Newsletter

Newsletter

In this report, we will focus on the robots among investment advisors. The breakthrough seems to have been achieved. The range on offer in Switzerland is now large and confusing. Reason enough for us to We take a closer look at some of the most innovative robo-advisors in Switzerland. In this comprehensive Robo-Advisor Switzerland comparison, you will find out what these modern working machines are good for, how they differ and whether they are suitable for you.

Short & sweet

-

Robo-advisors make investing much easier for private investors: once the risk profile has been defined and a standing order set up, the investment process is fully automated.

-

The three robo-advisors examined – clevercircles (the “flexible”), findependent (the “price breaker”) and Selma (the “established”) – differ from each other, in some cases significantly.

-

What they have in common, however, is that they follow our preferred passive or index-based investment strategy. This is precisely why they can offer their services at fair prices.

-

The robo-advisors tested are particularly suitable for “savings plan fans”, “lazy people” and

“compromisers”. -

Compared to a do-it-yourself portfolio, they offer the following advantages, among others:

-

Savings plan capability

-

Simple rebalancing (at the touch of a button or fully automatic)

-

Personal dashboard with appealing data visualization, statistics and reports

-

Significant time savings

-

-

For investors who attach particular importance to the broadest possible range of ETFs and/or the lowest possible costs, however, the “do-it-yourself” portfolio remains the first choice.

-

With these vouchers you can secure a starting credit at clevercircles, findependent and Selma.

Contents

- Introduction to the topic “Robo-Advisor Switzerland”

- Robo-Advisor Switzerland comparison

- Robo-Advisor profiles

- Cost comparison between robo-advisors and ‘do it yourself’

- Robo-Advisor cost comparison with different investment sums

- Conclusion Robo-Advisor Switzerland comparison: Which Swiss Robo-Advisor is best for you?

- Robo-advisors: distinguishing features

- Bonus coupons for new customers

- This might also interest you

- Updates

- Disclaimer

Introduction to the topic “Robo-Advisor Switzerland”

Before we get to the specific Robo-Advisor Switzerland comparison, we would like to start by sharpening our basic understanding of Robo-Advisors and providing general information about their purpose.

What are robo-advisors?

A robo-advisor is an algorithm-based system that makes automatic investment recommendations and can also implement them. The term is a portmanteau word made up of the words robot and advisor. The aim of robo-advisors is to digitize and automate the services of a traditional financial advisor. The term “robo-advisor” is also used to describe financial service providers that work with corresponding systems. (Source: Wikipedia)

How can a robo-advisor be reconciled with our mission?

Good. This is because the three robo-advisors examined support a passive or index-based investment strategy. This means that only passive investment vehicles such as ETFs and/or index funds represent the investment universe. The running costs are somewhat higher than for purely self-organized investments. In return, however, brokerage fees (e.g. for savings plans by standing order or rebalancing) are saved. And finally, the overall costs are significantly lower than those incurred with conventional, active investment advice.

Who are robo-advisors suitable for?

If you belong to at least one of the following three groups, robo-advisors are an option worth considering:

“Savings plan enthusiasts”: Robo-advisors make it easy to invest smaller amounts on a regular basis. No matter how often you invest and how high your invested amount is, unlike a traditional broker, you do not incur any transaction fees in the form of brokerage fees.

“Lazy bums”: robo-advisors largely automate your financial investments. Based on your individual investment strategy and the corresponding risk profile, the robo-advisor takes care of your investment. The only requirement for this is that you “feed” it with money. It then invests this in the corresponding asset classes and investment products based on rules. In addition, the rather laborious manual rebalancing process is child’s play with a robo-advisor.

“Compromisers”: For those who are put off by the often (very) high fees of traditional asset management and the resulting lower returns, but at the same time shy away from the additional expense of a “do it yourself” investment, robo-advisors may represent the happy medium. This is because they are substantially cheaper than traditional asset management and yet very easy to use.

What happens if the Swiss robo-advisor goes bankrupt?

Your systems are protected by two measures:

- The cash is covered by the deposit guarantee of CHF 100,000,

- The risk-based investments are special assets, as these are the investment vehicles ETFs and index funds. Special assets are excluded from the bankruptcy estate.

How is the Swiss robo-advisor market performing?

The Swiss robo-advisor market has developed strongly in recent years. The offering is now as diverse as it is confusing. In a recent study, the comparison service moneyland.ch compared the asset management costs of traditional banks and no fewer than 14 different robo-advisors. The study concludes, among other things, that mandates from traditional banks are more than twice as expensive as the new online offerings.

