Your portfolio is set, your asset allocation is determined – and then the markets do what they want. Prices rise, fall, shift. Suddenly your portfolio no longer matches your risk profile. Does that have to be the case? Not necessarily. In this 5th lesson of our financial guide, you’ll find out how you can rebalance your assets with little effort – and when you can save yourself the trouble.

Rebalancing means adjusting your portfolio back to your target weighting after market fluctuations – no more and no less.

If you hold a single global ETF and a fixed amount of Swiss francs as a low-risk component, you do not need rebalancing.

It becomes relevant if the low-risk portion is defined as a percentage or if different asset classes in the portfolio perform differently.

Checking once or twice a year is sufficient – readjustment is only worthwhile if there is a deviation of 5 percentage points or more, ideally via new deposits rather than sales.

The so-called rebalancing bonus can bring a small additional return, but is a welcome side effect – the real argument remains risk control.

What is rebalancing – and do you even need it?

In the last lesson, you learned how to divide your assets into a high-risk and a low-risk part. The foundation of your portfolio is now in place. But the markets don’t stick to your plan: prices rise and fall, and the weightings shift with them. Rebalancing means restoring the original allocation.

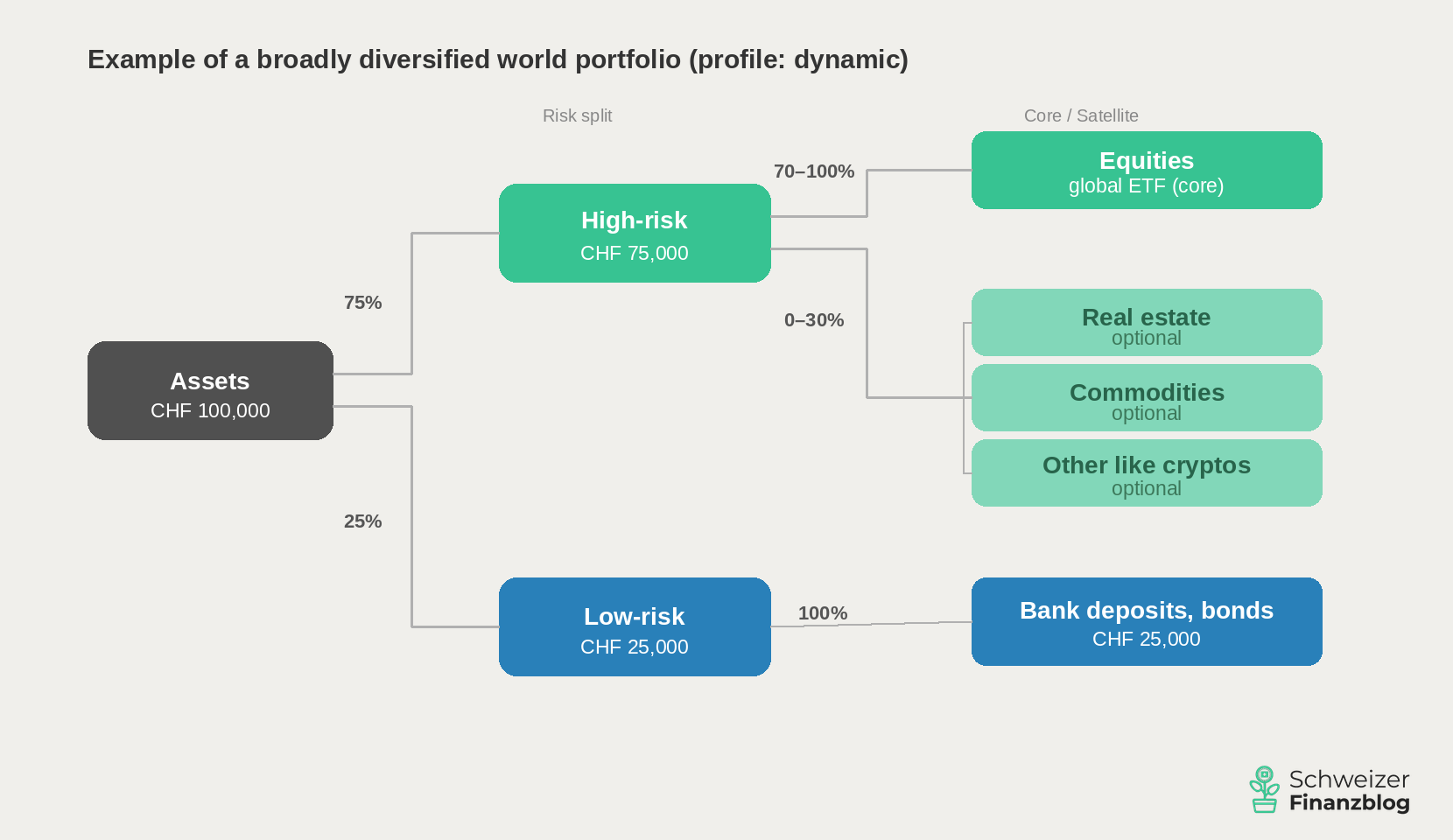

An example: You have invested CHF 100,000 – 75% high-risk, 25% low-risk.

Initial situation: global portfolio with risk split 75/25 and total assets of CHF 100,000; profile: dynamic. (Source: own presentation)

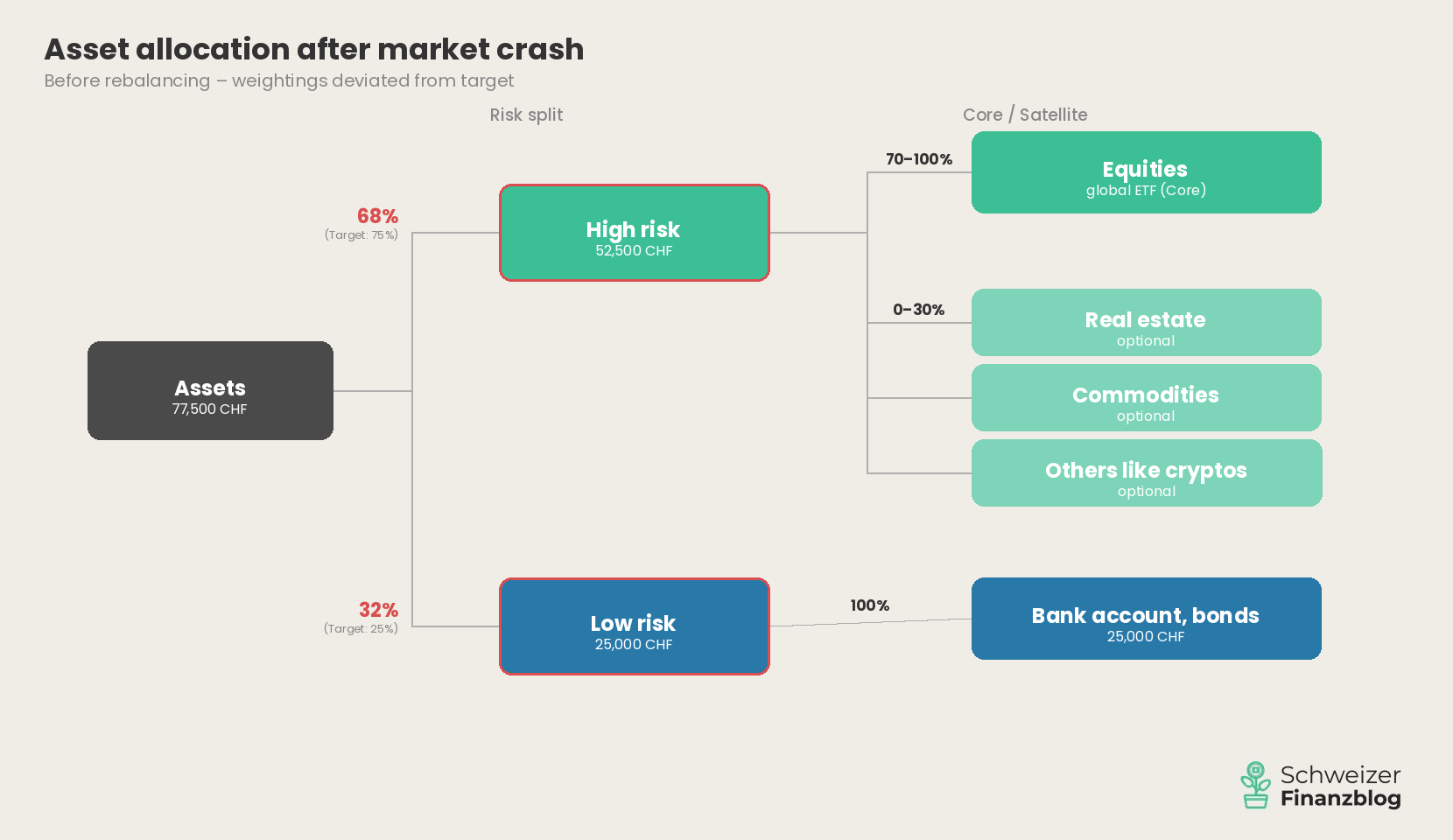

Now the stock markets collapse by 30%. Your risky portion falls from CHF 75,000 to CHF 52,500, while the CHF 25,000 in your savings account remains unchanged. Your total assets now amount to CHF 77,500 – and the low-risk portion is suddenly 32% instead of 25%. Your portfolio is much more conservative than you had planned.

