Newsletter

Newsletter

What happens if you leave CHF 10,000 in a savings account for several decades – and what happens if you invest it broadly in equities?

Saving feels safe. Investing money sounds risky. But if you know the figures, you might think otherwise. In this article, we compare the long-term performance of a savings account with the best-known global share index, the MSCI World – with real data, concrete examples and no jargon. You’ll see why the seemingly safe choice can be the more expensive one in the long term – and the role played by an often underestimated effect: compound interest.

Short & sweet

- Investing broadly in equities has historically paid off much more than saving – around 8% a year compared to 1.5% in a savings account, which barely beats inflation.

- Compound interest makes the big difference: if you start early, you make your profits work for you.

- Shares fluctuate in the short term – if you have at least ten years, you can ride out these fluctuations.

- It’s not worth waiting for the perfect moment. Those who invest regularly are better off in the long term.

- This first lesson shows what has been possible historically – no guarantee for the future, but a strong motivation to engage with the topic of investing.

Contents

Investing or saving money? The long-term comparison

Imagine two people. Both have saved 10,000 francs – and neither will need the money for decades to come.

Anna puts her money in a savings account. Safe, convenient, no surprises.

Beat decides differently: he invests in shares – specifically in a fund that contains the largest companies in all industrialized countries, the MSCI World. He buys a small piece of Apple, Nestlé, Toyota and hundreds of other companies at the same time.

In the end, Anna looks at her account: 10,000 has become around 17,000 francs. Not bad – if it weren’t for inflation, which has quietly eaten up most of it.