Robo-Advisor Switzerland comparison

In this section, we look at the following three robo-advisors, which are positioned very differently on the Swiss market (presented in alphabetical order):

- clevercircles: the flexible one

- findependent: the price breaker

- Selma: the established one

We have entered into a cooperation with all three robo-advisors. As a new customer, you benefit from a starting credit.

Profiles of the three robo-advisors in Switzerland

Before we take a closer look at the registration process, investment universe, handling and pricing, you will find the most important key data of the three Robo-Advisors Switzerland providers we reviewed in Table 1.

Robo-Advisor profiles

| clevercircles | findependent | Selma | |

|---|---|---|---|

| Slogan | “The first self-determined asset management” | “Investing has never been so easy” | “Managing finances properly” |

| Founding year | 2018 | 2020 | 2016 |

| Legal form / registered office | AG / Basel | AG / Aarau | AG / Zürich |

| Managing Director | Sebastian Comment | Matthias Bryner | Patrik Schär |

| Partner bank | Bank CIC AG (owner of clevercircles) | None (findependent is a licensed custodian securities firm) | Saxo Bank AG |

| Flat-rate fees | 0,65% TCHF 5 – 100 0,55% TCHF 100 – 200 0,45% ab TCHF 200 0,25% ab CHF 1 Mio. Mindestgebühren CHF 40 | 0,40% TCHF 50 (bis TCHF 2 gratis) 0,38% TCHF 50 – 150 0,35% TCHF 150 – 250 0,33% TCHF 250 – 500 0,31% TCHF 500 – 1 Mio. 0,29% TCHF ab CHF 1 Mio. Keine Gebühren auf dem Cashbestand | 0,68% TCHF 2 – 50 0,55% TCHF 50 – 150 0,47% ab TCHF 150 |

| Minimum amount Initial investment | CHF 5’000 | CHF 500 | CHF 2'000 |

| Savings plan eligibility / minimum amount | Ja / CHF 100 | Ja / CHF 100 | Ja / CHF 100 |

| Trading platform | Internet & App | App | Internet & App |

| Communication channels | Chat / Phone / E-Mail | Chat / Phone / E-Mail | Chat / Phone / E-Mail |

| Specialties (optional) | Currency hedging, flexible rebalancing, own investment committee, free demo version | Own investment solution for the greatest possible self-determination, investing for children | Portfolio alignment according to ESG principles at the touch of a button, pension solution 3a integrated on the platform, AI-supported advice and portfolio analysis |

| New customer code / start bonus | SFB / CHF 100 | SFB20 / CHF 20 | sfbselma / CHF 34 |

How does onboarding work?

Onboarding in our Robo-Advisor Switzerland comparison includes the following four process steps for all three providers:

- Registration with the robo-advisor, including signing the contract and creating an individual risk profile based on a questionnaire,

- Opening an account with the partner bank, including signing the contract,

- the money transfer to the partner bank and

- the investments by the robo-advisor based on the determined risk profile

Important: With robo-advisors, the onboarding process is much more than a formality. Your risk profile is determined with the questionnaire to be completed. The risk profile in turn directly influences which asset classes you invest in and in what proportions. This results in your asset allocation, which ultimately has a significant influence on your return.

And one more thing: When transferring money, always specify yourself (and not the robo-advisor) as the beneficiary. Otherwise there will be an unwanted refund, as we experienced ourselves.

Positive: With all three providers, you can cancel immediately or at least at the end of the month (clevercircles) without incurring any costs.

clevercircles

Onboarding is purely digital and takes around 15 minutes. This also includes installing the “clevercircles” smartphone app. Clevercircles is the only provider that is not interested in your current income, which we welcome.

findpendent

Onboarding is purely digital via the app and has only taken around 10 minutes since obtaining the license as an account-holding investment firm in 2026.

Selma

In contrast to the other two providers, onboarding is supplemented with interaction with a customer advisor (flesh and blood) in addition to the digital part. In a video call, you are asked to hold the relevant ID document up to the camera by downloading an app or using a web browser. In addition, various data such as name and date of birth are obtained on the audio track for the purpose of personal identification. Finally, the user is asked to verbally confirm acceptance of the contract. This surprising intermezzo and the comparatively extensive list of questions mean that the onboarding process took the longest in our Robo-Advisor Switzerland comparison.

How does the investment universe present itself and how plausible is it?

