Welcome to the first article on the Swiss Finance Blog! True to our motto “Independent financial education for successful investing”, we want to get started right away. Specifically, we will turn the wheel back 30 years and compare the performance of a savings account during this period with that of the MSCI World equity index. How much would a deposit at that time be worth today? What role does the time of entry play? And what significance does compound interest actually have? Investing money instead of saving? You will find the answers in this article.

Let’s assume the following scenario: Two people have 10,000 francs at their disposal, which they do not need to draw on for 30 years.

Person A, let’s call her Anna, decides on a safe investment in her savings account at the cantonal bank.

Person B, let’s call him Beat, invests more riskily by means of an exchange-traded equity fund (ETF) in the world equity index MSCI World.

The MSCI World tracks the stock market value of the largest 1,600 or so companies from 23 industrialized countries.

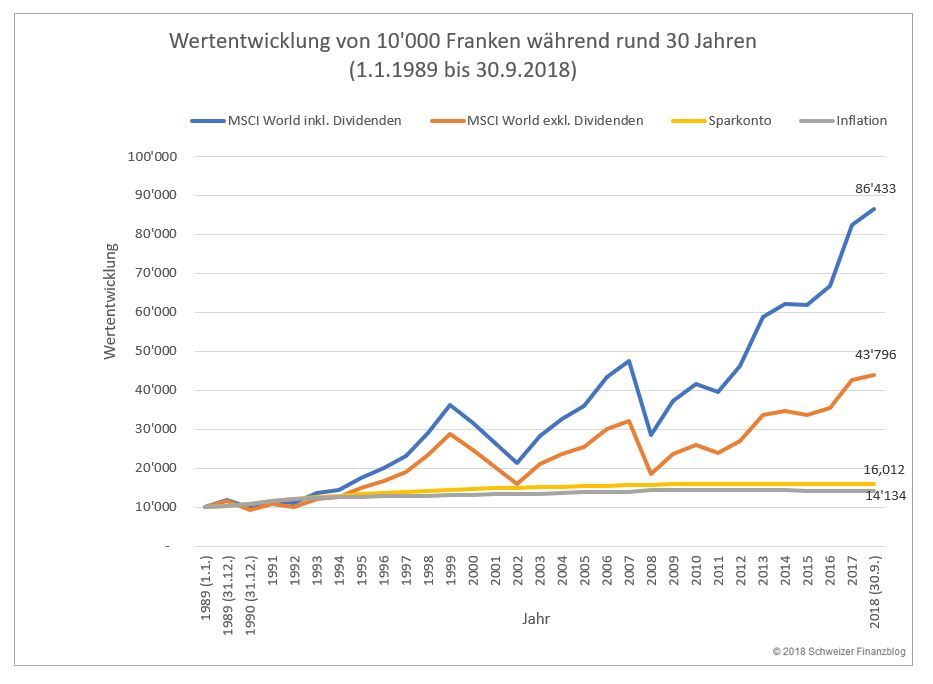

Over the 30-year period from 1.1.1989 to 30.9.2018, Anna was ultimately able to withdraw CHF 16,012 from her savings account (see Figure 1, yellow curve). This corresponds to a nominal increase in value of 60 percent or an average annual return of 1.58 percent.

With a simultaneous inflation rate of 1.16 percent (annualized), Anna will only have a small real increase in value of just under CHF 2,000 after thirty years.

The picture is very different for Beat: if he sells his ETF on the stock market after 30 years, he will have an impressive CHF 85,948 in his account (see Figure 1, blue curve). This corresponds to an increase in value of 760% or an average annual return of 7.45%. Or more than eight times Beat’s original investment.

What seems incredible is easily explained. Three factors play a decisive role:

If Beat had the dividends paid out to him and consumed them, his original investment would “only” have increased fourfold or CHF 43,796 (see Figure 1, orange curve).

The difference of over 40,000 francs is due to the incredible power of compound interest. Albert Einstein is even said to have once described the compound interest effect as the 8th wonder of the world.

Now you may object that we are all dead in the long term or that a 30-year investment horizon is definitely too long.

Agreed. So let’s assume a second scenario, which envisages an investment horizon of only 10 years instead of 30.

In our opinion, this duration should ideally not be undercut when investing in shares.

In contrast to a savings account, shares can fluctuate very strongly in the short term. For example, the MSCI World Index suffered a price loss of over 40 percent in a single year (2008)!