Asset allocation after a price slump of 30% in the high-risk portion. The low-risk portion rises from 25% to 32% – the portfolio is more conservative than planned. (Source: own illustration)

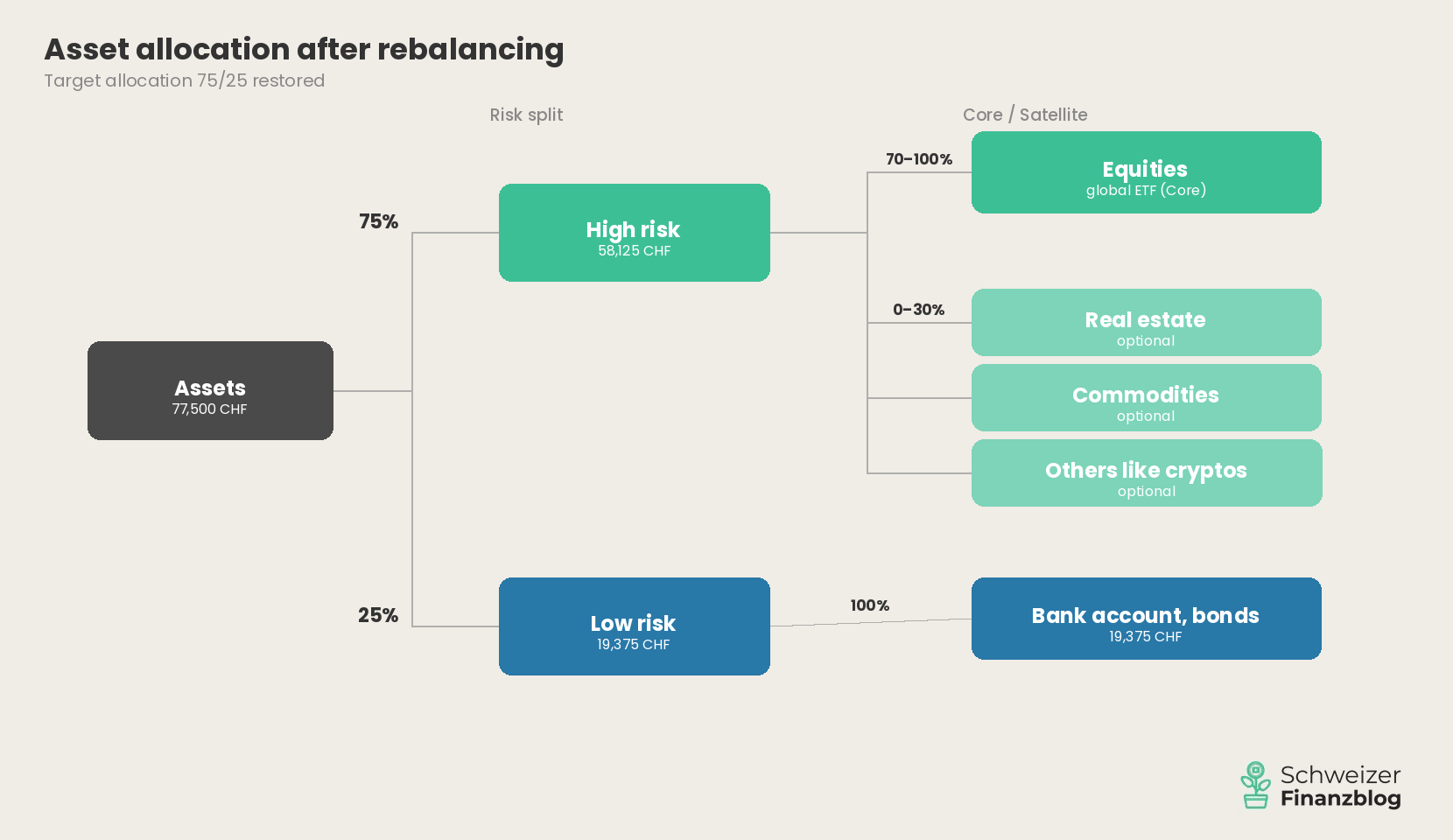

To get back to 75/25, you would have to shift around CHF 5,600 from your savings account to the risky part – after a crash, of all times, when your gut feeling is against it. This is exactly what rebalancing is: a sober, rule-based correction that brings your portfolio back into line with your risk profile.

When you don’t need rebalancing

But before you create a rebalancing calendar now: Not every portfolio needs this correction. If you hold a single global ETF and define the low-risk portion as a fixed amount in Swiss francs – e.g. CHF 25,000 in your savings account, excluding your nest egg – you simply have nothing to rebalance. The ETF is adjusted internally by the provider on an ongoing basis. And a fixed amount does not move, no matter what the markets do. In the same crash, your CHF 25,000 stays where it is. Your risky part has become smaller, but your risk profile has not changed. No need for action.

Rebalancing therefore becomes relevant if the low-risk portion is defined as a percentage (as in the example above) or if the portfolio consists of several ETFs, such as in a core-satellite approach. In both cases, the weightings drift apart over time – and you have to actively readjust them. We will now take a look at how this can be done pragmatically and cost-effectively.

Rebalancing in practice: how to bring your portfolio into balance

Two questions arise: When should you rebalance? And how?

When to rebalance?

In theory, there are two approaches: calendar-based and threshold-based. With the calendar-based approach, you review your portfolio at fixed intervals – about once a year. With the threshold-based approach, you only take action if a deviation exceeds a certain value, e.g. 5 percentage points.

In practice, you can combine the two: You check your portfolio once or twice a year – and only intervene if the deviation is large enough. That’s enough. Rebalancing is not a daily business, but an occasional adjustment.

Three ways to bring your portfolio back into balance

There are basically three methods to bring your portfolio back in line with the target weighting:

Rebalancing: You sell investments that are above their target weighting and use them to buy underweighted positions. Classic, but associated with transaction costs.

Cash flow rebalancing: You direct new deposits – for example from your monthly savings amount – specifically into the underweighted positions. No need to sell, no additional costs. For investors in the savings phase, this is the most elegant approach, which we also follow.

Combination: In the event of minor deviations, readjust by making new deposits. Only in the event of major shifts do you actively reallocate.

Perfection is out of place

If you balance every position exactly to the franc, you will pay unnecessarily high transaction fees – especially for smaller amounts. Concentrate on the biggest deviations. If the overall distribution between the high-risk and low-risk parts is correct again, you can safely ignore minor imbalances within the high-risk part. The next time you make a savings deposit, you can simply adjust them again. As a rule of thumb: If a position deviates from its target weighting by more than 5 percentage points, an intervention is indicated. Below this, the effort is not worthwhile in most cases.

The following graphic shows what this looks like in concrete terms.

Asset allocation after rebalancing. The target weighting of 75/25 has been restored – minor deviations within the risky part are deliberately tolerated. (Source: own presentation)

Good to know: Rebalancing in the deconsolidation phase, 3rd pillar and taxes

De-savings phase

What has been described so far relates to the accumulation phase – i.e. the time in which you build up your assets. But you can also rebalance your assets when you retire. The principle is simply reversed: Instead of targeting new deposits, you first sell positions that are above their target weighting. In this way, you bring your portfolio closer to the target weighting with each withdrawal – without additional transactions.

3rd pillar

If you hold part of your assets in the 3rd pillar: Rebalancing is usually automated here. You enter your risk profile once and the provider takes care of the rebalancing for you – often already included in the management fees. You still have to take care of rebalancing your free assets yourself.

Taxes

Rebalancing generally has no tax consequences for private investors in Switzerland. Capital gains on private assets are tax-free. The only exception: anyone who trades so frequently and on such a large scale that the tax authorities suspect commercial securities trading must pay tax on gains as income. This is not an issue for one or two rebalancing transactions per year.