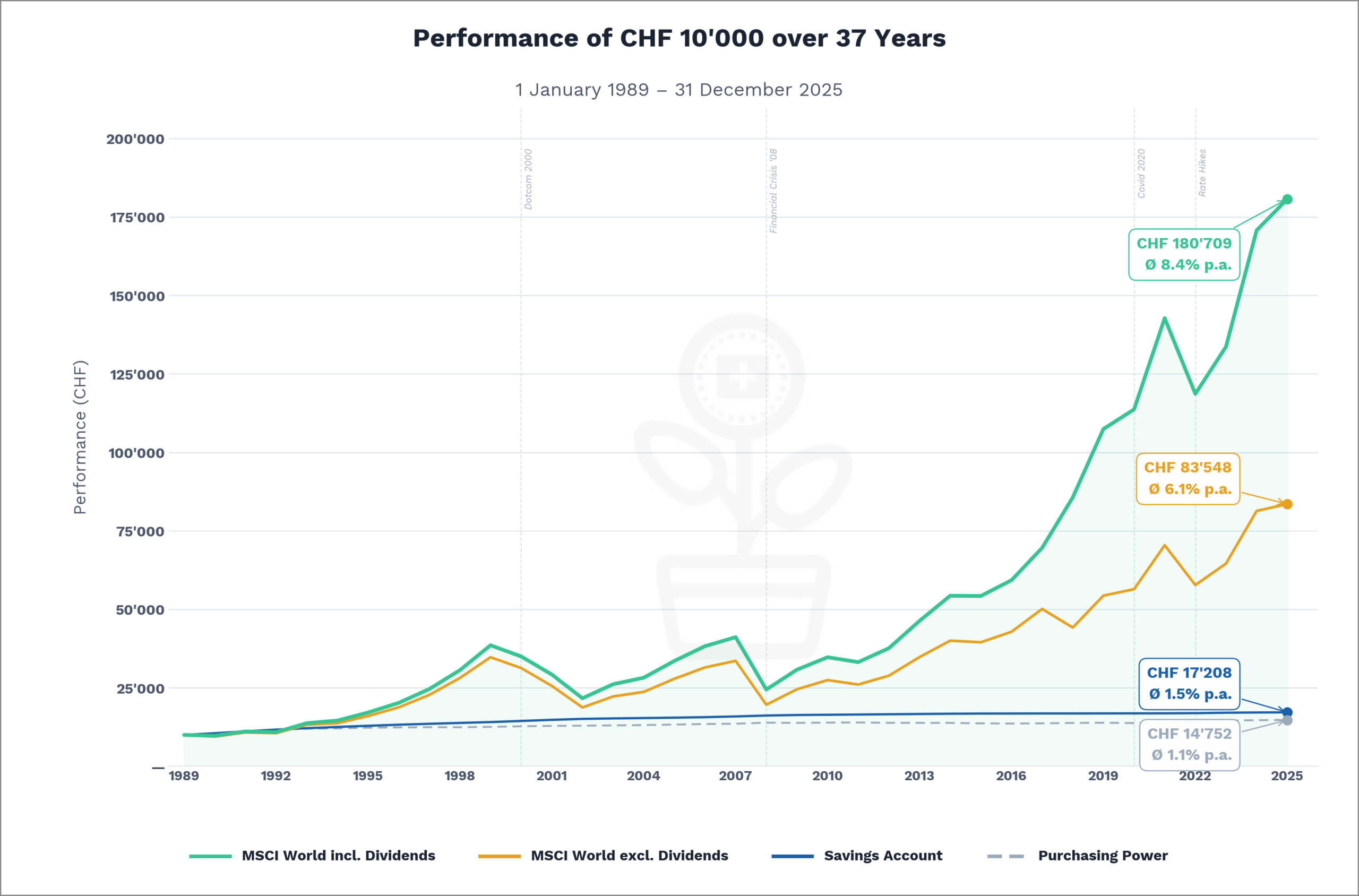

10,000 becomes 180,000 francs

Beat, on the other hand, has over 180,000 francs in his account over the same period – 18 times his original investment, with an average annual return of 8.4%.

How is this possible? The answer lies in three factors – one of which is particularly underestimated:

- Long investment horizon – time is the most important factor

- High returns – equities historically yield significantly more than savings accounts

- Compound interest – profits are continuously reinvested and in turn generate new profits

The uncanny power of the compound interest effect

The decisive factor is what happens to the profits. If the distributed dividends are spent every year, Beat ends up with around CHF 83,000. If, on the other hand, they are automatically reinvested, the money continues to work and in turn generates new profits. Profits on top of profits. Year after year. The result: over 180,000 francs.

The chart clearly shows the difference: in the case of the upper line, the dividends are reinvested – compound interest has a full effect. In the lower line, they are spent – compound interest only has a limited effect via price gains. The gap between the two grows with each year.

This effect is called compound interest. Albert Einstein is said to have once described it as the 8th wonder of the world – and the figures prove him right.

– Partner offers –

Still looking for the right financial solution? Our recommendations – with attractive starting bonuses.

– – – – –

In the long term, we are all dead

Now you might object: I don’t have that many decades. Fair enough.

So let’s assume a shorter investment horizon – let’s say 10 years. In our view, this is the minimum for equity investments. This is because shares can fluctuate very strongly in the short term: In a single year (2008), the MSCI World lost over 40% of its value!

Investing money: When is the right time?

This brings us to the next tricky issue: the supposedly right time to enter the market.