All three providers in our Robo-Advisor Switzerland comparison exclusively use our preferred passive investment vehicles, ETFs and/or index funds. A distinction must be made between the investment universe of the robo-advisor and the investor. In this section, we will focus on the former, concentrating in particular on the “equities” asset class.

clevercircles

The clevercircles investment universe consists of 16 products, which are spread across the following asset classes:

- Shares (6 products)

- Bonds / Debentures (4)

- Real estate (3)

- Raw materials (2)

- Precious metals (1)

All products offered are based on indices, which are also transparently available here for non-customers. The “Equities” asset class covers the most important markets in the developed and emerging world. However, individual countries such as Canada, Australia and a few countries outside the eurozone (e.g. Norway) are not included. A “flaw”, but one that only has a minimal impact on returns. What’s more, if you value investments in sustainable ESG products, you’ve come to the wrong place with clevercircles. Unlike the other two providers, clevercircles does not offer any green shares.

findpendent

The investment universe of findependent consists of around 40 products, which are spread across the following asset classes:

- Equities (30 products; focus on sustainability)

- Bonds / Debentures (6)

- Real estate (2)

- Precious metals (1; gold)

- Bitcoin (1)

All products offered are ETFs, which are also transparently available here for non-customers. The “equities” asset class covers all markets in the developed world and emerging markets. It is noticeable that findependent focuses on sustainable investments and works with corresponding ratings and screenings. In addition, findependent offers five ETFs for the trend themes “Clean Energy”, “Robotics & Automation”, “Digitalization”, “Health” and “Gender” as a further unique selling point. In contrast to the other two providers, precious metals are not an issue with findependent.

Selma

Selma offers the following asset classes:

- Shares

- Private equity

- Bonds / Debentures

- Real estate

- Precious metals

A product list that reflects the investment universe is not published. However, we have received detailed insights on request. For example, with the exception of Canada and Australia, the most important markets from the developed world and emerging markets are covered in the “equities” asset class. In addition, a sustainable ESG orientation of the portfolio is optional and easily possible at the touch of a button.

How plausible and flexible are the risk profile and asset allocation?

Based on the questionnaire completed during onboarding, all three providers in our Robo-Advisor Switzerland comparison determine your risk profile, which in turn results in your individual asset allocation, i.e. your personal investment universe.

It cannot be mentioned often enough: Asset allocation is the be-all and end-all for your investment. As a rule of thumb, the higher your equity allocation, the more return and risk you can expect. As rational investors with a long investment horizon, we aim for the highest possible proportion of equities with a global focus.

Of course, this does not mean that we reject liquid assets per se. Cash reserves are undoubtedly important for current expenses, but also for the unexpected. But we don’t need a robo-advisor for that. We handle payment transactions and the like conveniently via our house bank, where we also park our “nest egg”.

clevercircles

With clevercircles, a distinction is made between “portfolio” (current asset allocation) and “strategy” (targeted or strategic asset allocation). At the beginning, the cash share is 100%, as the investment interval with clevercircles is 10 days.

In addition to the attractive visualization, we noticed positively that we were able to adjust the proposed strategy or asset allocation, which was a little too conservative for our taste, very easily using the slider. So we increased the equity component of our target allocation in no time at all, left the real estate, removed the bonds and reduced the cash component to the still permissible minimum of 4 percent (see Figure 1).

The actual portfolio is based on the strategy, as shown in Figure 2. Deviations can be balanced every two months by means of rebalancing.

Note: The minimum amount to be invested with clevercircles is actually 5,000 francs. clevercircles granted Stefan and Toni an exception for this Robo-Advisor Switzerland comparison. They were able to test clevercircles with separate accounts for 2,5000 francs each.

findpendent

At findependent, we also complete the pleasantly short questionnaire to the best of our knowledge and belief and receive the investor profile “courageous”. On closer inspection, this means a target portfolio with a share of 80 percent equities, 10 percent real estate, 8 percent bonds and 2 percent cash.

In order to throw out the (currently almost interest-free) bonds, we have to manually upgrade the risk to “risk-averse”. (According to information from findependent, the highest risk level “risk-averse” is never suggested directly by the robo-advisor, but must always be done manually by the client). The corresponding adjustment in the target allocation is made in a matter of seconds. The difference between the “bold” and “high-risk” profiles is essentially that the equity component is increased and the risk premiums are eliminated, as shown in Figure 3.