The rebalancing bonus: a welcome side effect

The main aim of rebalancing is clear: to bring your portfolio back in line with your risk profile. However, there is a pleasant side effect that is known in specialist literature as the rebalancing bonus.

The principle behind it is simple: with rebalancing, you systematically buy investments that have fallen and reduce those that have risen. You are therefore acting anti-cyclically – and it is precisely this behavior that can generate a small additional return in the long term. Various studies put this effect at around 0.1 to 0.5 percentage points per year.

The honest flip side

The rebalancing bonus is not a law of nature. It works best when prices return to the mean after spikes – the so-called regression to the mean. In phases with long-lasting trends, however, rebalancing can slow you down because you sell winners too early. None other than Charlie Munger, Warren Buffett’s partner of many years, firmly rejected rebalancing for precisely this reason: systematically cutting winners slows down the growth of your portfolio.

Then there are the transaction costs. If you have to rebalance with an expensive house bank, you will quickly eat up the bonus again. The rebalancing bonus is therefore only worthwhile with a low-cost online broker where the fees per transaction are low.

Therefore: See the bonus as a welcome extra, not as a guarantee.

“The real argument for rebalancing is not the additional return – but risk control.“

– Partner offers –

Still looking for the right financial solution? Our recommendations – with attractive starting bonuses.

– – – – –

Conclusion

Rebalancing is not a third major investment principle alongside diversification and asset allocation – but the maintenance that ensures that your portfolio remains in line with your risk profile even after market fluctuations.

If you keep it simple – a global ETF and a fixed amount of Swiss francs in your savings account – you don’t need to worry about this. For everyone else: check once or twice a year and readjust if there are major deviations, preferably by making new deposits rather than selling. Perfection is out of place – as long as the overall allocation is correct, you can safely ignore minor imbalances.

In lesson 6, we take a closer look at the investment vehicle that crops up again and again in this guide: the ETF. What’s behind it – and why are we talking about a revolution in private investment?

2026-04-14: Article completely revised and updated.

Disclaimer

Disclaimer: Investing involves risks of loss. You must decide for yourself whether you want to bear these risks or not.

Errors excepted: We have written this article on rebalancing to the best of our knowledge and belief. Our aim is to provide you, as a private investor, with the most objective and meaningful financial information possible. However, if we have made mistakes, forgotten important aspects and/or are no longer up to date, we would be grateful if you could let us know.

How much of your assets should be invested in shares – and how much should stay in your bank account? The answer to this question is the most important decision when investing your money. Not the choice of the right ETF, not the perfect time to start – but the question of how you structure your assets. In this fourth lesson of our financial guide, you will find out how to determine your personal asset allocation step by step and what role your risk profile, liquidity reserve and 3rd pillar play in this.

Asset allocation – the division of your assets into a high-risk and a low-risk part – is the most important decision when investing your money.

Before you invest, you need a liquidity reserve of three to six months’ expenditure. This is not part of the asset allocation.

Your risk profile – consisting of risk appetite and risk capacity – determines the weighting. The more cautious of the two factors sets the framework.

Broadly diversified equity ETFs are at the heart of the risky part. The simplest solution: a single global ETF. If you want, you can add according to the core-satellite principle.

The low-risk part – bank deposits and possibly bonds with a high credit rating – offers hardly any return, but stability, flexibility and rebalancing ammunition.

Make a note of your target allocation. It is your fixed star – and worth more than any hot investment tip in the next stock market crisis.

What does asset allocation mean?

The term asset allocation is based on a simple idea: the structuring of your assets. Specifically, it’s about how you distribute your money across different asset classes – how much goes into shares, how much stays in your bank account, how much you put into real estate or other investments?

If diversification is the blueprint, then asset allocation – or your asset structure – is the foundation of your house. It determines how stable the building is, not the color of the walls or the model of the kitchen. Numerous studies confirm exactly this: it is not the choice of individual products, but the allocation of your assets that has the greatest influence on long-term investment success. You base all other investment decisions on your asset allocation.

Before we get into the details, it’s worth taking a look at the big picture. Your assets can be divided into three areas that fulfill different tasks:

The liquidity reserve: your safety net

Every sound financial plan includes a liquidity reserve – a nest egg of three to six months’ expenses in your bank account. This reserve serves to cushion unforeseen expenses such as job loss, illness or major repairs without you having to touch your investments.

Even if the liquidity reserve is also held in a low-risk bank account, it is not part of your asset allocation. The difference is that the low-risk portion of your investment is a conscious strategic decision within your portfolio. The liquidity reserve, on the other hand, is a requirement that must be met before you even think about investing. It is reserved for emergencies – and therefore taboo for investment purposes. Repaying any consumer loans also has priority – their interest rates exceed any realistic investment return.

Only what remains after your nest egg and debt reduction is your freely available investment capital. And it is precisely these assets that are now structured using asset allocation.

Your risk profile determines the allocation

How you allocate your disposable assets depends on your individual risk profile – i.e. the interplay between your risk appetite and your risk capacity, which we covered in detail in lesson 2.

As a reminder: risk appetite describes how much price loss you can withstand without lying awake at night or selling in a panic. Risk capacity describes how much loss your wallet can take without you getting into financial difficulties – determined by your initial financial situation and your investment horizon.

Both factors must be in harmony. An example: You are young, earn well and could easily cope financially with a 50% drop in the share price. But at minus 20% you get nervous and sell. In this case, it is not your risk capacity that is decisive, but your risk appetite – this sets the narrower limit. Conversely, if you consider yourself a risk-taker but want to buy an apartment in three years’ time, you should stick to the lower risk capacity. In short: the more cautious of the two factors sets the framework.

From theory to practice: dividing up your assets

Based on your risk profile, you divide your freely available investment assets into two parts: a high-risk part and a low-risk part. As a rule of thumb, the higher the proportion of equities, the higher the risk – but also the higher the return – of your portfolio.

Let’s assume fictitious fixed assets of CHF 100,000 – your nest egg is already secured. You have a regular income and have your running costs under control. Five typical breakdowns for your assets:

Risk profile

High risk*

Low risk**

Defensive

0-20%

80-100%

Conservative

20-40%

60-80%

Balanced

40-60%

40-60%

Dynamic

60-80%

20-40%

Offensive

80-100%

0-20%

*Equities, optionally supplemented by real estate, commodities, cryptos or other asset classes; **Bank deposits, possibly bonds with a high credit rating (e.g. Swiss government bonds)

For the offensive profile, we recommend an investment horizon of at least 10 years due to the high susceptibility to fluctuations. More conservative models with a low equity component, on the other hand, are also suitable for shorter periods.

The risky part: equities in the core, additions in the satellite

The risky part is the return driver of your portfolio – and its most important component is equities.

“In the risky part, you can’t avoid stocks.“

Specifically, it fulfills four tasks:

Long-term wealth accumulation: Shares are the asset class with the highest historical returns – and compound interest ensures that your money grows exponentially over decades.

Inflation protection: While bank deposits lose value in real terms, shares offer effective long-term protection against inflation.

Participation in the global economy: With a global ETF, you benefit from the growth of thousands of companies – without having to analyze a single one.

Passive income: Broadly diversified equity ETFs pay out dividends regularly – either directly to your account or automatically reinvested, depending on the fund, which increases the compound interest effect.

ETFs that track broad market indices from all regions of the world are particularly suitable investment vehicles. You can find out why we consider ETFs to be particularly attractive when investing in lesson 6.

A global ETF as a foundation

The simplest and most elegant solution: with a single global ETF – such as the Vanguard FTSE All-World or an MSCI ACWI ETF – you invest in thousands of companies from industrialized and emerging countries, weighted by market capitalization. A single purchase, global diversification, minimal effort. This is the core idea behind passive investing – and for most investors, it’s the ideal way to get started.

Targeted additions according to the core-satellite principle

If you want to go beyond this foundation, you can apply the core-satellite approach from lesson 3. The core – 70 to 100% of the risky part – remains a broadly diversified equity ETF. If you wish, you can supplement the remainder up to a maximum of 30% in the satellite with targeted additions:

Real estate with globally diversified REITs (real estate investment trusts) can improve the risk/return ratio due to their sometimes lower correlation to the stock market.

Commodities such as gold can serve as inflation protection and a crisis buffer – but do not generate any current income.

Cryptocurrencies such as Bitcoin are among the most volatile asset classes of all – anyone investing here should be able to withstand strong fluctuations and only use money that they can do without in extreme cases.

Other options such as collectibles, crowdlending, factor ETFs or individual shares are conceivable for risk-takers – as a small addition, not as a core component.