This brings us to the next tricky point: the (supposedly) right time to enter the market.

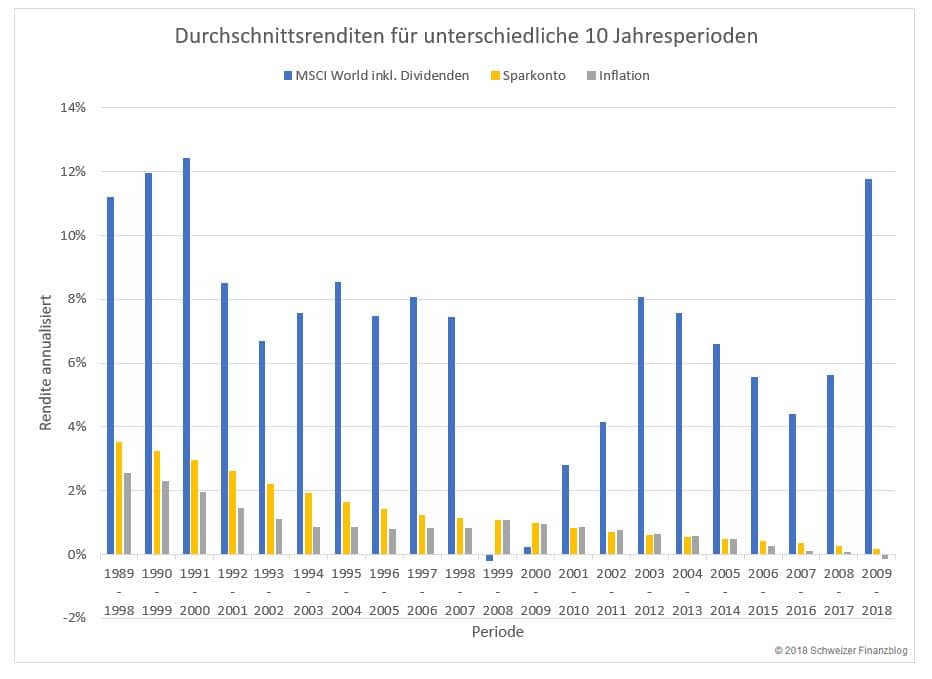

Let’s take our second scenario a step further and let Anna (savings account) and Beat (MSCI World equity ETF) invest their starting capital of CHF 10,000 in all possible 10-year periods since 1989 (see Figure 3).

– Partner offer –

– – – – –

We also assume that both Anna and Beat leave the income in the form of interest or dividends in their investment. This means that both benefit from the compound interest effect.

As Figure 3 clearly shows, the equity investment yields significantly higher returns than the savings account, except for two periods.

For Anna’s savings account, the period 1.1.1989 – 31.12.1998 proves to be the best with an average return of 3.52%. In contrast, the period 1.1.2009 – 30.9.2018 is poor for her, with an average nominal increase of a measly 0.16% per year.

Beat, on the other hand, receives the highest annual return on his equity investment for the period 1.1.1991 – 31.12.2000: 12.44%! In contrast, the period 1.1.1999 – 31.12.2008 is poor for him with a loss of 0.19 percent per year.

The global financial crisis or suprime crisis of 2008, which was triggered by a real estate crash in the USA, thoroughly spoiled its performance shortly before it was sold!

For the sake of simplicity, we have not taken currency risks, product costs and taxes into account in the calculations.

As far as costs are concerned, there are generally no costs for savings accounts. In the case of equity investments, the annual fees (Total Expense Ratio / TER) are now close to zero due to the strong competition on the ETF market and are therefore also negligible.

– Partner Offer –

According to our experience and due to the low costs for ETFs, “DEGIRO” is currently a particularly attractive broker (link to DEGIRO review). If you are interested, you can register with DEGIRO via our partner link , which supports our blog.

– – – – –

Glad you made it this far! Here is a summary of the most important findings:

In the next blog post, we’ll take a closer look at the investment topic and address the question of which factors are decisive when investing money.

You can get a complete overview of the topic of “Investing” here: Learning to invest – in eight lessons.

Disclaimer: Investing involves risks of loss. You must decide for yourself whether you want to bear these risks or not.

Errors excepted: We have written this article to the best of our knowledge and belief. Our aim is to provide you as a private investor with the most objective and meaningful financial information possible. However, should we have made any errors, forgotten important aspects and/or no longer have up-to-date information, we would be grateful if you could let us know.

X

X