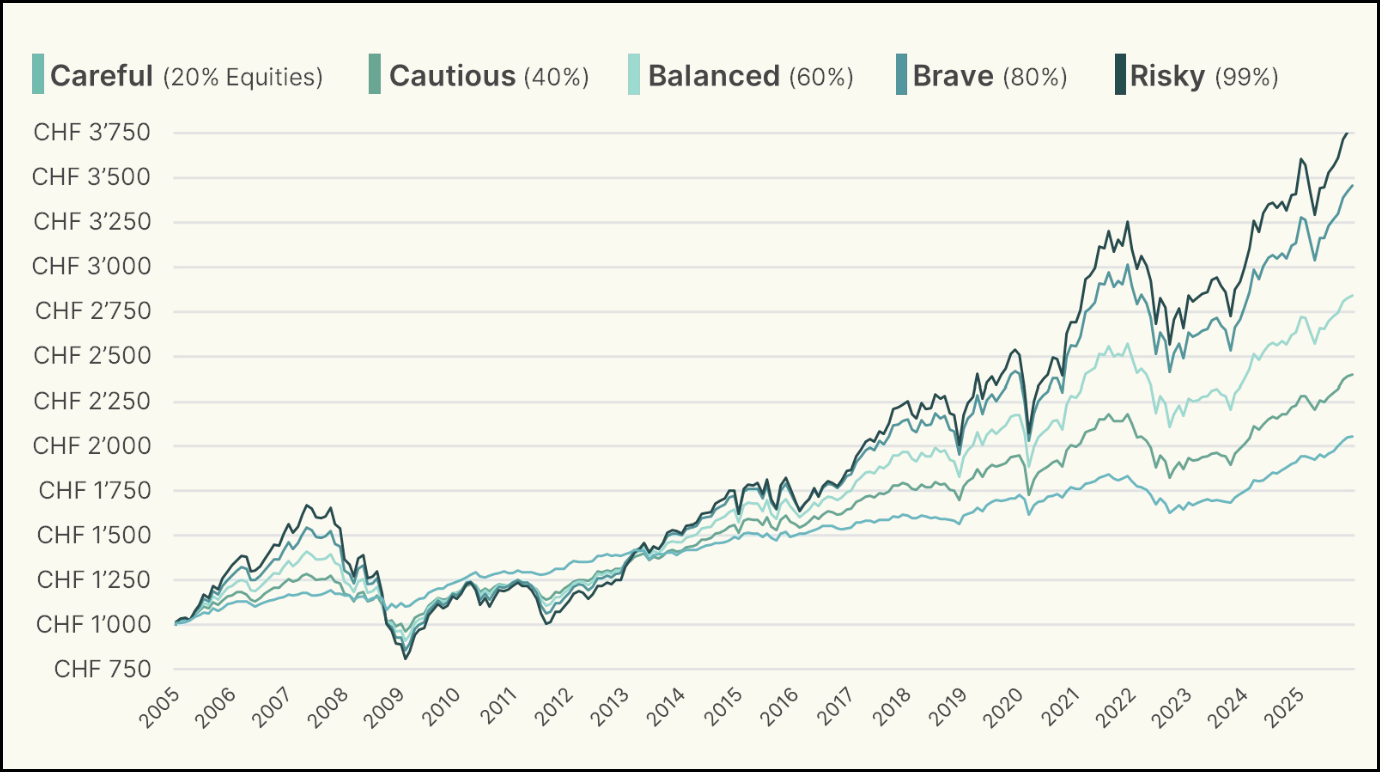

Figure 4 shows the performance of the four risk profiles offered by findependent from 2005 to 2021 and impressively confirms the investment principle: the higher the risk, the higher the return.

Unique: In addition to the four different risk profiles “considered”, “balanced”, “courageous” and “risk-taking”, you can put together your own investment solution – based on the findependent investment universe – from a sum of CHF 5,000. This means that findependent offers the highest degree of self-determination in the portfolio of all three robo-advisors examined.

Selma

At Selma, each investor is assigned their own planet, e.g. “Antunium” in the case of Antun (see Figure 5). As with the other two providers, we believe that the asset allocation determined is too conservative. We would therefore like to increase the proportion of equities, eliminate cash holdings as far as possible and remove the investments made by the robo-advisor in the asset classes cash, bonds and precious metals.

Easier said than done with Selma! Selma is the only provider that does not allow direct manipulation of the asset allocation. We learn via chat that the asset allocation can only be changed indirectly by adjusting the risk profile. Specifically, we have to answer the first question regarding risk appetite again. The “correct” answer that must be selected is “I like to speculate & like risk” (see Figure 6).