Rule of thumb: the more exotic the investment, the lower its weighting.

The low-risk part: security and availability

The low-risk part is the anchor of stability in your portfolio – and the calming pill for your nerves. If the stock markets plummet by 30% again, it is this part that ensures that you remain calm. Specifically, it fulfills three tasks:

Psychological anchor: If not everything is red, it’s easier to keep going and make better decisions.

Flexibility: If your circumstances change unexpectedly – new job, relocation, unplanned expenses beyond your nest egg – you have room to maneuver.

Rebalancing ammunition: After a crash, you can buy additional shares at a low price and rebalance your portfolio (more on this in lesson 5).

Bank balances – in savings or private accounts – are the simplest and most liquid option. You can access them at any time. In Switzerland, deposits of up to CHF 100,000 per person and bank are protected by the deposit guarantee scheme. The expected return is clear: at best some protection against inflation, but no real asset growth. That’s not the purpose of this part – it’s to give you security and the ability to act.

Bonds with a high credit rating – such as Swiss government bonds with a top rating of “AAA” – also offer a high level of security. However, their yield in Switzerland is historically close to inflation. Anyone hoping for a significant return after deducting inflation will generally be disappointed with Swiss bonds. However, they can still play a role as a stabilizer in a portfolio – especially for investors with a balanced or conservative profile.

Other options such as medium-term notes or fixed-term deposits offer slightly higher returns than a savings account, but tie up the capital for a fixed term. You can find an overview of this in lesson 2.

“Determining your individual asset allocation tailored to your risk profile is the be-all and end-all of your investment.“

Exemplary asset structure for people with a dynamic risk profile – the second-highest of five risk levels. The core consists of a single global equity ETF (e.g. FTSE All-World or MSCI ACWI). Satellite positions such as real estate, commodities or cryptocurrencies are optional. In the low-risk section, bank deposits and, if necessary, bonds with a high credit rating provide stability. The liquidity reserve is not shown – it is not part of the asset allocation. (Source: own illustration)

And what about pillar 3a?

A question we are asked time and again: Where in my asset allocation do the 3a assets actually belong – low-risk or high-risk?

Our answer: Neither. Your 3a assets are tied pension assets – you cannot simply withdraw them if you want to. Early withdrawals are only possible in a few cases, such as when buying a home, emigrating or becoming self-employed. Pillar 3a therefore does not belong in the same drawer as your disposable assets, but follows its own rules.

But that doesn’t mean you should ignore them – on the contrary. If you still have 10, 20 or more years until retirement, you are sitting on an enormous compound interest lever. And this is precisely why we recommend investing your 3rd pillar in equities. The biggest return guzzler here? The fees. Traditional bank products often charge 1% or more per year – sounds like little, but can add up to tens of thousands of francs in lost returns over the long term. Low-cost online providers with fees of less than 0.5% make a huge difference here.

– Partner offers –

Still looking for the right financial solution? Our recommendations – with attractive starting bonuses.

– – – – –

Conclusion

Asset allocation is the most important decision in your investment – more important than the choice of individual products, more important than the time of entry, more important than the question of whether to buy ETF A or ETF B. It is your fixed star to which you align all other investment decisions.

The principle is simple: first secure your liquidity reserve. Then divide your freely available assets into a high-risk and a low-risk part based on your risk profile. In the high-risk part, broadly diversified equity ETFs are at the core – if you wish, you can supplement them with additions according to the core-satellite principle. In the low-risk part, bank deposits provide stability and peace of mind. You view your 3a assets separately – equity-based and cost-effective.

Make a note of your target allocation – so that you can monitor it periodically and take countermeasures if necessary. Because when shares rise or fall, the weighting shifts automatically. In our next lesson, we will look at how you can restore your original portfolio structure easily and cost-effectively: rebalancing.

2026-04-10: Article completely revised and updated.

Disclaimer

Disclaimer: Investing involves risks of loss. You must decide for yourself whether you want to bear these risks or not.

Errors excepted: We have written this article on asset allocation to the best of our knowledge and belief. Our aim is to provide you as a private investor with the most objective and meaningful financial information possible. However, if we have made any errors, forgotten important aspects and/or are no longer up to date, we would be grateful if you could let us know.

Why does a broadly diversified portfolio beat the supposedly smartest stock tip? The answer lies in one of the most powerful concepts of modern financial theory – and in the only real “free lunch” in investing. In this third lesson of our financial guide, you will find out how to use diversification effectively in two stages, where its limits lie and what this means for your wealth accumulation.

Diversification is the only “free lunch” in investing: You get the same return potential with less risk.

Before you invest, you should meet two basic requirements: a nest egg of three to six months’ expenditure and no outstanding consumer loans.

Level 1: Diversify your shares globally and across sectors – this eliminates company-specific risk.

Level 2: If you want to go one step further, combine different asset classes – bonds, commodities and alternative investments can reduce fluctuations or open up additional opportunities for returns.

With the core-satellite approach, you maintain discipline in the foundation and scope for targeted positions in the satellite.

Stock picking can increase returns – but can also lead to a total loss. Even professional fund managers regularly fail to beat the market in the long term. This is why diversification is generally the more promising approach – and scientifically sound.

Resisting the temptation of stock-picking

Admittedly: It’s not easy to resist the supposedly safe stock tip with rosy profit prospects from a trusted acquaintance. But it’s definitely necessary!

“The hunt for individual stocks, also known as stock-picking, can backfire badly.“

If you invest in a single stock, substantial price losses with no prospect of a sustained recovery are unfortunately an all too realistic scenario. And it’s not just exotic stocks that are affected, but also well-known and established Swiss companies.

The Swatch Group, once a popular stock on the Swiss stock exchange, has lost around 70% of its value since its high in November 2013 – as the chart clearly shows.

Swatch Group share price performance since 1997: Despite interim highs of over CHF 600, the share price at the beginning of 2026 is below the 2006 level (Source: Google Finance, April 2, 2026)

The worst case is even more drastic: bankruptcy. Swissair, once the nation’s proudest airline, had to stay on the ground in October 2001 – shareholders lost everything. Investors in Credit Suisse did not fare much better: Once one of the largest banks in the world, it was taken over by UBS on an emergency basis for little money in March 2023 following a crisis of confidence. Shareholders lost practically everything.

Incidentally, the opposite of stock-picking is not necessarily passive investing – even actively managed funds often hold hundreds of stocks and are therefore broadly diversified. The actual counter-concept is the concentration on a few stocks. And it is precisely this concentration that increases risk – without increasing returns.

But concentration is not only evident in stock picking. Anyone who keeps their entire assets in a savings account is also concentrating on a single form of investment – with the difference that the threat here is not price losses, but a creeping loss of purchasing power due to inflation. And the compound interest effect, which makes the decisive difference in the long term, has virtually no effect. We showed how big this difference is over decades in lesson 1.

You can find out how diversification solves this risk – and what the science says about it – in the next chapter.

What is behind diversification? The theory in a nutshell

This brings us to Harry Markowitz’s Modern Portfolio Theory (MPT). He was awarded the Nobel Prize in Economics in 1990 for his groundbreaking doctoral thesis.

Markowitz was the first to provide theoretical proof of the positive effect of diversification on the risk and return of an overall portfolio. The core of his theory is the distinction between systematic and unsystematic risk.

All securities on the market are subject to systematic risk – i.e. market risks such as interest rate rises, recessions or political instability. It cannot be diversified away and is simply the price of investing itself.

The unsystematic risk, on the other hand, is the company-specific risk – such as management errors as in the VW emissions scandal. This risk can be reduced through diversification. And that is the key point: the market compensates you for the systematic risk – but not for the unsystematic risk. So if you invest in individual stocks, you are taking on unnecessary risk without being able to expect higher returns.

“Company-specific risk can be reduced through diversification – market risk cannot.“

You will achieve the strongest diversification effects if you combine investments with the lowest possible correlation. The range extends from +1 (same development) to 0 (independent development) to -1 (opposite development). Within the equity asset class, typical correlations are between 0.70 and 0.95 – the effect is real, but limited. The combination of different asset classes brings significantly more, as we will see below.

