via a virtual wheel of fortune when signing up; Stefan “spun” a bonus of just CHF 20)

- Lifetime fee allowance of up to CHF 7,500 via the VIAC Lifetime Reward Program “Refer-a-Friend” (simply send us a message with the reference “VIAC Invest Bonus” to mail@schweizerfinanzblog.ch and we will arrange the first CHF 1,000 for you).

The selectable investment strategies with different equity proportions and four investment focuses “Global”, “Switzerland”, “Sustainable” and “Own strategy” are as varied as with “VIAC 3a”.

By contrast, the investment universe, which is also passively managed, consists of significantly fewer investment funds (see “VIAC Invest”title list), all of which were newly launched and therefore do not yet have a track record. For example, there are no funds with small caps or commodities (except gold).

As VIAC Support informed us on request, this smaller investment offering, which differs from the other VIAC products, is related to the high regulatory requirements of Finma (e.g. minimum volume to be achieved after 12 months per newly launched fund).

You can find out more about the new “VIAC Invest” product, which allows you to invest fully automatically in your desired portfolio from as little as CHF 1 using a savings plan, on the VIAC website.

This might also interest you

Update

2024-12-09 Investment universe of “VIAC Invest” explained and various illustrations updated.

2024-12-07 New product “VIAC Invest” presented.

Disclaimer

Disclaimer: Investing involves risks of loss. You must decide for yourself whether you want to bear these risks or not.

Errors excepted: We have written this article about our VIAC experience to the best of our knowledge and belief. Our aim is to provide you as a private investor with the most objective and meaningful financial information possible. However, should we have made any errors, forgotten important aspects and/or no longer have up-to-date information, we would be grateful if you could let us know.

7 Kommentare

Hallo,

Ihr schreibt Ihr verfolgt mit VIAC eine eigene Anlagestrategie um den Home-Bias zu verringern. Wie sieht Eure Strategie aus?

Liebe Grüsse

Hoi David

Hier unsere individuellen Strategien, Toni: 99% Aktienanteil verteilt auf: 66% Entwickelte Welt (ex CH), 20% Emerging Markets, 3% CH, 10% Small Caps Entwickelte Welt (ex CH); Stefan: 84% Aktienanteil verteilt auf: 24% CH, 10% Europa (ex CH), 12% USA, 3% Canada, 5% Pacific (ex Japan), 5% Japan, 10% Emerging Markets; 15% Small Caps Entwickelte Welt (ex CH); zusätzlich 10% Immobilien und 5% Bitcoin.

Beide verfügen über mehrere Konten bei VIAC, wobei Stefan neben zwei individuellen auch ein Konto mit Standardstrategie “Global 100” führt.

Beste Grüsse

SFB

Ich setze bei meiner Säule 3a und Vermögensanlage auf VIAC – eine Schweizer App mit top Rendite, tiefer Kostenstruktur und voller Flexibilität.

Besonders spannend: Du kannst dein Portfolio frei gestalten – sogar mit Bitcoin-Anteil. 🪙

Mein aktuelles Portfolio:

• 81 % Swisscanto World ex CH – IPF

• 9 % Swisscanto Emerging Markets

• 4 % Swisscanto World ex CH Small Cap Responsible – IPF

• 5 % iShares Bitcoin Trust

• 1 % Cash

Weil es hier um Erfahrungen mit VIAC 3a geht, gebe auch ich mal meinen Senf dazu.

Am 08. Juli 2019 bin ich mit dem damals vollen Betrag von CHF 7’056.00 eingestiegen. Ab da habe ich jedes Jahr Anfang Januar den maximal möglichen Betrag einbezahlt. Bis Ende 2024 ist so ein total einbezahlter Betrag von CHF 41’530.00 zusammen gekommen.

Per 31.12.2024 steht der Kontosaldo auf CHF 50’891.62, was eine Gesamtperformance in CHF von 9’361.62 ausmacht.

Als Strategie kamen anhand der beantworteten Fragen Global 80 heraus, jedoch ohne Obligationen (wobei ich nicht mehr nachvollziehen kann, warum ich damals Obligationen ausgeschlossen habe). Mein Anlagehorizont ist übrigens auch kürzer, als die der Blogersteller.

Jeder kann für sich selbst ausrechnen, ob das eine ansprechende Performance ist. Ich jedenfalls bin damit zufrieden.

Und ja, einfacher und kostengünstiger kann das Anlegen von 3a Vermögen kaum sein. Ich kann VIAC also guten Gewissens empfehlen.

Hallo zusammen

Vielen Dank für den Bericht.

Ich habe meine 3 Säule momentan bei meiner Hausbank Raiffeisen aber die Gebühren sind einfach zu hoch. Desshalb bin ich auf der Suche nach einer Variante. VIAC scheint mir genau das Richtige zu sein.

Aus Steuerlichen Gründen macht es Sinn, mehrere 3a Konten zu eröffnen und nicht über ca. 50‘000.- CHF pro Konto zu gehen. Nur Frage ich mich, ob ich dann nicht der Zinseszinseffekt kaputt mache? Denn wenn ich immer in dasselbe Konto einzahle, erhalte ich nicht mehr aus den Zinsen?

Danke für ein Feedback.

Nein, mit mehreren 3a-Konten schmälerst du den Zinseszinseffekt nicht.

Mein persönlicher Tipp: Global 100. Läuft seit Jahren bei mir und wirft aktuell um die 10% Rendite ab.

Guten Start und viel Erfolg!

Gruss

MC