We do not understand the connection between speculation and a higher proportion of equities in the form of passive ETF equity investments. With regard to the asset class “equities”, day trading in the form of stock picking and market timing would be speculative investment behavior for us, which we as advocates of the buy and hold strategy are known to reject.

After all, by adjusting the risk profile, we got rid of the Oblis, but not the precious metals (see Figure 7). Supporter Marco explains this to us in the chat: “The precious metal share is currently higher, and will remain so for some time until the markets are no longer so overpriced.”

Selma does not seem to believe in efficient markets that are always correctly valued according to portfolio theory.

Positive: The adjustment is made promptly or on the following day.

As we later learned from Selma, unlike the other two providers, the investment strategy on which the asset allocation is based is adjusted dynamically, taking into account the customer’s individual life situation as well as market conditions.

Factors such as a changed asset situation (e.g. due to buying a house) or approaching retirement age influence the risk profile and therefore the asset allocation. Market-related factors that influence asset allocation include changes in global market capitalizations and shifts in overvaluations and undervaluations according to CAPE.

How does rebalancing work?

Depending on market developments, your portfolio may deviate from your target portfolio to a greater or lesser extent over time. In such cases, it makes sense to rebalance your portfolio periodically to bring it back into line with your asset allocation.

Rebalancing is very easy with robo-advisors, which we see as a clear advantage over the “do it yourself” portfolio. With the latter, rebalancing is carried out on a product-by-product basis through manually commissioned transactions. This procedure can be tedious and costly. With robo-advisors, on the other hand, rebalancing is carried out conveniently across the entire portfolio, although we were able to identify significant differences between the providers.

clevercircles

clevercircles offers the greatest flexibility in rebalancing. It is the only provider that does without an automatic process. Optionally, but conveniently at the touch of a button, the investor can have a rebalancing carried out every two months (see Figure 8). If no action is taken, no rebalancing takes place.

findpendent

With findependent, rebalancing is automated on a daily basis.

Selma

At Selma, rebalancing is generally automated every four weeks and, as mentioned, takes into account both client-specific and market-specific factors.

How high are the costs and how are they made up?

The main source of income for all three robo-advisors is a flat fee, which is charged as a percentage of the investment amount. The “do it yourself” investor saves this fee. In return, the robo-advisor includes administration and custody fees as well as brokerage fees.

All three robo-advisors rely on low-cost ETFs or index funds. We therefore assume that the product costs (TER) are largely identical to a “do it yourself” portfolio. Similarly, we do not expect any significant differences in exchange rate surcharges and stamp duty & stock exchange fees.

For a better understanding, we have broken down the most important cost blocks in the following table and compared them with those of a “do it yourself” portfolio:

Cost comparison between robo-advisors and ‘do it yourself’

| Cost blocks | Robo-Advisor | «Do it yourself» |

|---|---|---|

| Flat-rate fees | x | |

| Custody fees | x* | |

| Transaction costs / brokerage fees | x | |

| Product costs (TER) | x | x |

| Exchange rate surcharges | x | x |

| Stamp & stock exchange duties | x | x** |

clevercircles

clevercircles follows a degressive fee model with four tariff levels, which are 0.65% (TCHF 5 – 100), 0.55% (TCHF 100 – 200), 0.45% (from TCHF 200) or 0.25% (from CHF 1 million), depending on the investment amount, with a minimum charge of CHF 40 per year. If a more favorable tariff level is reached, this applies to the entire investment amount. Wealthy investors are therefore rewarded.

findpendent

findependent pursues a fee model that is quite unconventional in the industry, but certainly appealing. For example, no flat fees are charged at all for the first 2,000 francs. It is therefore not surprising that findependent’s price is particularly attractive for small investors.

Thereafter, a graduated approach is chosen and, depending on the investment amount, 0.40% (up to CHF 50,000), 0.38% (from CHF 50,000), 0.35% (from CHF 150,000), 0.33% (from CHF 250,000), 0.31% (from CHF 500,000) or 0.29% (from CHF 1 million) fees are charged. If a new level is reached, the new rate applies to the entire investment amount. Fair: Any cash is excluded from the flat fee.