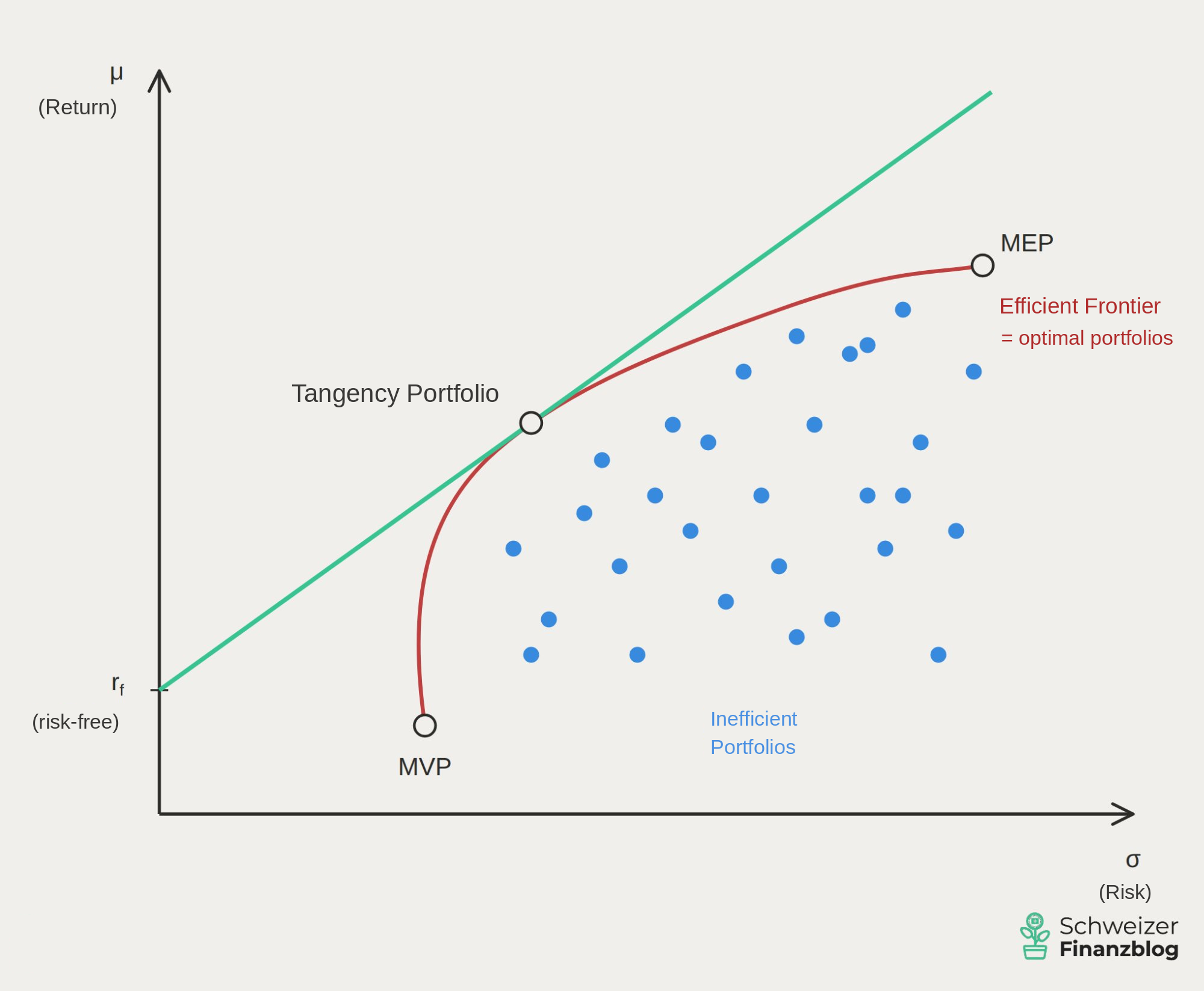

The efficiency line: what makes an optimal portfolio

Markowitz not only showed that diversification reduces risk – he also specified the minimum amount of risk that must be taken for a given return. The result is the efficient frontier.

The efficiency line is created by plotting all conceivable portfolio combinations in a diagram – with the risk on the x-axis and the expected return on the y-axis.

Portfolios on the curve are efficient: they achieve the maximum possible return for a given risk. Portfolios below the curve are inefficient – too much risk for too little return. Portfolios above the curve are simply not achievable.

Not every portfolio is equally good: the blue dots show inefficient portfolios – they deliver too little return for the risk taken. The relationship between risk and return is only right on the red efficiency line. Three points stand out: the MVP (minimum variance portfolio) at the lower end with the lowest risk, the MEP (maximum return portfolio) at the upper end with the highest return and in between the tangential portfolio – the portfolio with the highest return per unit of risk taken.

“Diversification is the only free lunch in investing: same expected return – but less risk.“

A global equity ETF such as the FTSE All-World is close to the MEP – the maximum return portfolio at the upper end of the efficiency line. A single stock such as the Swatch Group, on the other hand, lies to the right of the curve: with the same or even lower expected return, you bear significantly more risk – without being compensated for it. This is precisely the “free lunch” of diversification: not more return, but less risk with the same expected return.

Diversification in practice – two stages

Theory is nice – but how do you put diversification into practice? And how far do you have to go? The old stock market adage that you shouldn’t put all your eggs in the same basket comes in two stages. But first you should fulfill an important prerequisite.

The nest egg. Before you invest, you should keep a bank balance of three to six months’ expenses as a liquidity reserve. This reserve serves to cushion unforeseen expenses – due to job loss, illness or repairs – without you having to touch your investments. Paying off any consumer loans also has priority, as their interest rates exceed any realistic return on investment. Only once you have built up this reserve and are free of consumer debt can you really invest the rest of your assets for the long term.

Level 1 – Diversification within the equity asset class

Let’s start with the most important level: broadly diversify shares. A simple rule of thumb helps with orientation:

No-go: individual shares If you only hold one share, you bear the full company-specific risk. Total loss – as with Swissair – is not a theoretical scenario.

Suboptimal: few Swiss stocks Many people tend to overweight domestic stocks – the so-called home bias. Understandable, but structurally problematic: the Swiss market is heavily concentrated in three sectors (pharmaceuticals, financials, consumer goods) and accounts for less than 3% of global market capitalization.

Recommended: Global and cross-sector A global ETF on the FTSE All-World or MSCI ACWI comprises thousands of companies from all over the world. The company-specific risk is practically eliminated – and you simply don’t care whether individual companies rise or fall in the index.

Global beats Switzerland beats CH stocks. Swatch Group is down after 20 years – while the broad global index has more than tripled the capital invested. A clear argument for global diversification in the portfolio. (Source: Own presentation based on stock market data from Google Finance / SIX; period January 6, 2006 to March 31, 2026; SMI and Swatch Group in CHF, FTSE All-World in USD; excluding dividends, not adjusted for inflation)

Caution: limited cluster risk also in ETFs

Anyone who buys an MSCI World ETF and thinks they are perfectly diversified should take a closer look: Around 70% of the index is made up of US equities, of which over 20% is made up of the seven largest technology companies alone (“Magnificent Seven”). In addition, the MSCI World only covers developed markets of large and medium-sized companies – emerging markets such as China, India or Brazil are not included. If you want real geographical diversification, you have two options: either supplement the emerging markets component with a separate ETF, or invest directly in an MSCI ACWI or FTSE All-World, which already include emerging markets. If you want to go one step further, add a small-cap ETF to your portfolio – and thus also include smaller companies.

The legislator also has diversification rules: For UCITS funds – the standard structure of most ETFs available in Switzerland – the so-called 5-10-40 rule applies: individual positions exceeding 5% of the fund assets may not account for more than 40% in total. UCITS is not a must, but a quality feature designed to protect investors. Other ETFs – such as those that track the best-known Swiss index SMI – do not meet the requirements, as Nestlé, Novartis and Roche together regularly make up more than 50% of the index. So if you want to invest in a well-diversified way, you should pay attention to the UCITS label.

Excursus: Currency risk – an issue for Swiss investors

If you invest globally, you automatically invest in foreign currencies – around 60% of a FTSE All-World consists of US dollar securities. The decisive factor here is not whether you buy your ETF in CHF or USD, but in which currency areas the companies in the fund operate.

Is that a reason to forego global diversification? No. In the long term, the diversification benefits clearly outweigh the disadvantages, and currency fluctuations are partially balanced out over time. Currency-hedged ETFs do exist, but they cost more and eat into returns in the long term. For most investors with a long-term horizon, the currency risk is simply bearable – and part of the package.

Conclusion on diversification level 1

In combination with a solid liquidity reserve in your bank account, you are already well positioned with level 1 – a global equity ETF covers the most important aspects. But if you want to go one step further – reduce fluctuations or tap into additional return opportunities – you can combine different asset classes. This is level 2.

Level 2 – Diversification across asset classes

The combination of different asset classes is even more effective than diversification within equities – because their correlations with each other are significantly lower than within the equity asset class. While equities from different markets still have correlations of 0.70 to 0.95, the correlations between equities and other asset classes are often significantly lower – in some cases close to zero or even negative. The lower the correlation, the greater the diversification effect.