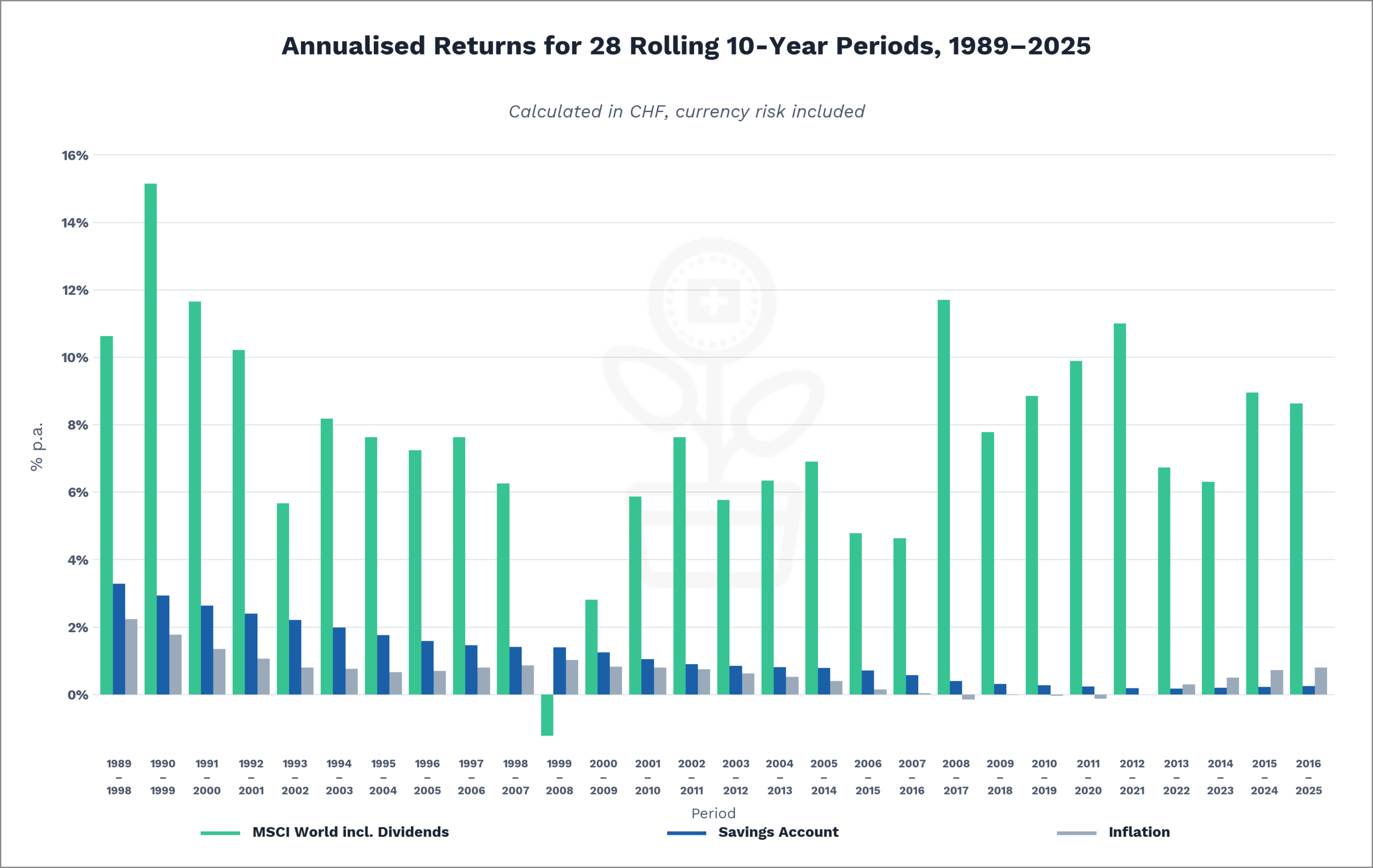

To do this, we let Anna and Beat invest their starting capital of CHF 10,000 in all possible 10-year periods since 1989 – and see what comes out of it.

We also assume that both Anna and Beat leave the income in the form of interest or dividends in their investment. This means that both benefit from the compound interest effect.

In almost all 10-year periods, equity investments yield significantly higher returns than savings accounts – with just one exception.

In Anna’s case, the period 1989-1998 shines with 3.28% per year. The worst period is 2013-2022: a measly 0.17% nominal.

Beat achieved its best return in the period 1990-1999: a whopping 15.14% per year. The worst period was 1999-2008 – an annual loss of 1.23%. Twice as bad luck: Beat entered the market at the dotcom peak of all times, and the 2008 financial crisis wiped out his performance shortly before the sale.

The problem: we don’t know the right time to invest – and those who wait for it often wait too long. The solution is as simple as it is effective: invest money regularly instead of speculating on the perfect moment. If you invest monthly, you sometimes buy expensive, sometimes cheap – and thus smooth out the effects of large price fluctuations over time.

Particularly striking: from the period 2013-2022, savings accounts no longer offset inflation. Anyone who left their money there lost purchasing power in real terms despite nominal interest rates.

For the sake of completeness, we have not taken currency risks, costs and taxes into account in our calculations.

The savings account is free and the annual fees for ETFs are now minimal – often less than 0.2% per year. We will discuss currency risks and taxes in later lessons.

Conclusion

The figures are clear: investing money – long-term and broadly diversified in shares – generates significantly higher returns than a savings account. Compound interest does its work silently and quietly – the longer, the more powerful. There is no such thing as the “right” time to invest – and if you wait, you lose valuable time.

This lesson has shown what was historically possible – not what is guaranteed. Whether and how you invest depends on your personal situation and your risk profile. This is what the next lessons are about.

In lesson 2, we take a closer look: What’s behind the relationship between risk and return – and why is there never one without the other?

You can find an overview of all the lessons here: Learning to invest – in eight lessons.

This might also interest you

Updates

2026-03-11: Text and data updated.

Disclaimer

Disclaimer: Investing involves risks of loss. You must decide for yourself whether you want to bear these risks or not.

Errors excepted: We have written this article about investing money to the best of our knowledge and belief. Our aim is to provide you as a private investor with the most objective and meaningful information possible on the subject of finance. However, should we have made any errors, forgotten important aspects and/or no longer have up-to-date information, we would be grateful if you could let us know.

4 Kommentare

8 übersichtliche Lektionen, toll geschrieben! Auf meinem Blog habe ich eine Finanzwanderroute angelegt 🙂 über dein Feedback wäre ich sehr gespannt! LG Eric

Danke für die Blumen, Eric. Übrigens, eine originelle, gelungene Idee, deine Finanzwanderroute. Viel Erfolg mit deinem Blog!

LG Stefan von SFB

Hallo zusammen

Toller Beitrag zum Thema investieren

Herzlichen Dank Manuel für dein positives Feedback! Stefan & Toni