Selma

Like clevercircles, Selma offers a degressive fee model with three tariff levels, which are 0.68% (TCHF 2 – 50), 0.55% (TCHF 50 – 150) or 0.47% (from TCHF 150), depending on the investment amount. If you reach a more favorable rate level, this applies to the entire investment amount. As with clevercircles, wealthy investors are therefore rewarded. On the positive side, Selma also takes into account any funds paid into the 3a pension plan integrated into its platform.

Robo-Advisor cost comparison with different investment sums

| Provider | CHF 25'000 | CHF 100’000 | CHF 500’000 | CHF 1'000’000 |

|---|---|---|---|---|

| clevercircles | CHF 163 | CHF 550 | CHF 2’250 | CHF 2'500 |

| findependent | CHF 92 | CHF 372 | CHF 1'544 | CHF 2'894 |

| Selma | CHF 170 | CHF 550 | CHF 2’350 | CHF 4’700 |

How good is the support?

All three providers in our Robo Advisor Switzerland comparison have a friendly and competent support team. In addition, they all offer comprehensible and informative FAQs. Naturally, there is no personal consultation. We found differences in the communication channels and response times.

Experience with support at clevercircles

A positive aspect of clevercircles is that individual questions are dealt with in detail. Inquiries by email are usually answered the following day. Alternatively, a telephone hotline is available. We were unable to test the chat function on the website because it was temporarily unavailable during our test phase for technical reasons. clevercircles informs us that the chat will be back in operation from January 2022 and will be continuously supported during office hours.

Experience with support at findependent

In our experience, findependent offers the most efficient support. All our inquiries have been answered via chat within a few minutes. This means that findependent fulfills its own ambitious claim that it usually responds within a few minutes with flying colors! The chat function is not only available on the website, but also in the app. In addition to the chat, you can also contact findependent by phone and email.

Experience with support at Selma

Selma offers e-mail, telephone and chat as communication channels. Answers in the chat are usually sent on the same day, but somewhat later than with findependent. (An e-mail is sent to inform you that a new chat message has been received). Positive: In contrast to findependent, the chat takes place via the login, which is why the chat histories can be called up again at any time.

Since 2024, Selma has offered the option of AI-supported robo-advisory services based on OpenAI technology. You can have your assets, your investment strategy or your investments assessed by artificial intelligence on the basis of various predefined questions (see example below).

What additional services are offered?

In this section, we want to take a closer look at the three Swiss robo-advisor providers in terms of special services. In doing so, we define additional services that not every robo-advisor offers or even represents a unique selling point (USP). Important: These services are all optional. This means that the investor can obtain these services, but does not have to.

clevercircles

clevercircles undoubtedly offers the widest range of special services:

- Currency hedging: Every two months, customers can decide for themselves how they want to hedge their investment in the two most important foreign currencies (EUR/USD) against currency loss. For each currency, they determine whether 30%, 60% or 90% of the foreign currency portfolio should be hedged. Currency hedging is free of charge for customers except for a minimal spread (90% discount from the official customer tariff of Bank CIC). According to clevercircles, the currency hedging feature is used regularly by more than half of its clients.

- Flexible rebalancing: Due to the different performance of the asset classes and markets, the portfolio can deviate significantly from the target allocation over time. With clevercircles, flexible rebalancing is possible at the touch of a button (every 2 months or longer), which brings the portfolio back into line with the defined strategy (see also this chapter).

- Your own investment committee / circle: If you are interested in what others think about financial matters, you can put together your own advisory committee (circle) consisting of investment professionals, business media, community, friends and family. Clevercircles therefore relies on group dynamics and swarm intelligence and thus also emphasizes the playful side of investing. We at the Swiss finance blog also have our own Circle. The Circles can also be used as a guide to overweight or underweight certain asset classes in the short term or depending on the market situation. We refrain from this tactical reallocation or corresponding recommendations because it does not correspond to our investment philosophy.

- Free demo version: If you would like to get to know the platform better without investing your own money, you can open a non-binding and free demo account for testing purposes.

findpendent

findependent enters the race with the following unique selling point:

- Your own investment solution: findependent offers those who value a particularly high degree of self-determination in their investments the opportunity to put together their own portfolio. You can choose from an investment universe of around 40 ETFs. This option is aimed at experienced and picky investors. From an investment amount of 5,000, you can participate at no extra cost.

- Investing for children: You can use the same app and the same account to invest in several investment goals (e.g. asset accumulation, child A and child B).

Selma

Selma offers the following additional services:

- More sustainable alignment of the existing portfolio according to ESG principles at the touch of a button.