Bonds

Bonds often move in the opposite direction to equities – in times of crisis, bond prices rise when everyone is looking for safety. However, this is not always the case: in 2022, both equities and bonds fell massively in value when the central banks drastically increased interest rates. Bonds are therefore not a panacea, but can be a valuable portfolio anchor over long periods of time.

A classic example is the 60/40 portfolio: 60% global equities, 40% bonds. For decades, this has been a proven starting point for people with a balanced investment approach – more stability, but also lower returns than with pure equity investments. Anyone with a long investment horizon and a focus on maximum growth will find bonds to be a drag on returns. The right weighting ultimately depends on the individual risk profile – precisely the topic of the next lesson.

Alternative investments as an admixture

Anyone wishing to expand their portfolio beyond traditional asset classes will find further sources of diversification in the area of alternative investments – with different return, risk and liquidity profiles.

Real estate Real estate ETFs are the most accessible entry into “concrete gold” – without a mortgage, condominium owners’ association or administrative expenses. They offer regular income, but are sensitive to changes in interest rates and are not completely decoupled from the stock markets.

Commodities Gold, oil and industrial metals often act as a hedge against inflation and have low correlations with equities. Gold in particular has acted as a safe haven in many crises. However, commodities do not generate current income such as dividends or interest.

Crowdlending P2P lending – direct lending to private individuals or SMEs via online platforms – can generate attractive returns. But the risks are real: during the coronavirus crash in 2020, several platforms froze payouts, and Estateguru ‘s returns plummeted from double digits to zero for many – high default rates on German real estate loans still weigh on the platform today. Conceivable as a small addition for risk-takers – not as a core component.

Collectibles Collector’s items – Art, watches, whisky, sports cards – are considered inflation-resistant and have little correlation with financial markets. Investments from as little as EUR 50 are possible via platforms such as Splint Invest. The downsides: low liquidity, assets that are difficult to value and no ongoing income.

Cryptocurrencies Bitcoin & Co. are among the most volatile asset classes of all – anyone investing here should be able to withstand strong fluctuations and only use money that they can do without in extreme cases.

Conclusion on diversification level 2

All asset classes can be a useful addition to the portfolio – but none can replace the stable foundation of diversified equity ETFs. The golden rule: the more exotic the investment, the smaller its weighting should be.

The pragmatic middle way: the core-satellite approach

The core-satellite approach elegantly resolves the apparent dilemma between diversification and concentration. The idea is simple:

Core– 70-100% of the portfolio One or two broadly diversified ETFs – such as MSCI ACWI or FTSE All-World – form the stable foundation. There is no speculation here, assets are built up over the long term. People with a more balanced investment approach can also supplement the core with bonds.

Satellite– optional 0-30% There is room here for targeted positions – individual countries or sectors, factor ETFs, individual shares or alternative investments such as real estate ETFs, P2P lending, collectibles or cryptos. These positions can beat the market, but they don’t have to. Their loss does not jeopardize the overall portfolio.

The key advantage: you keep the discipline of diversification at the core without sacrificing the joy of active investing. And you always know what is at stake.

The honest flip side: diversification vs. concentration

Here’s a point that financial blogs often fail to mention because it seems to undermine the main message. But it is part of the truth:

Exceptional returns come from concentration, not diversification.

Warren Buffett achieved his excess returns by betting massively on a few carefully selected companies. Private equity funds also outperform the market – if they do – through concentrated bets. Anyone who had bet everything on Nvidia or Apple in the past would be rich today.

That sounds tempting – but it is not a realistic path for the vast majority. And for one simple reason: concentration not only increases the opportunities, but also the risks. For every Buffett, there are hundreds who have backed the wrong horse and suffered total losses. Excess returns through concentration require sound analysis, a robust psychological profile, a lot of time – and above all a considerable amount of luck.

For most private investors, diversification is therefore not the path to super returns – but it is the path to solid, risk-adjusted returns over decades. And that is exactly what sustainable wealth accumulation means in practice.

– Partner offers –

Still looking for the right financial solution? Our recommendations – with attractive starting bonuses.

– – – – –

Conclusion

Diversification is not a lazy compromise – it is the only proven “free lunch” in investing: same return potential, less risk. If you accumulate individual securities, you take on unnecessary risk without any corresponding return compensation. And if you park your assets in a savings account, you avoid price fluctuations – but you pay a different price: gradual loss of purchasing power due to inflation and lost compound interest.

Even the first stage – a global equity ETF combined with a solid liquidity reserve – forms a solid foundation. If you want to go further, you can also diversify across different asset classes – with a sense of proportion.

The core-satellite approach combines the best of both worlds: a stable foundation thanks to diversification and scope for targeted positions thanks to controlled concentration.

In the fourth lesson of this financial guide, we start right here and look at asset allocation – in other words, the question of how you distribute your total assets across the various asset classes in line with your individual risk profile.

2026-04-10: Commodities and cryptocurrencies added to the alternative asset classes.

2026-04-06: Article completely revised and updated.

Disclaimer

Disclaimer: Investing involves risks of loss. You must decide for yourself whether you want to bear these risks or not.

Errors excepted: We have written this article on investment diversification to the best of our knowledge and belief. Our aim is to provide you as a private investor with the most objective and meaningful financial information possible. However, if we have made mistakes, forgotten important aspects and/or are no longer up to date, we would be grateful if you could let us know.

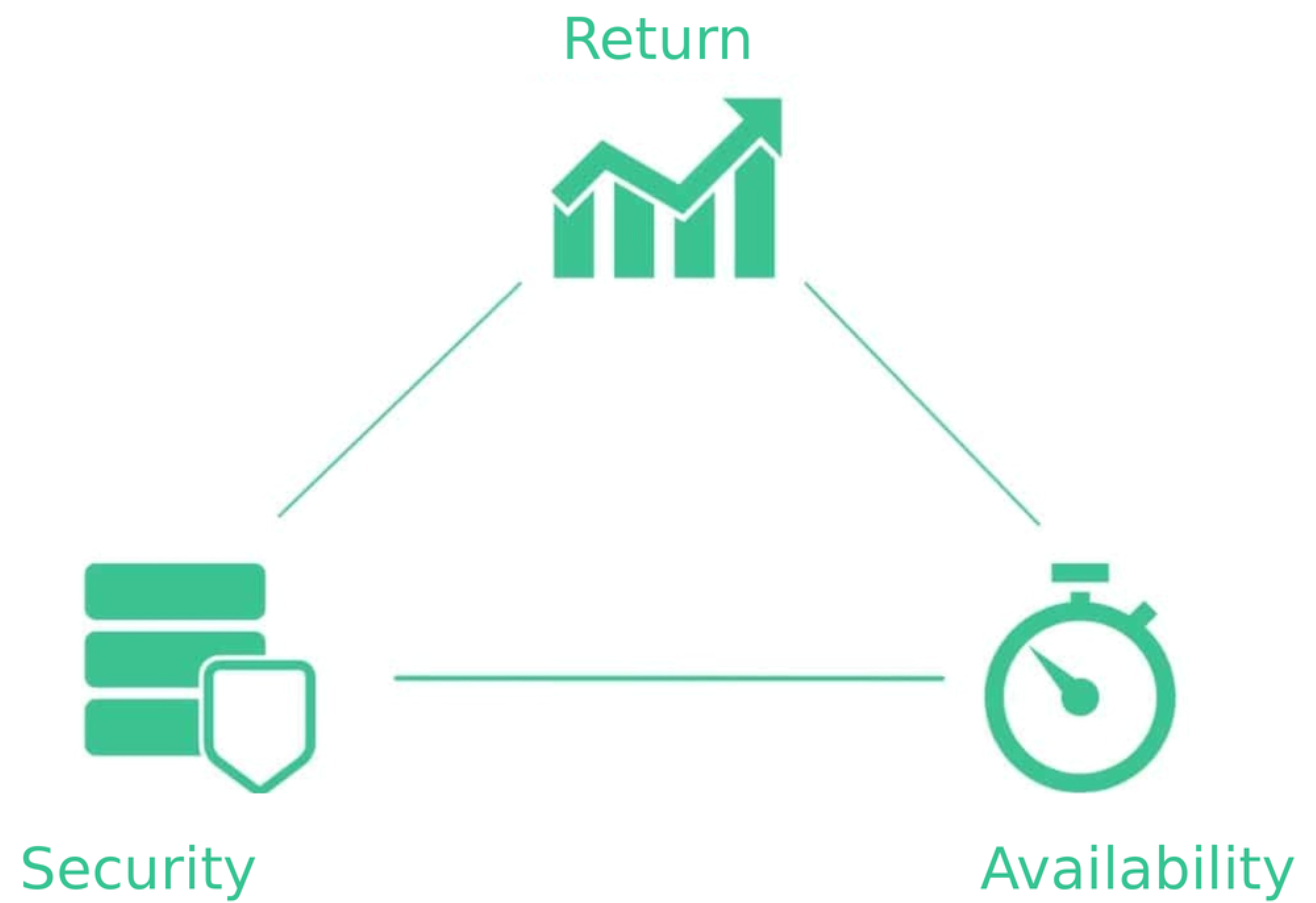

Why does one investment yield an attractive return while another barely beats inflation? The answer lies in the magic triangle of investing – and in a conflict of objectives that no one can escape. In this second lesson of our financial guide, you will find out which three factors are decisive for your wealth accumulation, how they depend on each other and which goals you can pursue at the same time – and which not.

The magic triangle of investment shows that returns, availability and security cannot be maximized at the same time.

If you prioritize two of these goals, you will inevitably have to cut back on the third – this applies to every asset class.

Shares offer returns and availability, but little security. The bank account is safe and available, but offers little return. Medium-term notes or fixed-term deposits offer security and slightly higher returns – but the capital is tied up.

Which combination is the right one depends on your risk profile – there is no universal best answer.

What is the magic triangle of investing?

The magic triangle of investment describes the three competing goals of investment: return, availability and security. The illustration below symbolizes these goals with the corner points of a triangle.

The magic triangle of investing: return, availability and security – the three competing goals of your wealth accumulation.

Returns: What are the benefits of the investment?

The yield describes the return on an investment and is the most important starting point for many investors. Typical sources of income are dividends, interest payments or price gains.

As a rule, the higher the targeted return, the greater the risks taken – there is no such thing as a consistently high return without corresponding fluctuations. This is precisely where the conflict of objectives in the magic triangle of investment begins.

For long-term wealth accumulation, it is crucial that income is reinvested wherever possible. The compound interest effect ensures that assets can grow exponentially over time.

The return after costs, taxes and inflation is also important: fees and inflation can significantly reduce the real return. For long-term investments in particular, it is therefore worth paying attention to cost-effective and efficient products – such as broadly diversified ETFs that track an entire asset class such as equities at low cost. Our article Best ETFs Switzerland and globally shows which ones are particularly convincing.

Availability: How liquid is the investment?

Availability – often also referred to as liquidity – describes how quickly an investment can be converted back into cash or bank deposits. The shorter this period is, the more liquid the investment is.

Not only the time, but also the costs of the conversion play a role. Sales fees, spreads or any penalty costs can reduce the amount actually available.

Liquidity depends heavily on the asset class: Exchange-traded securities such as ETFs or shares can be sold every trading day, while real estate or private equity investments are much less flexible.

In the context of the magic triangle, it is clear that high availability often comes at the expense of returns or security. If you want to access your money quickly, you usually have to compromise on one of the other two factors.

Security: How safe is my capital?

Security refers to the preservation of the invested assets. It describes the extent to which an investment is subject to fluctuations and how high the risk of permanent loss is.

Diversification is an important factor in increasing security. Risks can be reduced by spreading across different asset classes, regions and sectors.

At the same time, there is no such thing as absolute security with yield-oriented investments. Even broadly diversified portfolios are subject to short-term fluctuations.

In the magic triangle of investment, security is in conflict with returns and availability. Higher security often goes hand in hand with lower expected returns or limited flexibility.

Only two goals can be achieved at the same time

The magic triangle of investment makes it clear that all three goals – return, availability and security – cannot be maximized at the same time. If you prioritize two of them, you will inevitably have to compromise on the third. This basic rule applies regardless of the asset class or market environment.

There are three specific variants to choose from:

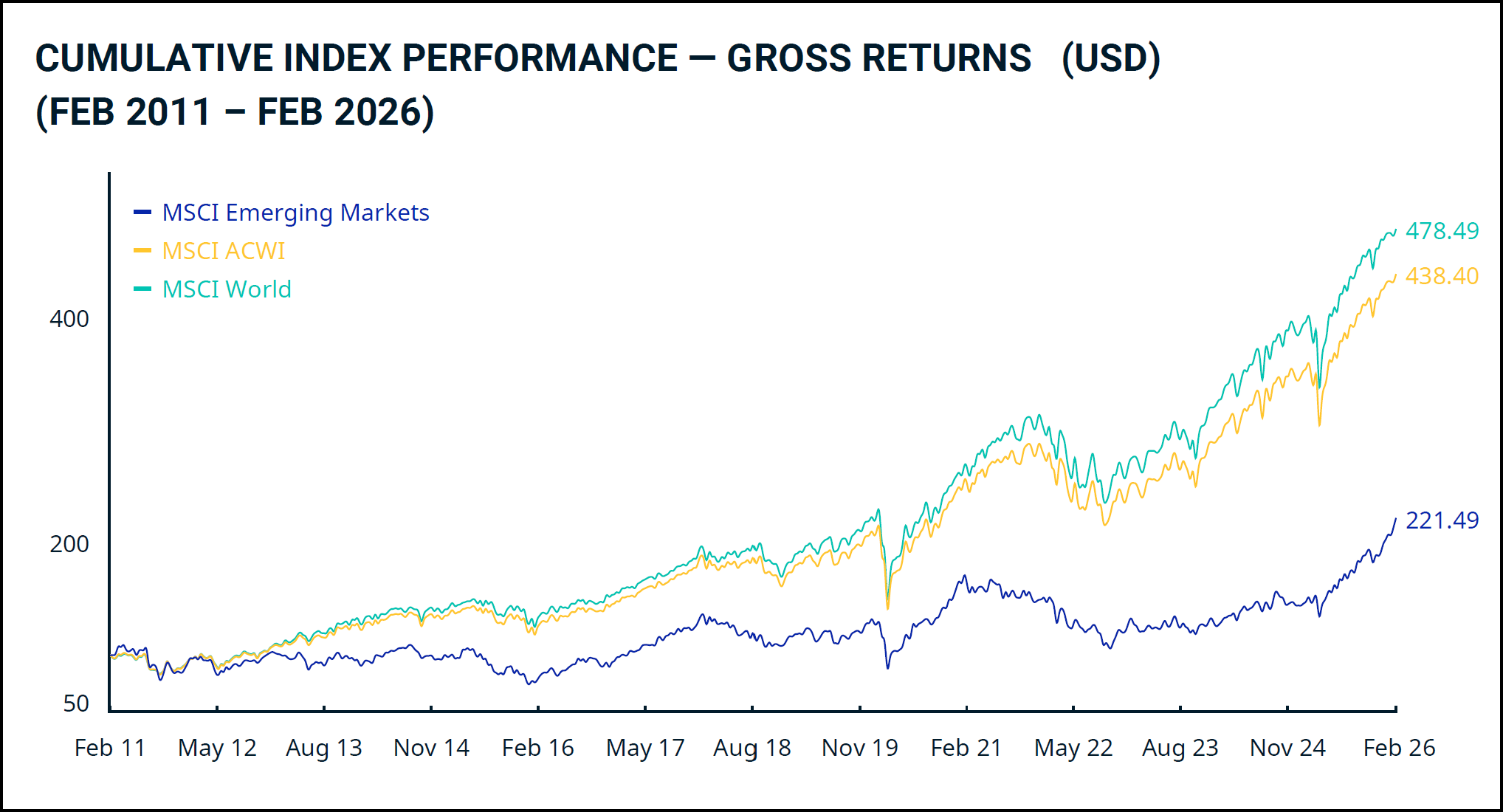

Option 1: High return + high availability = low security

Equities – strong long-term returns, volatile in the short term. Three classics in a 15-year comparison: MSCI World, MSCI ACWI and MSCI Emerging Markets. (Source: MSCI)

Equities are an example of this combination. They can generate attractive long-term returns and can be sold at any time during stock market trading hours. At the same time, they are sometimes subject to considerable price fluctuations – temporary losses in value of 30% or more are not uncommon in the past.

The security depends heavily on how broadly diversified the investment is. If you invest in individual shares, you risk a total loss in extreme cases – for example if a company goes bankrupt. With a globally diversified equity fund – such as an ETF on the global equity market – a total loss is practically impossible, as thousands of companies would have to become worthless at the same time. Diversification therefore reduces the risk considerably – but it does not eliminate the conflict of objectives in the magic triangle.