- Pillar 3a pension provision: From an amount of CHF 500, you can invest in tied pension provision on the same platform. The same flat-rate fee is charged (see this section).

- AI-supported financial advice based on your Selma portfolio.

Conclusion Robo-Advisor Switzerland comparison: Which Swiss Robo-Advisor is best for you?

As can be seen from the pre-selection in this chapter, we believe that robo-advisors are particularly suitable for “savings plan enthusiasts”, “lazy people” and “compromisers”.

To summarize, we see the following four main advantages over a “do it yourself” portfolio:

- Savings plan capability

- Simple rebalancing (at the touch of a button or fully automated)

- Individual dashboard (attractive data visualization in the form of statistics and reports)

- Time saving

On the other hand, the “do it yourself” portfolio remains the first choice for investors who attach particular importance to a comprehensive range of products and/or thelowest possible costs. You will need a suitable trading platform for this : on our recommendations page you will find a selection of online brokers we have tested, including a starting balance (see also our series of articles Learn to invest – in eight lessons).

Decision-making aid Robo-Advisor Switzerland

Now that we have sharpened the profile of the three Robo-Advisor Switzerland providers examined (see in particular the profiles in this chapter), the following table will help you decide which provider is right for you. The criteria are distinguishing features that do not apply to all three robo-advisors examined and which vary in relevance depending on the type of investor:

Robo-advisors: distinguishing features

| Criteria | clevercircles | findependent | Selma |

|---|---|---|---|

| Multi-channel (app & web) | x | x | |

| Lowest costs and initial investment | x | ||

| Highest starting bonus | x | ||

| Highest degree of self-determination in portfolio construction | x | ||

| Sustainable investments | x | x | |

| Investments in trend themes | x | ||

| ”Precious metals” asset class | x | x | x |

| Currency hedging (optional) | x | ||

| Flexible rebalancing (optional) | x | ||

| Portfolio coordination with experts and the community (optional) | x | ||

| Non-binding demo version (optional) | x | ||

| Integrated 3a pension plan (optional) | x | ||

| Automatic adjustment of the investment strategy to the customer's individual life situation | x | ||

| Investing for children (investing in different investment goals) | x | ||

| AI-supported financial advice (optional) | x |

In addition, with regard to the positioning of the three robo-advisors in Switzerland, we noticed that clevercircles and findependent offer investors a great deal of freedom, while Selma takes more control. This comparatively high degree of guidance (or, depending on your point of view, limited flexibility) should appeal in particular to inexperienced investors or those with little interest in financial topics.

Bonus coupons for new customers

Have you been convinced by the offer of a provider in this Robo-Advisor Switzerland comparison? If so, secure a starting credit by simply selecting one of the following bonus coupons and entering the corresponding code when registering.

clevercircles bonus coupon worth CHF 100 (Robo-Advisor Switzerland comparison)

findependent bonus coupon worth CHF 20 (Robo-Advisor Switzerland comparison)

Selma bonus coupon worth CHF 34 (Robo-Advisor Switzerland comparison)

This might also interest you

Updates

2026-03-17: At findependent the license as an account-holding investment firm and its consequences are mentioned.

2026-01-12: Updated selectively.

2024-10-31: Note that the chat function has now also been integrated into the app.

2024-06-17: New AI-assisted analysis from Selma mentioned, including an example of Toni’s portfolio.

2024-05-22: Updated for findependent (lower) fees.

2023-07-03: New, staggered and more favorable tariff structure for findependent and note regarding the new option “Create for children” added.

2023-05-25: Clarification for Selma that the funds paid into the integrated 3a pension are taken into account in the tariff levels.

2023-05-12: New onboarding process via app mentioned at findependent.

2023-04-13: Investment universe at findependent increased to over 30 ETFs (from 25); automated rebalancing now takes place daily (originally monthly). New and most favorable tariff level of 0.25% mentioned at clevercircles.

2023-02-17: Added the new section “Short & sweet” at the beginning of the article.

Disclaimer

Disclaimer: Investing involves risks of loss. You must decide for yourself whether you want to bear these risks or not.

Errors excepted: We have written this article to the best of our knowledge and belief. Our aim is to provide you as a private investor with the most objective and meaningful financial information possible. However, should we have made any errors, forgotten important aspects and/or no longer have up-to-date information, we would be grateful if you could let us know.