This category also includes commodities such as oil, grain and precious metals – whereby gold is considered more of a store of value and inflation hedge than a traditional investment – as well as real estate shares and REITs (exchange-traded real estate funds). Cryptocurrencies, which are among the most volatile asset classes of all, are particularly speculative.

Another option in this area is P2P crowdlending: investors lend money directly to private individuals or companies and receive higher interest rates than on a savings account. The expected returns are attractive, but the credit default risk is real – deposit protection does not apply here. Find out more in our article Crowdlending: P2P Switzerland on the rise.

Variant 2: High availability + high security = low return

Bank account – secure and available, but hardly any return.

The classic bank account combines maximum flexibility with a high level of security: balances of up to CHF 100,000 per person and bank are protected in Switzerland by deposit protection, and the money is available at all times. However, because the bank cannot plan the capital for the longer term, the interest rate is correspondingly low. In the current interest rate environment, the return is barely sufficient to compensate for inflation – the real value of the capital is thus at best maintained or even gradually decreases.

So anyone who opts for maximum security and availability is taking a different risk: a gradual loss of purchasing power and foregoing real asset growth.

Option 3: High security + higher return = low availability

Cash bonds and fixed-term deposits – only attractive to a limited extent in the current low interest rate environment, despite predictable returns.

Typical of this combination are forms of investment where the capital is tied up for a fixed term – in return for a higher interest rate than on a traditional bank account, which can at least enable real value retention.

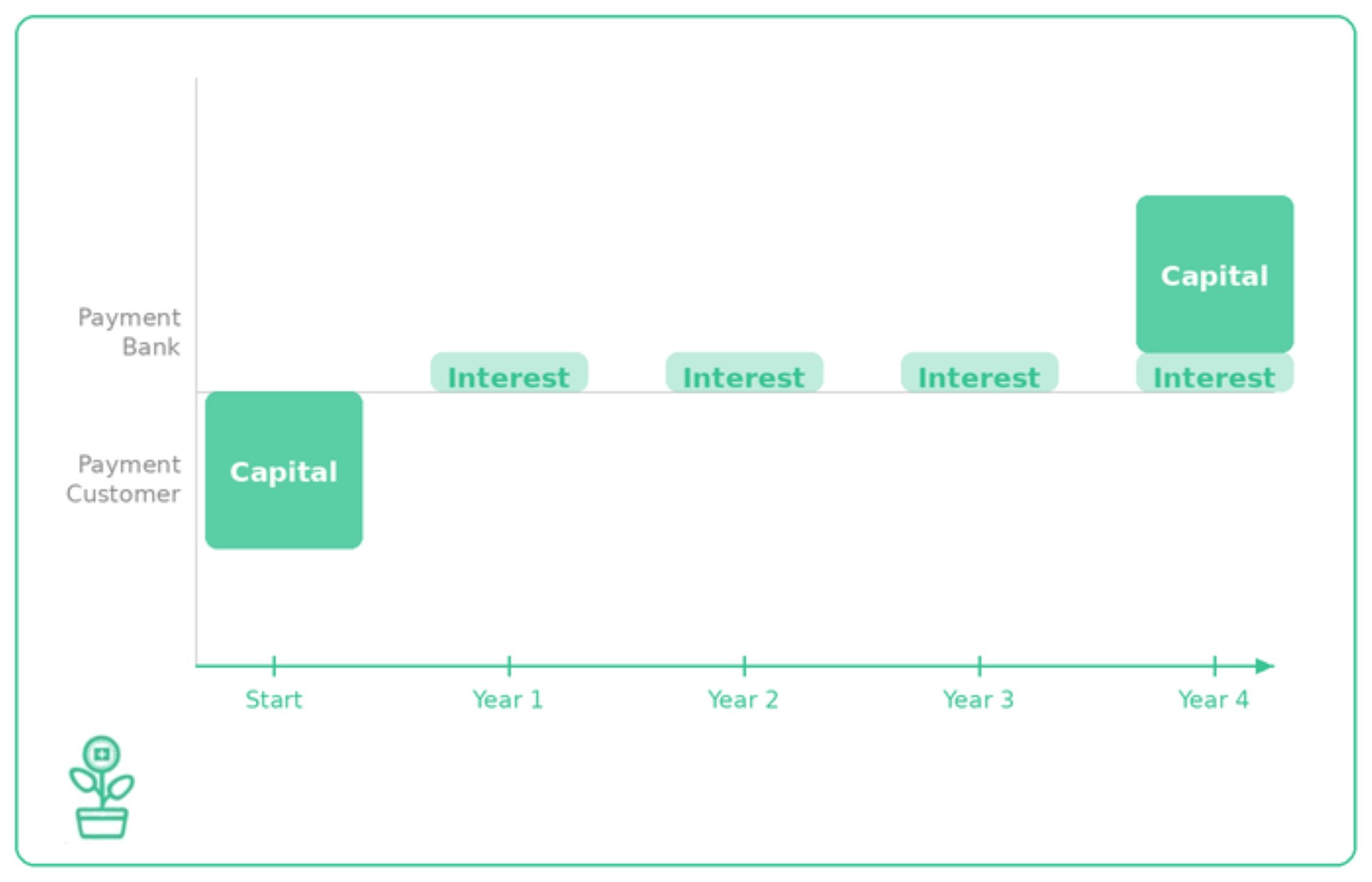

Medium-term notes are fixed-interest securities issued by banks. Investors lend their capital to the bank for a defined term – usually between two and ten years – and receive regular interest payments in return. As the bank can manage the capital more predictably, it pays an interest premium over the savings or private account. Deposit protection also applies up to CHF 100,000 per person and bank.

Fixed-term deposits work in a similar way: Here too, an amount is invested for an agreed term and earns interest at a fixed rate. The main difference to a medium-term note is that a fixed-term deposit is not a security – it is purely a bank deposit that also benefits from deposit protection.

The common price of both forms of investment is limited availability: anyone who wants to access their money early is dependent on goodwill solutions from the bank or must expect losses.

Note: In the current low interest rate environment, interest rates on medium-term notes and fixed-term deposits are also modest. Nevertheless, it is worth comparing providers, as the conditions can vary considerably depending on the bank.

Individual risk profile influences the magic triangle of investment

What your personal magic triangle looks like is not an abstract question – it depends directly on your individual risk profile. This is made up of your risk appetite and your risk capacity.

Your risk appetite: How much risk are you willing to take?

This describes your risk appetite – i.e. your psychological attitude towards fluctuations and possible losses. If you sleep peacefully, even if the portfolio temporarily loses 20 percent of its value, you have a high risk appetite. If, on the other hand, you panic every time prices fall, you should invest more conservatively – regardless of what is mathematically possible. Risk appetite is subjective in nature and is shaped by experience, personality and financial education, among other things.

Your risk tolerance: How much risk can you take?

This describes your risk capacity – i.e. your objective financial situation. It depends on how much capital you have available, what obligations you have and when you expect to need the invested money. If you have high fixed expenses or are dependent on the capital in the foreseeable future, you simply have less scope for risk – regardless of your personal attitude.

The interplay between risk appetite and risk capacity

Both factors together determine which of the three goals in the magic triangle should be your priority.

One example: Anyone planning a major expenditure in the next two to three years – such as buying a home – should focus their assets primarily on high availability and security. Even those who are generally willing to take risks and are relaxed about price fluctuations would be ill-advised to make risky investments in this situation. The ability to take risks – reduced here by the short investment horizon – sets a clear limit that overrides the willingness to take risks.

In short: risk appetite describes what you want – risk capacity describes what you can afford. For a sound investment strategy, both must be in harmony.

– Partner offer –

Still looking for the right financial solution? Our recommendations – with attractive starting bonuses.

——

Conclusion

The dream of a high-yield investment that is available at any time and 100% secure has come to an end. Unfortunately. As in other areas of life, we cannot avoid compromises when it comes to investing.

Which combination is the right one depends on your personal situation: your risk appetite and your risk capacity – which also includes your investment horizon. There is no universal best answer – only the one that suits you.

In lesson 3, we take a closer look: How can smart diversification optimize the risk/return ratio – and what does that mean for your portfolio in concrete terms?

2026-03-27: Text and illustrations completely revised.

Disclaimer

Disclaimer: Investing involves risks of loss. You must decide for yourself whether you want to bear these risks or not.

Errors excepted: We have written this article on the magic triangle of investing to the best of our knowledge and belief. Our aim is to provide you, as a private investor, with the most objective and meaningful financial information possible. However, if we have made any mistakes, forgotten important aspects and/or are no longer up to date, we would be grateful if you could let us know.