Transparency note: In order to report credibly and realistically at first hand, the Schweizer Finanzblog team is a customer of the three Swiss robo-advisors examined at the time of publication or has invested its own money. There are also cooperation agreements with all three providers, which allow Schweizer Finanzblog to offer all new customers attractive special conditions in the form of starting credit. You can find the corresponding bonus coupons in this section.

6 Kommentare

Hoi Toni & Stefan

Danke erstmals für Eure super Blog!!

Was mich jedoch wundert: warum wird das Angebot/Produkte von Truewealth auf eurem Blog komplett totgeschwiegen? Auch via Suchfunktion gibt es “null” Treffer! Spekulativ kommen mir da höchstens persönliche Gründe oder zuwenig finanziellen Anreiz in den Sinn.. oder liege ich da komplett falsch?

Auch wenn ihr Truewealth nicht promoten wollt, wäre eine Einschätzung/Vergleich bei entsprechenden Themen (Vorsorge/RoboAdvisor/Sparplänte..) doch hilfreich und vertrauensbildend.

Besten Dank für Eure Antwort!

Liebe Grüsse

Tom

Hoi Tom

Merci fürs Lob und die Anmerkung bezüglich TrueWealth. Um bei unseren Reviews glaubwürdig aus erster Hand berichten bzw. aus dem Vollen schöpfen zu können, möchten wir bei den vorgestellten Anbietern jeweils selber Kunde sein. Bei TrueWealth sind wir dies nicht. Wahrscheinlich hat uns damals die nach wie vor geltende, relativ hohe Eintrittshürde von CHF 8’500 Starteinlage etwas abgeschreckt:-) Gegenfrage: Gibt es deines Erachtens einen zwingenden Grund “TrueWealth” einem der drei im obigen Artikel vorgestellten Robo-Advisors vorzuziehen?

Liebe Grüsse

SFB

Informativ, danke!

Sali Toni, Sali Stefan

wie immer sehr gute Arbeit und gut recherchiert. Danke für die Infos.

Die “Klassifizierung” gefällt mir sehr gut.

Die Auswahl an ETF’s erscheint mir bei allen jedoch sehr, sehr mager.

Das dürfte vermutlich an den Retrozessionen und Vertriebsentschädigungen liegen welche diese erhalten.

Somit ist der Kunden hier nicht immer am “Besten” bedient und investiert in EFT’s mit höherem TER und ggf. schlechterer Performance. Die Abweichungen sollten bei den einzelnen Index und ETF’s zwar nicht allzu gross sein aber es gibt sie wenn man die Rendite der Anbieter z.B. bei JustETF vergleicht. Einerseits ist dies bedingt durch den TER und anderseits durch den Tracking Error.

Die Integration von 3a und Freizügigkeitskonten finde ich sinnvoll. Dazu nutze ich derzeit VIAC zu günstigeren Konditionen. Für mich persönlich erscheint das Kosten/Nutzen Verhältnis noch zu hoch und unausgereift für den Mehrwert des automatischen Re balancing.

Bin mal gespannt wie sich das Ganze weiter entwickelt.

Hoi Arnaldo

Merci für deine Mitteilung und das positive Feedback.

Wir teilen deine Vorbehalte jedoch nicht ganz. Sicher, die Auswahl oder je nach Standpunkt die Qual der Wahl der zur Verfügung stehenden Anlageprodukte ist beim Robo-Advisor kleiner als beim “Do it yourself”-Portfolio. Aber letztlich wird dieses ja in der Regel auch nur aus einer Handvoll ETFs bestehen. Und bezüglich der Produktkosten (TER), so werden die von den drei getesteten Robo-Advisors verwendeten ETFs oder Indexfonds zu Marktpreisen (TER durchschnittlich rund 0,2%) angeboten. Mehrkosten bzw. Minderrenditen entstehen bei diesem Kostenblock gegenüber dem “Do it yourself”-Anleger also nicht.

Beste Grüsse

SFB

Hallo Arnaldo

Als Gründer von findependent nehme ich gerne kurz Stellung zur ETF-Auswahl. Das Angebot ist unbestritten einiges kleiner, als bspw. bei einem Broker. Wir haben uns aber ganz bewusst dafür entschieden, eine überschaubare ETF-Auswahl anzubieten, da zu viel Auswahl schnell auch überfordern kann. Wir nehmen auch bewusst keine Retrozessionen oder Vetriebsentschädigungen entgegen, damit wir bei der Auswahl der ETFs wirklich nur im besten Interesse der Kunden handeln können.

Liebe Grüsse

Matthias

Gründer von findependent